What Is Whole Life Insurance? Your 2026 Guide

Whole life insurance is defined as a permanent life insurance policy that provides coverage for your entire life, as long as you pay your premiums. Unlike term policies that expire after 10, 20, or 30 years, whole life never lapses due to age or health changes. It combines a guaranteed death benefit with a cash value account that grows at a fixed, tax-deferred rate. For self-employed individuals, business owners, and anyone seeking financial certainty, understanding the full picture of whole life insurance, including its costs, mechanics, and trade-offs, is the foundation of a sound coverage decision.

What is whole life insurance and how does it work?

Whole life insurance works by splitting each premium payment between two destinations: the death benefit reserve and the cash value account. The death benefit is the guaranteed amount paid to your beneficiaries when you die. The cash value is a savings component that accumulates inside the policy over time.

Premiums in a whole life policy are level, meaning they are fixed at the time you buy the policy and never increase. This is a meaningful distinction from other insurance products where costs can rise as you age. A 35-year-old who locks in a policy today pays the same monthly amount at age 70.

The cash value grows at a fixed, guaranteed annual interest rate ranging from 1% to 3.5%, depending on the insurer and policy design. That growth is tax-deferred, meaning you owe no taxes on the gains while the money stays inside the policy. Once you have accumulated enough cash value, you can borrow against it through a policy loan, which is also tax-free as long as the policy remains in force.

Some whole life policies issued by mutual insurance companies, such as those from Northwestern Mutual or MassMutual, also pay annual dividends. These dividends are not guaranteed, but many participating policies have paid them consistently for decades. You can use dividends to reduce premiums, purchase additional coverage, or let them accumulate inside the policy.

Pro Tip: Ask your broker specifically how the policy is designed before you sign. A policy optimized for maximum death benefit will build cash value more slowly than one designed for accelerated cash accumulation. These are two very different products even if they carry the same label.

How much does whole life insurance cost?

Whole life premiums run 5 to 15 times higher than term life insurance for the same death benefit amount. That gap is real and significant, and it is the first number you need to understand before comparing policies.

The cost of whole life insurance depends primarily on your age, gender, health status, and how the policy is structured. Women typically pay 15 to 25% less than men of the same age because of longer average life expectancy. The table below shows representative monthly premiums for a $100,000 whole life policy for healthy, non-smoking applicants.

| Age | Male (monthly) | Female (monthly) |

|---|---|---|

| 30 | ~$105 | ~$85 |

| 40 | ~$150 | ~$120 |

| 50 | ~$220 | ~$175 |

| 60 | ~$324 | ~$255 |

Source: 2026 premium estimates for standard health class applicants.

For larger coverage amounts, the numbers scale proportionally. A healthy 40-year-old man pays approximately $5,524 per year for $500,000 in whole life coverage. That same coverage in a 20-year term policy would cost a fraction of that amount.

Policy design also drives cost in ways most buyers never see. A policy built to maximize the death benefit allocates most of your premium toward the insurance component, leaving less to grow as cash value. A policy designed for cash accumulation does the opposite. How premiums are allocated between these two functions is more influential on long-term performance than the premium amount itself, yet most agents do not walk buyers through this distinction clearly.

Payment structures add another layer. Limited-pay policies let you finish paying premiums in 10 or 20 years while keeping coverage for life. Premiums-to-100 policies spread payments across your entire lifetime at a lower monthly amount. Limited-pay costs more per month but eliminates the obligation in a defined window, which appeals to business owners with predictable income peaks.

Pro Tip: Compare the total premium paid over 20 years, not just the monthly number. A lower monthly premium on a premiums-to-100 structure often costs more in total dollars than a 20-pay policy.

Benefits and drawbacks of whole life insurance

Whole life insurance offers a specific set of advantages that no other insurance product replicates exactly. It also carries real limitations that make it the wrong choice for many buyers.

The core benefits:

- Lifetime coverage. The policy never expires. Your beneficiaries receive the death benefit whether you die at 55 or 95.

- Fixed premiums. Your monthly cost is locked in at issue and never increases, regardless of health changes or age.

- Tax-deferred cash value growth. The savings component grows without annual tax liability, and policy loans are tax-free as long as the policy stays in force.

- Tax-free death benefit. Beneficiaries receive the payout free of income tax under IRS rules.

- Dividend potential. Participating policies from mutual insurers may pay annual dividends that increase the policy’s value over time.

The real drawbacks:

- High cost. The premium gap versus term life is substantial, especially in the early years when cash value is minimal.

