Why Offer Employee Health Benefits to Your Team

Offering employee health benefits is the single most effective investment a small business owner can make to attract skilled workers, reduce turnover, and build a productive team. Employer-sponsored health coverage, the formal industry term for what most people call “employee health benefits,” now covers over 180 million Americans and has become the standard expectation in the labor market. If you are weighing whether to add health coverage to your compensation package, the data and the business logic both point in the same direction.

Why offer employee health benefits to attract and keep talent

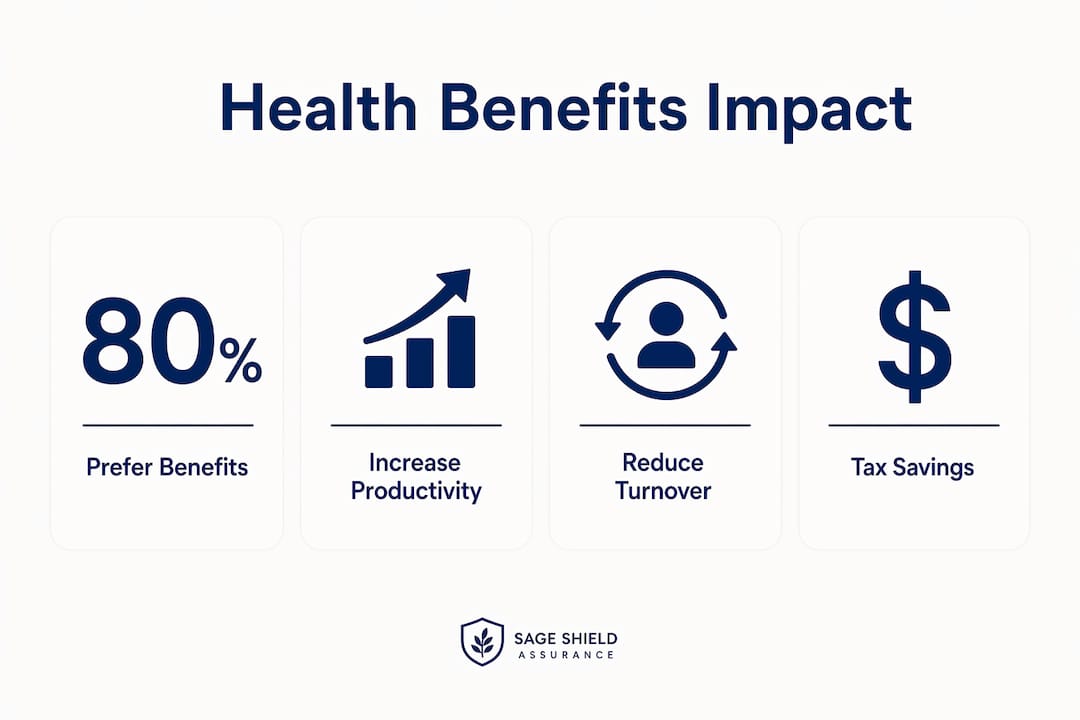

The competition for skilled workers is real, and health coverage is one of the clearest signals you can send to a candidate about how you value your team. 80% of employees prefer better benefits over a pay raise, which means a well-designed health plan can outperform a salary bump when it comes to attracting top candidates. That statistic reframes the entire cost conversation. You are not spending money on benefits instead of wages. You are spending it more efficiently.

The employee health insurance advantages extend well beyond the hiring stage. Workers who feel financially protected by their employer are less likely to leave. Replacing a single employee costs between 50% and 200% of their annual salary when you factor in recruiting, onboarding, and lost productivity. Health benefits reduce that churn directly. Strong benefits correlate with reduced turnover and lower recruitment costs because employees increasingly weigh benefits as equal to salary when deciding whether to stay.

Mental health coverage deserves specific attention here. Burnout and anxiety are leading causes of voluntary resignation in 2026, and workers who have access to mental health support through their employer are significantly more likely to stay long term. Offering a plan that includes behavioral health coverage is not a luxury add-on. It is a retention tool with measurable impact.

Key reasons health benefits improve talent outcomes:

- Workers with health coverage report higher job satisfaction and loyalty

- Mental health and wellness benefits reduce voluntary turnover

- 97% of employers already offer health coverage, making it a baseline expectation for candidates

- Benefits packages signal employer commitment, which strengthens your employer brand

How health benefits drive productivity and workplace morale

Access to preventive care is the mechanism that connects health benefits to daily productivity. Employees who can see a doctor regularly, manage chronic conditions, and address mental health concerns before they escalate miss fewer days and perform better when they are at work. Preventive care decreases sick days and reduces presenteeism, the costly pattern of employees showing up but working at reduced capacity due to untreated health issues.

