Association Health Plans for Small Business Owners: 2026 Guide

An association health plan (AHP) is group health coverage sponsored through a bona fide association of employers that pools purchasing power to buy insurance collectively under ERISA. Small businesses with fewer than 50 employees typically cannot access large-group rates on their own. AHPs solve that problem by letting multiple employers join together through a qualifying association, giving them the collective weight of a much larger workforce. Understanding what is an association health plan, how eligibility works, and where the trade-offs lie is the first step toward making a sound coverage decision for your business in 2026.

How do association health plans work for small businesses?

An AHP is a structural arrangement for pooled purchasing, not a new type of insurance product. Small businesses band together through a qualifying association to buy large-group or self-insured health plans they could not access individually. The association acts as the plan sponsor, and each member employer participates in a single group plan rather than shopping the individual or small-group market.

The mechanics work like this. A bona fide association, such as a trade group or professional organization, negotiates with an insurer or sets up a self-funded arrangement on behalf of its member employers. Each employer pays premiums or contributions based on their workforce size. The insurer or third-party administrator then covers claims across the entire pooled membership.

The key legal concept here is “commonality of interest.” Member employers must share a genuine connection, whether by industry, profession, or geography, not just a desire to buy cheaper insurance. ERISA’s employer definition treats the association as a single employer for regulatory purposes, which is what unlocks large-group plan treatment.

AHPs differ from traditional small-group plans in one critical way. A small-group plan covers only one employer’s workers. An AHP aggregates dozens or hundreds of employers under one plan, spreading risk across a much larger pool. That scale can translate into lower premiums and access to plan designs that small employers rarely see in the individual market.

Pro Tip: Ask any association whether it is fully insured or self-funded before enrolling. Self-funded AHPs carry different financial risks and regulatory treatment, and your state’s insurance department may have limited oversight over them.

What are the eligibility requirements to join or form an association health plan?

Eligibility for an AHP is stricter than most small business owners expect. The association sponsoring the plan must meet specific criteria under ERISA before it can offer coverage to member employers.

- Independent business purpose. The association must exist for reasons beyond providing health insurance. A trade association, professional society, or chamber of commerce qualifies. A group formed solely to buy health coverage does not.

- Genuine commonality of interest. Members must share a substantive organizational relationship. Commonality must be substantive, reflecting genuine ties beyond geographic proximity or a shared interest in cheaper premiums.

- Employer control and governance. Member employers must have meaningful control over the association’s activities. The association cannot be run entirely by an insurer or third-party promoter.

- Restricted membership. AHP membership is restricted to qualifying employers and their workers. The general public cannot join the way they can purchase an individual market policy.

- Documentation requirements. Associations typically require proof of business status, industry affiliation, and employee count. Incomplete documentation is one of the most common reasons employers are denied membership.

The 2018 Department of Labor rule temporarily broadened these criteria, allowing sole proprietors and geographically connected employers to qualify more easily. That rule was later rescinded. The current standard reverts to a facts-and-circumstances test under ERISA, meaning each association’s eligibility is evaluated individually based on its structure and purpose.

Pro Tip: Before applying to join an AHP, request the association’s governing documents and ask specifically how it demonstrates commonality of interest. If the association cannot produce clear documentation, that is a red flag for regulatory compliance.

What are the benefits and limitations of association health plans?

AHPs offer real advantages for small business owners, but they come with trade-offs that deserve honest attention.

