Employer Contribution Health Insurance Explained (2026)

Employer contribution health insurance is defined as the share of monthly premium costs your business pays on behalf of employees enrolled in a group health plan. This cost-sharing arrangement sits at the center of every employer-sponsored benefits package, and understanding it is non-negotiable for small business owners and self-employed individuals who want to build competitive teams without overspending. Employer-sponsored insurance is the largest source of private health coverage in the U.S., with employer contributions accounting for 6.9% of total private-industry compensation in 2025. That figure tells you just how significant this expense is relative to overall payroll.

How does employer contribution health insurance work?

The mechanics of health insurance employer contribution are straightforward. Your business selects a group health plan, negotiates a premium with an insurer, and then splits that monthly cost with each enrolled employee. Group health insurance pools risk across your workforce, which typically produces lower per-person premiums than anything available on the individual market. The employer pays the larger share; the employee pays the remainder through payroll deductions.

Here is how the cost-sharing structure typically breaks down:

- Employer share: Most small businesses cover 50%–80% of the employee-only premium. The exact percentage varies by plan design and company budget.

- Employee share: The remaining premium amount is deducted directly from each paycheck, usually on a pre-tax basis under a Section 125 cafeteria plan.

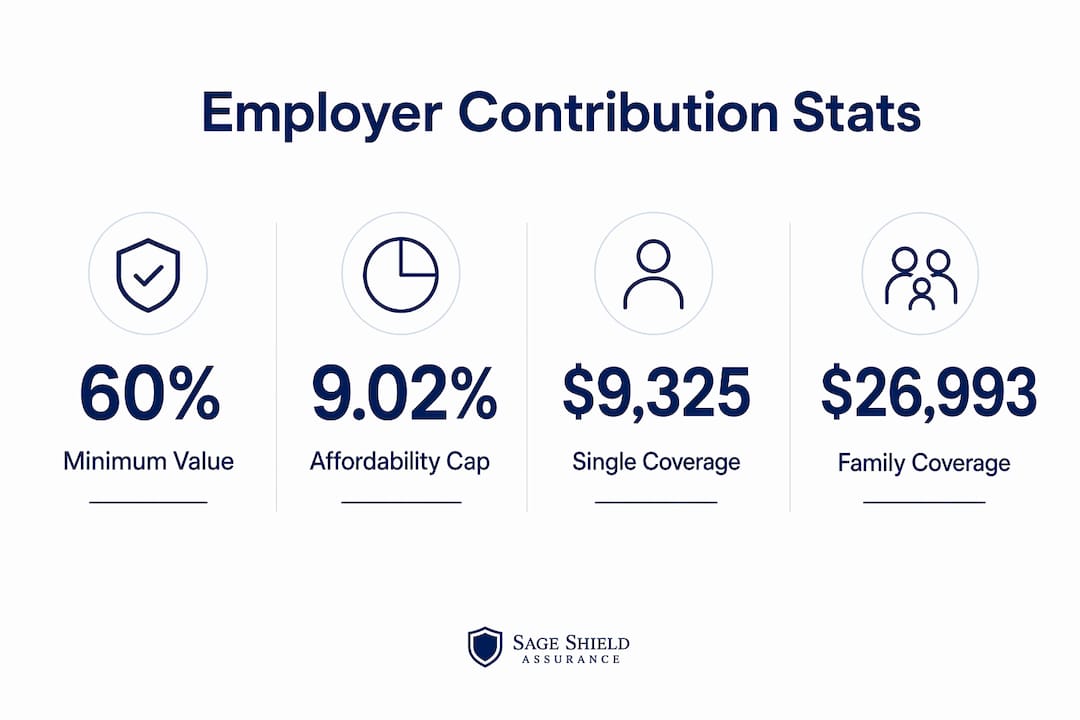

- Family and dependent tiers: Employers often contribute less toward family coverage than toward single coverage. Some contribute nothing toward dependents, leaving that cost entirely to the employee.

- Group rates: Because insurers spread risk across the whole group, group rates are lower than individual market premiums for comparable coverage.

Pro Tip: Set up payroll deductions under a Section 125 plan from day one. Employees pay their share pre-tax, which reduces your payroll tax liability at the same time it reduces theirs.

Average 2025 premiums reached $9,325 for single coverage and $26,993 for family coverage. Those numbers show why the employer-versus-employee split matters so much to your bottom line and to your team’s take-home pay.

What are the ACA rules for employer contributions?

