What Is Group Health Coverage for Small Business Owners

Group health coverage is employer-sponsored insurance that pools employees under a single policy to deliver lower-cost medical benefits than most individuals can access on their own. For small business owners and self-employed individuals with staff, it is one of the most powerful tools available for controlling healthcare costs while competing for talent. Understanding how group medical coverage works, what it costs, and who qualifies can mean the difference between a benefits package that retains employees and one that drives them to larger competitors.

What is group health coverage and how does it work?

Group health coverage is defined as a health insurance policy purchased by an employer and extended to eligible employees, often including their dependents. The core mechanic is risk pooling: by covering a broad group of people, the insurer spreads the financial risk of high medical claims across many members. Employer-sponsored insurance remains the most common form of private coverage in the United States precisely because this pooling stabilizes premiums and avoids the adverse selection that drives up costs in individual markets.

The employer selects a plan type and carrier, then employees enroll during an open enrollment window or within a qualifying life event period. Common plan structures include HMOs (Health Maintenance Organizations), PPOs (Preferred Provider Organizations), and HDHPs (High Deductible Health Plans). Each carries different tradeoffs between monthly premium costs, provider flexibility, and out-of-pocket exposure. Group plans must also cover the 10 essential health benefits mandated by the Affordable Care Act, including hospitalization, prescription drugs, and maternity care.

Pro Tip: If your workforce skews younger and healthier, an HDHP paired with a Health Savings Account can lower your premium spend significantly. Review your team’s average age and claims history before defaulting to a PPO.

How does group health insurance work for premiums and enrollment?

The premium split between employer and employee is the financial backbone of group health insurance explained simply: the employer pays a share, and the employee pays the rest through payroll. Employers typically contribute at least 50% of the individual employee premium, with many paying more to stay competitive in their hiring market. That means employees often pay less than half the true cost of their coverage, which is a meaningful compensation benefit even when wages are modest.

Employees pay their share through pre-tax payroll deductions, which reduces their taxable income and increases effective take-home pay. A worker paying $300 per month in premiums pre-tax saves real money compared to buying the same coverage with after-tax dollars on the individual market. Federal law also sets a clear boundary on eligibility delays: employers may impose a waiting period for new hires, but it cannot exceed 90 days under current federal rules. That protects employees from being left uninsured for extended periods after starting a new job.

Here is a straightforward breakdown of how enrollment typically flows for a small business:

- The employer selects a carrier and one or more plan options.

- Eligible employees receive enrollment materials during the open enrollment window.

- Employees choose their plan tier and add any dependents.

- Premium deductions begin on the first paycheck of the coverage period.

- Coverage renews annually, with the employer reviewing plan performance and costs each year.

What are the main funding models for group health plans?