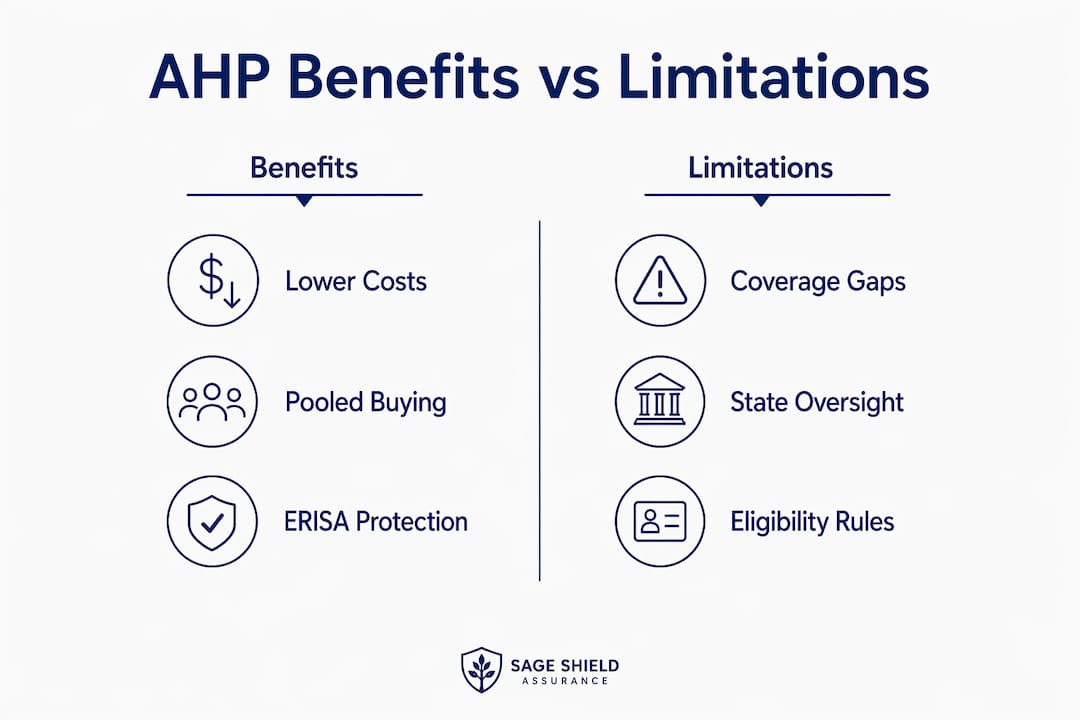

Key benefits

- Lower premiums through pooled bargaining. The Congressional Budget Office found that AHPs could lower premiums for small businesses by enabling common-interest groups to purchase plans collectively. Pooling spreads risk and increases negotiating leverage with insurers.

- Access to large-group plan features. Small employers gain access to plan designs, networks, and benefit structures that are typically reserved for companies with hundreds of employees.

- Flexibility in plan design. Some AHPs offer a wider range of deductible and network options than the small-group market provides.

- Self-funded options. Some associations operate self-insured AHPs, which can offer additional cost control and plan customization.

Key limitations

| Factor | AHP | ACA Small-Group Plan |

|---|---|---|

| Essential health benefits | May not be required | Required by law |

| Consumer protections | Varies by plan | Standardized under ACA |

| Premium rating rules | May differ | ACA-regulated |

| State oversight | Limited (ERISA preemption) | Full state regulation |

| Open to public | No, restricted membership | Yes, through marketplace |

AHPs may avoid some ACA requirements, including the mandate to cover the 10 essential health benefits. That flexibility cuts both ways. It can lower premiums, but it can also leave gaps in coverage for things like mental health services, maternity care, or prescription drugs.

Entrepreneurs who focus only on the premium savings often miss the coverage gaps. A plan that costs less per month but excludes a benefit your employees need is not a bargain. Entrepreneurs benefit from pooled bargaining power but face real trade-offs in consumer protections, making careful plan review non-negotiable.

How to evaluate and choose the right association health plan

Choosing an AHP requires more due diligence than selecting a standard small-group plan. The variation in plan design across AHPs is wide, and plan details vary significantly and should be reviewed carefully before enrollment.

Start with these steps:

- Read the Summary of Benefits and Coverage (SBC). The SBC is a standardized document that shows covered services, cost-sharing amounts, and coverage limits. Compare it line by line against your current plan or ACA alternatives.

- Verify network access. Confirm that your employees’ current doctors and preferred hospitals are in the plan’s network. Out-of-network costs in AHPs can be significant.

- Check prescription drug coverage. AHPs that are not ACA-compliant may have narrower formularies. Verify that common medications your team uses are covered at reasonable cost-sharing levels.

- Understand the association’s financial stability. For self-funded AHPs, ask about stop-loss insurance and reserve levels. A financially unstable association can leave members with unpaid claims.

- Compare total cost, not just premiums. Factor in deductibles, co-pays, out-of-pocket maximums, and any excluded services when calculating the true cost of coverage.

Working with a knowledgeable benefits adviser is the most reliable way to avoid surprises. Marketing claims about savings should always be validated with side-by-side benefit comparisons and careful review of co-pays, covered services, and prescription rules in the SBC. An adviser who specializes in small business health coverage can run that comparison for you and flag gaps before you commit.

You should also review your employer contribution obligations under any AHP, since contribution rules vary by plan and affect your total cost of offering coverage.

What regulatory changes should small businesses watch in 2026?

The regulatory environment for AHPs has shifted repeatedly over the past decade, and small business owners need to stay current.

- The 2018 DOL rule and its rescission. The Department of Labor’s 2018 rule expanded AHP eligibility broadly, including for sole proprietors and geographically linked groups. A federal court struck down key provisions, and the rule was later rescinded. The current standard returns to ERISA’s original facts-and-circumstances test.

- ERISA preemption and state oversight. ERISA-governed AHPs are largely exempt from state insurance regulations. That means state consumer protections that apply to fully insured small-group plans may not apply to your AHP.