Presenteeism is often invisible to small business owners, but its cost is not. A worker managing uncontrolled diabetes or untreated depression may be physically present while operating at 60% capacity. Health coverage that includes regular checkups, prescription access, and mental health visits addresses the root cause of that performance gap. The productivity gains from a well-used health plan are not theoretical. They show up in output, customer service quality, and team cohesion.

Pro Tip: Add a telemedicine option to your health plan. Employees are far more likely to address minor health issues early when they can consult a doctor from their phone, which prevents those issues from becoming serious and costly.

Morale is the less quantifiable but equally real benefit. When employees know their employer has invested in their physical and mental wellbeing, their sense of loyalty and motivation increases. That psychological shift reduces conflict, improves collaboration, and creates a workplace culture where people want to perform. The importance of health benefits to team morale is not just a soft metric. It translates directly into retention, referrals, and the quality of work your team delivers.

What are the financial advantages of offering health benefits?

The financial case for offering health coverage is stronger than most small business owners realize, largely because of tax incentives that go underused. The Small Business Health Care Tax Credit allows qualifying businesses to offset up to 50% of premium costs. To qualify, you generally need fewer than 25 full-time equivalent employees, pay average wages below a certain threshold, and purchase coverage through the Small Business Health Options Program (SHOP) marketplace. Many small business owners miss this credit entirely.

Beyond the tax credit, employer contributions to health premiums are fully tax-deductible as a business expense. That means every dollar you spend on employee coverage reduces your taxable income. The net cost of offering benefits is lower than the sticker price suggests, and that gap widens when you account for the retention savings described above.

| Financial advantage | What it means for your business |

|---|---|

| Small Business Health Care Tax Credit | Offsets up to 50% of premium costs for qualifying businesses |

| Tax-deductible premiums | Employer contributions reduce taxable business income |

| Risk pooling in group plans | Lowers per-person costs compared to individual market rates |

| Reduced turnover costs | Fewer replacements means lower recruiting and onboarding spend |

| Preventive care savings | Early treatment prevents expensive emergency and crisis care |

Group plans use risk pooling to spread costs across all enrolled employees, which eliminates individual medical underwriting and significantly reduces premiums. This is especially valuable for employees with pre-existing conditions, who would face much higher costs on the individual market. For a small business, offering a group plan means your team gets better coverage at a lower cost than they could access on their own.

Pro Tip: Work with a licensed broker to confirm whether your business qualifies for the Small Business Health Care Tax Credit before your next enrollment period. Many owners who qualify never claim it.

How to design an effective health benefits plan for a small business

Building a health benefits package that actually works requires more than picking the cheapest plan available. The goal is to align coverage with both your business objectives and your employees’ real needs. Here is a practical framework for getting it right:

- Define your goals first. Decide whether your primary objective is reducing turnover, improving productivity, or attracting a specific type of candidate. Your goal determines which plan features matter most.

- Offer plan options, not just one plan. A mix of a PPO for employees who want flexibility and an HDHP paired with a Health Savings Account for cost-conscious workers gives your team real choice without dramatically increasing your costs.

- Include telemedicine and mental health coverage. These two features have the highest utilization rates among working-age adults and deliver the clearest productivity returns.

- Communicate benefits clearly and repeatedly. Clear communication optimizes benefit usage and increases program ROI. A benefits package no one understands is a benefits package no one uses.

- Collect employee feedback annually. Survey your team each year to find out which benefits they use, which they do not, and what gaps they feel. Adjust accordingly.

- Use a broker to manage complexity. A qualified broker, such as those at Sageshieldassurance, can compare plans across multiple carriers, identify tax efficiencies, and handle the administrative burden of enrollment and renewals.

The benefits of employee health plans are maximized when the plan design reflects actual employee demographics. A team of younger workers may prioritize mental health and telemedicine. A team with older employees or families may prioritize low deductibles and broad specialist networks. Tailoring the plan to your workforce is what separates a benefits package that drives retention from one that sits unused.

Common pitfalls to avoid when offering health coverage

Most small business owners who struggle with health benefits make the same set of mistakes. Knowing them in advance saves you money and protects your team’s trust.

- Raising deductibles without support: High deductibles without access support lead employees to delay care, which turns manageable conditions into expensive crises. If you need to control costs, pair a high-deductible plan with an HSA contribution rather than simply cutting coverage.

- Failing to promote preventive care: Employees who do not know their plan covers annual physicals, screenings, and mental health visits will not use those benefits. Active communication about what is covered stabilizes claims and keeps premiums from rising.