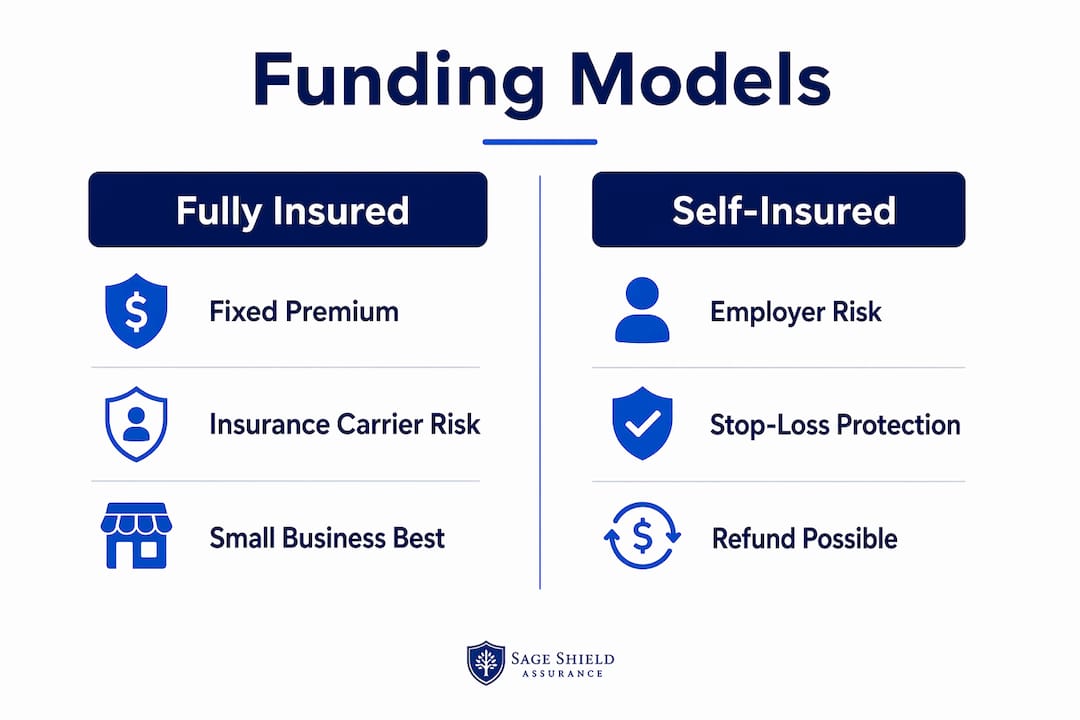

Not every group health plan is structured the same way. The three primary funding models are fully insured, self-insured, and level-funded, and each carries different implications for cost, risk, and flexibility.

Fully insured plans are the most common for small businesses. The employer pays a fixed monthly premium to an insurance carrier, and the carrier assumes all financial risk for claims. Costs are predictable, but the employer has no opportunity to recoup money if claims run low.

Self-insured plans shift the financial risk to the employer. The business pays claims directly, typically with stop-loss insurance to cap catastrophic exposure. This model suits larger employers with enough employees to absorb claims volatility.

Level-funded plans occupy the middle ground. Level-funded plans combine fixed monthly payments with stop-loss protection and offer potential refunds if actual claims come in below projections. For small employers who want cost control without the full exposure of self-insurance, level-funded plans are worth serious consideration.

| Funding model | Risk holder | Refund possible | Best for |

|---|---|---|---|

| Fully insured | Insurance carrier | No | Businesses wanting predictability |

| Self-insured | Employer | N/A | Larger employers with claims data |

| Level-funded | Shared (with stop-loss) | Yes | Small businesses seeking cost control |

Most states require employers to contribute a minimum portion of premiums, but many exceed this minimum to attract and retain employees in competitive markets. Employers commonly pay between 50% and 80% of total premium costs depending on industry and region.

Pro Tip: Ask your broker to model a level-funded plan alongside your current fully insured quote. If your group has had low claims for two or more consecutive years, the refund potential alone can offset a meaningful portion of your annual premium.

How does group coverage compare to individual health insurance?

The difference between group and individual health insurance comes down to three factors: price, underwriting, and stability. Small businesses with fewer than 50 employees can reduce healthcare costs by 20 to 30% per enrollee by choosing a group plan over individual market coverage. That gap exists because group plans spread risk across all enrolled employees, while individual plans price each person based on age and geography.

Individual plans also carry more volatility. Premiums on the individual market can shift significantly year over year based on insurer participation in a given state’s exchange. Group plans, by contrast, renew with the same carrier and benefit structure unless the employer actively changes them, which gives employees a stable coverage experience.

Here is where group plans hold a clear structural advantage over individual coverage:

- No medical underwriting. Group plans cannot deny coverage or charge more based on an employee’s health history. Individual plans outside the ACA marketplace can still use health status in some contexts.

- Dependent coverage. Group plans typically extend to spouses and children, often at rates below what the individual market charges for family plans.

- Employee retention. Offering group health benefits signals employer investment in workforce wellbeing, which directly affects hiring and retention outcomes.

- Tax advantages for the employer. Premium contributions are deductible as a business expense, reducing the net cost of offering coverage.

The one structural limitation worth noting: insurance carriers require minimum participation rates to maintain viable groups. If too few employees enroll, the carrier may increase premiums or decline to offer coverage. This is a real constraint for very small teams where several employees may already have coverage through a spouse.

What should small business owners consider when choosing a plan?

Choosing the right group health policy requires balancing your budget against your employees’ needs and your market’s expectations. Start with these practical steps:

- Confirm your eligibility. Most carriers require at least two enrolled employees to issue a group policy. Self-employed individuals without common-law employees typically cannot obtain a bona fide group plan and should explore alternatives like ICHRA (Individual Coverage Health Reimbursement Arrangement) instead.

- Evaluate plan types against your workforce. An HMO works well for employees concentrated in one geographic area. A PPO suits teams spread across multiple states. An HDHP with HSA contributions appeals to younger, lower-utilization employees who prioritize take-home pay.

- Set a realistic contribution budget. Decide what percentage of the employee-only premium you will cover before shopping plans. This number drives every other cost decision.