- Ongoing legal challenges. Court decisions continue to shape which associations qualify and what coverage standards apply. Regulatory volatility means associations and advisers must re-validate qualification and compliance documentation regularly, especially before each enrollment period.

- Legislative proposals. Bills like the Association Health Plans Act have been introduced in Congress to codify expanded eligibility. None have passed as of 2026, but legislative activity signals continued policy debate.

- State-level variation. Some states have enacted their own AHP regulations that add requirements beyond ERISA. Check your state’s insurance department rules before enrolling.

“Due to political and regulatory changes, small businesses should expect eligibility criteria and requirements for AHPs to evolve and consult current experts.” — Goldwater Institute

Small businesses should expect eligibility criteria to continue shifting. Building a relationship with a benefits adviser who tracks these changes is not optional. It is the only reliable way to stay compliant and avoid coverage disruptions.

Key takeaways

Association health plans give small businesses access to large-group coverage through pooled purchasing under ERISA, but eligibility requirements, ACA trade-offs, and regulatory volatility make expert guidance non-negotiable before enrollment.

| Point | Details |

|---|---|

| AHP definition | An AHP is group coverage sponsored by a bona fide employer association under ERISA, not a standalone insurance product. |

| Eligibility is strict | Associations must have an independent business purpose, genuine commonality, and employer governance to qualify. |

| ACA trade-offs exist | AHPs may skip essential health benefits, so always compare the SBC against ACA-compliant alternatives. |

| Regulatory environment shifts | The 2018 DOL rule was rescinded; current eligibility uses a facts-and-circumstances test that can change again. |

| Expert review is critical | Work with a benefits adviser to validate savings claims, network access, and compliance before enrolling. |

My honest assessment of AHPs for entrepreneurs

I have reviewed a lot of health insurance options for small business owners, and AHPs sit in an interesting middle ground. They are genuinely useful for the right employer in the right association. A freelance graphic designer joining a professional creative industry association with a long track record and solid governance? That can work well. A small retailer being pitched an AHP by a group that formed six months ago with no clear business purpose beyond selling coverage? Walk away.

The thing most articles do not say plainly is this: the savings are real in some cases, but the coverage gaps are also real. I have seen business owners enroll in an AHP because the premium was $200 per month lower, only to discover that mental health coverage was excluded or that their preferred specialist was out of network. The SBC comparison step is not bureaucratic box-checking. It is the difference between a good deal and an expensive mistake.

My strongest recommendation is to treat regulatory stability as a selection criterion. An AHP backed by a well-established trade association with decades of history is far less likely to face compliance disruption than one built around a newer or loosely defined group. The self-employed coverage options available in 2026 are broader than most owners realize, and AHPs are one tool in a larger toolkit, not the only answer.

— mkaravas1m

Sageshieldassurance can help you find the right health plan

Small business health insurance decisions carry real financial and legal consequences. Sageshieldassurance works with entrepreneurs and business owners across 40 states to cut through the complexity and find coverage that fits both their workforce and their budget.

Sageshieldassurance’s team reviews AHP options alongside ACA small-group plans, self-funded arrangements, and individual coverage alternatives to give you a complete picture before you commit. Every client gets a side-by-side benefit comparison, a policy review, and ongoing support as regulations change. If you are weighing an AHP or any other group health option, the health insurance specialists at Sageshieldassurance are ready to walk you through it with no pressure and no guesswork.

FAQ

What is an association health plan in simple terms?

An association health plan is group health insurance that small businesses buy collectively through a qualifying employer association under ERISA. It gives small employers access to large-group plan pricing and features they could not get on their own.

Who qualifies to join an association health plan?

Employers who belong to a bona fide association with a genuine business purpose and shared commonality of interest qualify. The general public cannot join, and membership requires documentation of business status and association eligibility.

Do association health plans cover the same benefits as ACA plans?

Not always. AHPs may skip some ACA requirements, including coverage of the 10 essential health benefits. Always review the plan’s Summary of Benefits and Coverage and compare it directly against ACA-compliant alternatives before enrolling.

Are association health plans regulated by states or the federal government?

ERISA-governed AHPs are primarily subject to federal oversight, which limits state insurance regulators’ authority over them. Some states have added their own AHP rules, so check both federal ERISA standards and your state’s insurance department requirements.

How has the regulatory environment for AHPs changed recently?

The Department of Labor’s 2018 rule expanded AHP eligibility significantly, but it was later rescinded after court challenges. The current standard uses ERISA’s original facts-and-circumstances test, meaning each association’s eligibility is evaluated individually based on its structure and documented purpose.

Leave a Reply