The Affordable Care Act (ACA) imposes specific obligations on employers, and getting this wrong is expensive. The ACA’s employer shared responsibility provisions apply to businesses with 50 or more full-time equivalent employees, commonly called Applicable Large Employers (ALEs). Smaller employers are not legally required to offer coverage, but those who do must still meet minimum standards if they want to avoid triggering employee eligibility for premium tax credits.

Two tests define compliance: minimum value and affordability.

Minimum value means the plan must cover at least 60% of the total allowed cost of benefits. Most standard group plans clear this threshold automatically.

Affordability is the trickier test. For 2025 plan years, the ACA affordability threshold caps the employee-only premium at 9.02% of household income. Under the Federal Poverty Level (FPL) safe harbor, that translates to a maximum monthly employee contribution of approximately $113.20. If your employee pays more than that for self-only coverage, the plan fails the affordability test.

The IRS provides three safe harbor methods to simplify compliance:

| Safe Harbor Method | Basis for Calculation | Best For |

|---|---|---|

| FPL Safe Harbor | Federal Poverty Level for a single individual ($15,060 in 2024) | Simplest to administer; predictable budgeting |

| Rate of Pay Safe Harbor | Employee’s hourly rate or monthly salary | Employers with stable, salaried workforces |

| W-2 Safe Harbor | Employee’s prior-year W-2 Box 1 wages | Employers with consistent year-over-year payroll |

Employers prefer the FPL safe harbor because it produces predictable results and requires no individual income data from employees. Penalties only trigger when an employee actually claims a premium tax credit through the marketplace, but that risk is real and the fines are substantial.

Pro Tip: Even if you have fewer than 50 employees, document your contribution methodology using one of the three safe harbor methods. It protects you if your headcount grows and simplifies Form W-2 reporting from the start.

Employers must also report the cost of employer-sponsored coverage on employee W-2 forms. This reporting is informational for most employees, but it feeds into ACA compliance audits and affects plan design decisions.

What are the tax benefits of employer health insurance contributions?

The tax structure around employer contributions is one of the strongest financial arguments for offering group coverage. Employer premium contributions are excluded entirely from employee taxable income and reduce payroll taxes for both the employer and the employee. That is a direct subsidy built into the federal tax code.

Here is where the savings stack up:

- For employees: The portion of premium deducted from their paycheck under a Section 125 plan reduces their federal income tax, state income tax (in most states), and FICA taxes.

- For employers: Premium payments are fully tax-deductible as a business expense, reducing your net cost of offering coverage.

- For both parties: Pre-tax health deductions create federal and state subsidies that make employer-sponsored coverage far cheaper than equivalent after-tax compensation.

The competitive advantage is just as real as the tax savings. Employer-sponsored insurance functions as tax-advantaged compensation, meaning you can offer more total value to employees without raising gross salaries. For a small business competing against larger companies for talent, that matters. Health benefits consistently rank among the top factors employees weigh when evaluating job offers.

For self-employed individuals who hire even one or two employees, the combination of tax deductions and group rate access makes a group plan worth serious consideration versus sending employees to the individual market.

How do plan types affect employer contribution structures?

Not all group health plans work the same way, and the plan type you choose directly shapes how much you and your employees pay. Common employer health plan types include Health Maintenance Organizations (HMOs), Preferred Provider Organizations (PPOs), and High-Deductible Health Plans (HDHPs). Each carries a different premium level and out-of-pocket structure.

| Plan Type | Typical Premium Level | Network Flexibility | Employee Out-of-Pocket Risk |

|---|---|---|---|

| HMO | Lower | In-network only; requires referrals | Lower deductibles and copays |

| PPO | Higher | In-network and out-of-network | Moderate deductibles and copays |

| HDHP | Lowest | Varies; often broad | High deductible; pairs with HSA |

HDHPs carry the lowest premiums, which reduces your monthly contribution cost. The trade-off is that employees face higher deductibles before coverage kicks in. Most ACA-compliant employer plans cap out-of-pocket costs at $10,600 for 2026, but employees on HDHPs can hit that ceiling faster than those on HMOs.

Contribution structures also vary by coverage tier. Most employers contribute a fixed dollar amount or percentage toward employee-only coverage and offer a separate, often lower, contribution toward employee-plus-family tiers. A small business might cover 70% of a single HMO premium but only 40% of the family premium. Knowing your workforce demographics helps you choose the tier structure that delivers the most value per dollar spent.

Practical tips for small business owners managing health contributions

Managing employer health insurance contributions well requires more than picking a plan. You need a system.