- Choosing a plan based solely on premium cost: The cheapest plan often has the narrowest network and the highest out-of-pocket costs. Employees who cannot afford to use their coverage will not benefit from it, and you will not see the productivity or retention gains you are paying for.

- Ignoring the ROI measurement: Health benefits deliver measurable returns beyond medical claims. Track turnover rates, absenteeism, and employee satisfaction scores before and after implementing a plan to quantify the impact.

- Treating benefits as a one-time decision: Plans need annual review. Carrier pricing changes, employee needs shift, and new options like virtual care become available. A static plan loses value over time.

Key takeaways

Offering employee health benefits is a strategic business decision that reduces turnover, improves productivity, and delivers measurable tax and financial advantages for small business owners.

| Point | Details |

|---|---|

| Retention and recruitment | 80% of employees prefer better benefits over a pay raise, making health coverage a primary hiring tool. |

| Productivity gains | Preventive care access reduces absenteeism and presenteeism, improving daily output and team performance. |

| Tax efficiency | Qualifying small businesses can offset up to 50% of premium costs through the Small Business Health Care Tax Credit. |

| Risk pooling advantage | Group plans lower per-person costs and protect employees with pre-existing conditions from individual market pricing. |

| Communication is critical | Clear, repeated communication about benefits maximizes employee usage and the return on your investment. |

What I have learned from watching small businesses get this wrong

Most small business owners I have worked with approach health benefits as a cost to minimize rather than a tool to deploy. That mindset produces exactly the outcome they fear: a plan that is too limited to attract good candidates, too confusing for employees to use, and too expensive relative to the value it delivers.

The owners who get it right share one habit. They treat benefits as a management lever, not a line item. They ask: what do I want this plan to do for my business? And then they build toward that answer. One business owner I spoke with cut his annual turnover from 40% to 12% in two years simply by adding a solid PPO and a mental health benefit, then communicating both clearly at onboarding and in quarterly check-ins. His premium cost increased by roughly $8,000 per year. His recruiting and training savings exceeded $60,000.

The tax angle is also consistently overlooked. The Small Business Health Care Tax Credit exists specifically to make coverage affordable for businesses with fewer than 25 employees, yet a significant portion of qualifying owners never claim it. That is not a minor oversight. It is thousands of dollars left on the table annually.

My honest recommendation: do not design a benefits package alone. The plan options, carrier negotiations, and tax structures are genuinely complex. A broker who specializes in small business health coverage will find efficiencies you will not find on your own, and the cost of that guidance is almost always recovered in the first year.

— mkaravas1m

How Sageshieldassurance helps small businesses build the right plan

Small business owners who are ready to offer health coverage but unsure where to start will find a clear path forward with Sageshieldassurance. The team at Sageshieldassurance specializes in matching small businesses with tailored health insurance plans across leading carriers, handling the comparison work, enrollment logistics, and ongoing plan management that most owners do not have time to manage alone.

With over 500 families served across 40 states, Sageshieldassurance brings the kind of carrier relationships and plan knowledge that translate directly into better coverage at lower cost for your team. Their brokers also identify tax credit opportunities and structure plans to maximize your deductions. If you want to understand your brokerage options before committing to a plan, Sageshieldassurance offers a no-pressure review of your current situation and what coverage would realistically cost.

FAQ

Why should a small business offer health benefits?

Offering health coverage attracts better candidates, reduces employee turnover, and improves daily productivity through preventive care access. It also provides tax advantages, including fully deductible employer premium contributions and potential eligibility for the Small Business Health Care Tax Credit.

How do health benefits affect employee retention?

Employees view benefits as equal to salary when making decisions about whether to stay with an employer. Businesses that offer strong health coverage consistently report lower voluntary turnover rates compared to those that do not.

What is the Small Business Health Care Tax Credit?

The Small Business Health Care Tax Credit allows qualifying businesses with fewer than 25 full-time equivalent employees to offset up to 50% of health premium costs. Plans must be purchased through the SHOP marketplace to qualify.

Are group health plans cheaper than individual plans?

Group plans use risk pooling to spread costs across all enrolled employees, which eliminates individual medical underwriting and reduces per-person premiums. This makes group coverage significantly more affordable than individual market plans, particularly for employees with pre-existing conditions.

What is the biggest mistake small businesses make with health benefits?

The most common mistake is raising deductibles to cut costs without providing employee support, which causes workers to delay care and drives up crisis care expenses over time. Pairing a high-deductible plan with an HSA contribution is a more effective cost-control strategy.

Leave a Reply