- Slow cash value growth. A guaranteed rate of 1% to 3.5% lags behind what a diversified investment portfolio might return over the same period.

- Complexity. Policy riders, dividend options, loan provisions, and surrender charges create layers of detail that require careful review.

- Surrender charges. Canceling a whole life policy in the first several years often results in receiving less than you paid in.

The most common misunderstanding about whole life is treating it as a primary investment vehicle. Whole life should be viewed as lifetime protection with a savings element attached, not as a wealth-building strategy. For most buyers, the decision comes down to whether the certainty of lifetime coverage justifies the higher cost compared to term insurance.

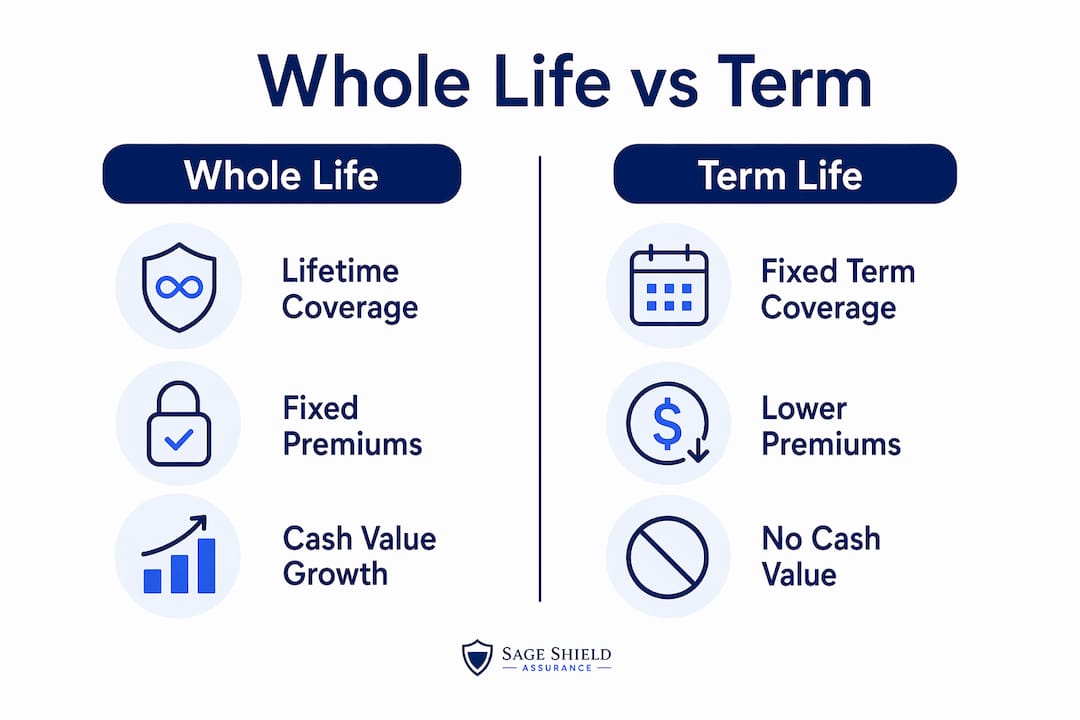

Whole life vs. term life insurance: which one fits your situation?

Term life and whole life share several features: fixed premiums, medical underwriting at purchase, and a guaranteed death benefit. The differences, however, are fundamental.

| Feature | Whole life | Term life |

|---|---|---|

| Coverage duration | Lifetime | 10, 20, or 30 years |

| Premium level | Fixed, higher | Fixed, lower |

| Cash value | Yes, grows tax-deferred | No |

| Dividends | Possible (participating policies) | No |

| Conversion option | N/A | Often available |

| Best for | Permanent needs, estate planning | Temporary income replacement |

Term life is the right tool when your coverage need has a defined end point. Paying off a mortgage, replacing income until children are independent, or covering a business loan are all temporary obligations. Whole life fits when the need is permanent: funding a special needs trust, covering estate taxes, or leaving a guaranteed inheritance.

One feature worth knowing: many term policies include a conversion rider that lets you switch to a whole life policy later without a new medical exam. This matters if your health changes and you want permanent coverage down the road. Buying a term policy with a conversion rider now gives you flexibility without locking in the higher whole life premium today.

Pro Tip: Before choosing between whole life and term, write down your specific financial obligations and their time horizons. If every item on that list has an end date, term life is almost certainly the better fit.

Who should get whole life insurance?

Whole life insurance provides peace of mind for individuals who need certainty that coverage will never expire, regardless of how long they live. That need is more specific than most people assume.