- Calculate total employer cost before committing. Add up premiums, administrative fees, and any broker costs. Compare that against your payroll budget before you sign.

- Use the FPL safe harbor from day one. It simplifies ACA compliance and makes annual budgeting predictable, even if you are currently below the 50-employee threshold.

- Plan for premium increases. Group health premiums typically rise each year. Build a 5%–10% annual increase into your benefits budget so renewals do not catch you off guard.

- Work with a licensed broker. A qualified broker compares plans across multiple carriers, flags compliance risks, and manages enrollment administration so you are not doing it alone.

- Consider private health insurance for very small teams. If you have one or two employees, private health insurance for business owners may offer better value than a full group plan.

Pro Tip: Review your plan options every year at renewal, not just when you first set up coverage. Carrier pricing shifts, and a plan that was the best value two years ago may no longer be. Use a premium comparison tool to benchmark your current plan against alternatives.

Key takeaways

Employer contributions to health insurance are the most tax-efficient form of employee compensation available to small business owners, and getting the structure right protects both your budget and your compliance standing.

| Point | Details |

|---|---|

| Employer contribution defined | The share of monthly health insurance premiums your business pays on behalf of enrolled employees. |

| ACA affordability threshold | Employee-only premiums cannot exceed 9.02% of household income; the FPL safe harbor caps this at roughly $113.20 per month. |

| Tax advantages are real | Employer premiums are fully tax-deductible; employee shares are deducted pre-tax, reducing FICA and income taxes for both parties. |

| Plan type drives cost | HMOs carry lower premiums; HDHPs reduce employer cost but shift more out-of-pocket risk to employees. |

| Broker support reduces risk | A licensed broker manages plan comparison, compliance documentation, and annual renewal to prevent costly mistakes. |

What i’ve learned working with small employers on health benefits

Most small business owners I work with underestimate one thing: the gap between offering a plan and offering a compliant plan. They assume that signing up with a carrier and paying premiums satisfies their obligations. It does not. The ACA’s affordability test is where I see the most expensive mistakes. An employer sets a contribution that feels generous, but because it was not benchmarked against the 9.02% threshold or a safe harbor method, an employee qualifies for a marketplace tax credit. That triggers a penalty notice the employer never saw coming.

The other pattern I see constantly is employers who set their contribution structure once and never revisit it. Premiums rise, employee demographics shift, and the plan that made sense three years ago now costs 30% more while covering a workforce that has aged into higher utilization. Annual reviews are not optional. They are the difference between a benefits program that works and one that quietly drains your budget.

My honest advice: do not treat health insurance as a checkbox. Treat it as a financial instrument. The tax advantages are real, the retention value is measurable, and the compliance risk is manageable. But only if you stay current on the rules and work with someone who does this every day.

— mkaravas1m

How Sageshieldassurance helps you get this right

Sageshieldassurance works specifically with self-employed individuals and small business owners who need more than a generic plan recommendation. Their team compares options across leading carriers, applies the right ACA safe harbor method for your workforce, and manages the compliance documentation that protects you at renewal and audit.

If you are ready to stop guessing on contribution amounts and start building a benefits structure that works for your budget and your team, Sageshieldassurance is the right starting point. Explore health insurance plans tailored to small employers, or get a personalized review from their brokers who have served over 500 families across 40 states. You can also review brokerage support options to understand exactly what professional guidance covers.

FAQ

What is an employer contribution to health insurance?

An employer contribution is the portion of a group health insurance premium the business pays on behalf of its employees. The employee pays the remaining share, typically through pre-tax payroll deductions.

How much do employers typically contribute to premiums?

Most employers cover 50%–80% of the employee-only premium. Average 2025 premiums were $9,325 for single coverage and $26,993 for family coverage, so the employer share represents a significant compensation cost.

What is the ACA affordability rule for employer plans?

For 2025 plan years, the ACA caps the employee-only premium at 9.02% of household income. Under the FPL safe harbor, that equals a maximum monthly employee contribution of approximately $113.20.

Are employer health insurance contributions tax-deductible?

Yes. Employer premium payments are fully tax-deductible as a business expense. Employee contributions deducted through a Section 125 plan also reduce federal income tax and FICA taxes for both the employer and the employee.

Do small businesses have to offer health insurance?

Businesses with fewer than 50 full-time equivalent employees are not required by federal law to offer health coverage. However, those that do offer coverage must meet ACA minimum value and affordability standards to avoid exposing employees to marketplace tax credit eligibility.

Leave a Reply