- Check participation thresholds. Before enrolling, survey employees on whether they would participate. A carrier requiring 70% participation on a 10-person team means you need at least seven enrollees to qualify.

- Communicate clearly during open enrollment. Employees who do not understand their options often default to the cheapest plan, which may not serve their actual healthcare needs. Clear, plain-language enrollment guides reduce confusion and increase satisfaction.

For self-employed owners without staff, the individual coverage options available in 2026 have expanded meaningfully, and an ICHRA can provide tax-advantaged reimbursements for individually purchased plans without requiring a group structure.

Pro Tip: Review your plan’s self-funded health plan options annually, not just at renewal. Carrier pricing shifts, and a plan that was the best value two years ago may no longer be competitive.

Key takeaways

Group health coverage lowers costs and increases access by pooling employee risk under one employer-sponsored policy, making it the most cost-effective coverage structure for small businesses with two or more enrolled employees.

| Point | Details |

|---|---|

| Risk pooling reduces premiums | Spreading risk across employees lowers individual costs by 20 to 30% versus individual market plans. |

| Employers share premium costs | Employers typically cover at least 50% of premiums, with many paying up to 80% to stay competitive. |

| Funding model affects flexibility | Level-funded plans offer refund potential and stop-loss protection suited to small employers. |

| Participation thresholds matter | Carriers require minimum enrollment rates; failing to meet them can raise premiums or void coverage. |

| Solo entrepreneurs need alternatives | Self-employed owners without employees should consider ICHRA as a tax-advantaged substitute for group plans. |

Why group health coverage is worth getting right the first time

I have worked with hundreds of small business owners who treated health benefits as an afterthought, something to figure out after hiring was done. That sequence almost always costs more in the long run. The business that offers a well-structured group plan from day one attracts better candidates, retains them longer, and spends less per employee on healthcare than the business scrambling to patch together individual plans for a growing team.

The funding model conversation is where most small employers leave money on the table. Fully insured plans are comfortable and familiar, but a level-funded plan for a healthy 10-person team can return thousands of dollars at year-end if claims stay low. That is not a theoretical benefit. I have seen it happen repeatedly for businesses in the $1 to $5 million revenue range where every dollar of operating cost matters.

The participation threshold issue catches more business owners off guard than any other factor. You can find the perfect plan at the right price, only to discover that three employees on spousal coverage drop your participation rate below the carrier’s minimum. Survey your team before you shop, not after. And if you are a solo operator without employees, stop trying to force a group structure that does not fit. An ICHRA gives you the tax advantages of employer-sponsored coverage without requiring a group. The private health insurance benefits available to business owners in 2026 are broader than most people realize, and the right broker will show you options you did not know existed.

— mkaravas1m

How Sageshieldassurance can help you find the right plan

Sageshieldassurance specializes in health insurance solutions built specifically for small business owners and self-employed individuals, not the one-size-fits-all packages designed for large corporations.

With partnerships across leading carriers and clients served in over 40 states, Sageshieldassurance guides you through plan selection, contribution modeling, and employee enrollment with the kind of hands-on support that most brokers reserve for enterprise accounts. Whether you are offering group health benefits to a team of five or exploring health insurance options as a solo entrepreneur, the team at Sageshieldassurance will match your budget to the right structure. Request a personalized consultation today and get a clear picture of what your coverage should actually cost.

FAQ

What is group health coverage in simple terms?

Group health coverage is a health insurance policy an employer purchases to cover employees under one shared plan, spreading risk across the group to lower individual premium costs. It typically includes the employee and can extend to dependents.

Who qualifies for group health coverage?

Employees who meet their employer’s eligibility criteria, such as working a minimum number of hours per week, qualify for group coverage after any applicable waiting period, which federal law caps at 90 days. Self-employed individuals without common-law employees generally do not qualify for a bona fide group plan.

How does group health insurance differ from individual coverage?

Group plans use risk pooling to lower premiums and require no medical underwriting, while individual plans price coverage based on age and can vary significantly year to year. Small businesses can save 20 to 30% per enrollee by choosing group coverage over individual market plans.

What are the main benefits of group health plans for small businesses?

Group health plans reduce per-employee premium costs, provide tax deductions on employer contributions, and support employee retention by offering a benefit that individual market coverage cannot match at the same price point.

Can a self-employed person get group health coverage?

A self-employed person with at least one common-law employee may qualify for a group plan, but sole proprietors without employees typically cannot. An ICHRA is the most practical alternative, allowing tax-advantaged reimbursements for individually purchased health coverage.

Leave a Reply