The following situations genuinely favor whole life over term:

- Parents of children with lifelong disabilities. A special needs dependent may require financial support indefinitely. A whole life policy guarantees funds will be available regardless of when the parent dies.

- Estate planning for high-net-worth individuals. Whole life can fund estate taxes or equalize inheritances among heirs without forcing the sale of assets.

- Business owners with permanent obligations. Buy-sell agreements and key person coverage sometimes require permanent insurance that cannot lapse.

- Individuals who have maxed out tax-advantaged accounts. Once 401(k) and IRA contributions are at their limits, the tax-deferred cash value in a whole life policy offers an additional sheltered savings vehicle.

- Those who want forced savings with guaranteed growth. For buyers who struggle to invest consistently, the mandatory premium structure creates discipline that a brokerage account does not.

Whole life is generally not the right fit for young families on tight budgets who need maximum death benefit coverage at the lowest possible cost. In those cases, a 20-year or 30-year term policy delivers far more coverage per dollar. Sageshieldassurance works with clients across both categories, matching the right product to the actual financial need rather than defaulting to one type.

Key takeaways

Whole life insurance is the right choice only when your coverage need is permanent and the higher premium cost is justified by specific financial goals.

| Point | Details |

|---|---|

| Permanent coverage guarantee | Whole life never expires, unlike term policies that end after a set period. |

| Fixed premiums for life | Your rate is locked at purchase and never increases due to age or health. |

| Tax-deferred cash value | Growth inside the policy is sheltered from taxes; loans against it are also tax-free. |

| Cost is significantly higher | Premiums run 5 to 15 times more than comparable term life coverage. |

| Policy design matters most | How premiums are split between death benefit and cash value determines long-term performance. |

Why I think most people misread whole life insurance

Most of the confusion I see around whole life comes from buyers comparing it to the wrong benchmark. They hear “cash value” and immediately start measuring it against a stock portfolio or a Roth IRA. That comparison almost always makes whole life look bad, and in that narrow frame, it often is.

But that is not the right question. The right question is: do you need coverage that cannot expire? If the answer is yes, the comparison is not whole life versus the S&P 500. The comparison is whole life versus the risk of dying without coverage because your term policy ran out.

Where I see whole life genuinely misused is when agents sell it to 28-year-olds with young children and limited income as a primary savings strategy. The cash value in those early years is minimal, the premiums are a significant budget burden, and the family would be far better protected by a $1 million 30-year term policy at a fraction of the cost. The “buy term and invest the difference” argument is not a cliché. For most working families, it is the correct answer.

Whole life earns its place in a financial plan when the need is specific: estate liquidity, permanent dependent support, or supplemental tax-sheltered savings for someone who has already maxed out every other option. Outside of those scenarios, I would push back hard on any recommendation that leads with whole life as the default choice.

— mkaravas1m

How Sageshieldassurance helps you choose the right policy

Choosing between whole life and term insurance is not a product decision. It is a financial planning decision that requires an honest look at your obligations, timeline, and budget.

Sageshieldassurance specializes in exactly this kind of analysis for self-employed individuals and business owners across 40 states. The team reviews your full financial picture, compares policies from multiple leading carriers, and explains the trade-offs in plain language before you sign anything. Whether you need permanent coverage for estate planning or a cost-effective term policy for income replacement, Sageshieldassurance builds the solution around your actual needs. Start with a personalized insurance consultation or explore the full range of life and health insurance services available to you today.

FAQ

What is the whole life insurance definition in simple terms?

Whole life insurance is a permanent life insurance policy that covers you for your entire life, pays a guaranteed death benefit to your beneficiaries, and builds a cash value account that grows at a fixed tax-deferred rate.

Is whole life insurance worth it for most people?

Whole life is worth it for individuals with permanent coverage needs, such as estate planning, lifelong dependents, or supplemental tax-sheltered savings. For most families needing income replacement, term life delivers more coverage at a lower cost.

How does cash value work in a whole life policy?

A portion of each premium goes into a cash value account that grows at a guaranteed rate of 1% to 3.5% annually. You can borrow against this balance tax-free while the policy remains active.

What is the biggest difference between whole life and term life?

Term life covers a set period and has no cash value. Whole life covers your entire life, builds cash value, and costs significantly more, typically 5 to 15 times the premium of a comparable term policy.

Can I switch from term life to whole life later?

Many term policies include a conversion rider that allows you to convert to a whole life policy without a new medical exam, giving you flexibility if your health or financial situation changes.

Leave a Reply