What Is Supplemental Health Insurance? Your 2026 Guide

Supplemental health insurance is defined as a secondary policy that pays cash benefits directly to you when specific health events occur, rather than paying your doctors or hospitals. These benefits fill the financial gaps your primary plan leaves open, including deductibles, copayments, coinsurance, and costs that have nothing to do with medical bills at all. Providers like Cigna, Anthem, and Guardian each offer distinct supplemental products built around accident coverage, critical illness, and hospital stays. If you carry a high-deductible health plan or worry about what happens to your income during a serious illness, supplemental health coverage is worth understanding in detail.

What is supplemental health insurance and how does it work?

Supplemental insurance pays cash directly to you for certain covered events, not to your medical providers. That distinction matters more than most people realize. Your primary health plan negotiates rates and pays hospitals. Your supplemental plan sends money to your bank account when a trigger event happens.

The trigger is everything. A hospital indemnity plan might pay you $300 per day you spend admitted to a hospital. An accident plan might pay a lump sum the moment you fracture a bone. A critical illness plan might send you $25,000 the day your oncologist confirms a cancer diagnosis. Each plan defines its own list of covered events, and benefits only flow when those specific events occur.

Benefits cover medical and nonmedical costs alike. You can use the cash to pay your deductible, cover a copay, hire a babysitter while you recover, or make a car payment you would have missed because you were out of work. No receipts required. No provider billing. The money is yours to use as you see fit.

Pro Tip: Supplemental insurance is not a replacement for primary coverage. It works alongside your existing plan. Never cancel your primary policy expecting a supplemental plan to carry the full load.

Supplemental plans are also available as voluntary employer benefits, often structured under a Section 125 Cafeteria Plan. That structure lets employees pay premiums with pre-tax dollars, which lowers their taxable income. Small businesses can offer these plans without adding payroll cost, which makes them a practical option for both sides of the employment relationship.

What are the main types of supplemental health insurance?

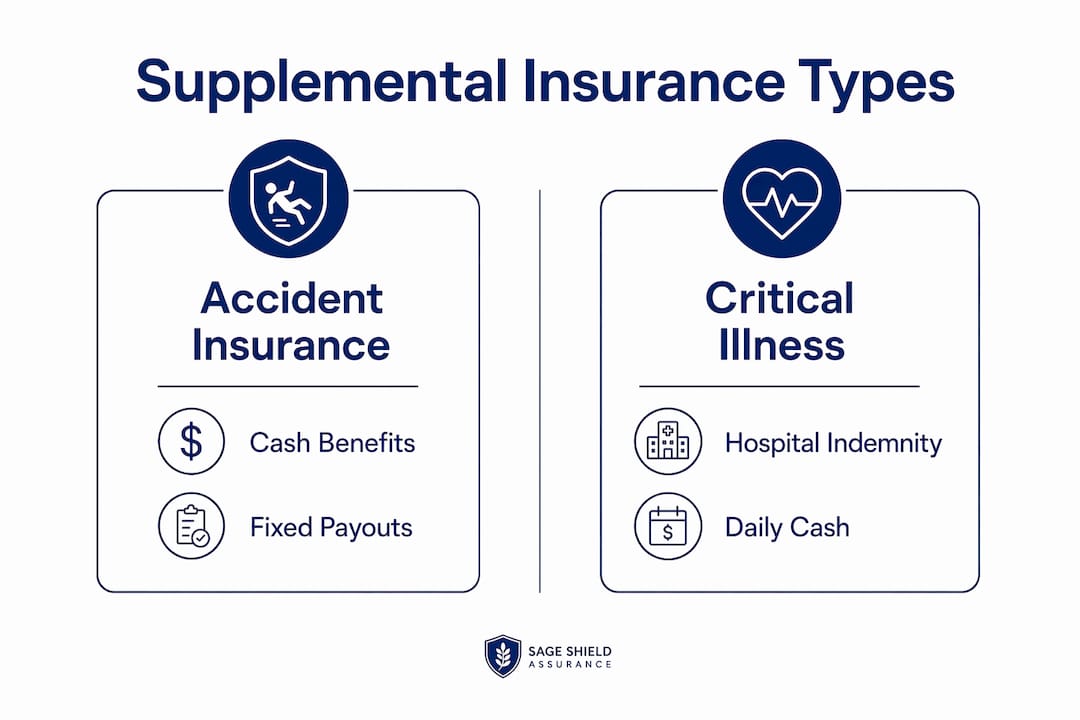

Three plan types dominate the supplemental market: accident insurance, critical illness insurance, and hospital indemnity insurance. Each targets a different financial risk, and each pays benefits differently.

| Plan Type | Trigger Event | Payout Structure | Best For |

|---|---|---|---|

| Accident insurance | Injury from a covered accident | Lump sum or scheduled benefit | Active individuals, families with children |

| Critical illness insurance | Diagnosis of cancer, stroke, or heart attack | Lump sum | Anyone with family history of serious illness |

| Hospital indemnity insurance | Hospital admission or per-day stay | Fixed daily or per-admission amount | Those with frequent hospitalization risk |

Accident insurance

Accident insurance pays fixed cash benefits for injuries caused by covered accidents. Covered events typically include fractures, dislocations, burns, and emergency room visits. The benefit schedule lists a dollar amount for each type of injury. A broken arm might pay $1,500. A torn ligament might pay $800. The plan does not reimburse your actual medical bill. It pays the scheduled amount regardless of what treatment costs.

Critical illness insurance

Cancer treatment can reach $150,000 in total costs, even with primary insurance in place. Critical illness insurance addresses that gap with a lump-sum payment triggered by a qualifying diagnosis. That payment can cover treatment costs, experimental therapies not covered by your primary plan, or simply the mortgage payments you cannot miss while you are in chemotherapy. The lump sum arrives at diagnosis, not after treatment ends.

Hospital indemnity insurance

Hospital indemnity plans pay a fixed amount for each day you spend in the hospital, or a flat amount per admission. The daily benefit might be $200 or $500 depending on your plan. If you spend five days admitted after surgery, a $300 per day plan pays you $1,500. That cash can offset your deductible, cover meals for your family, or replace a portion of lost wages. The payment is not tied to your actual hospital bill.

How does Medicare supplement insurance differ from other plans?

Medicare supplement insurance, formally called Medigap, occupies a specific and separate category. Medigap helps pay cost-sharing under Original Medicare Parts A and B, including copayments, coinsurance, and deductibles that Medicare leaves unpaid. It is not a cash benefit plan in the same sense as accident or critical illness insurance. It functions more like a secondary payer that settles the bill after Medicare pays its share.

The critical limitation most people miss: Medigap does not work with Medicare Advantage plans. If you are enrolled in Medicare Advantage, you cannot use a Medigap policy. The two systems are incompatible. This is a decision point that locks in your supplemental options based on which Medicare path you choose.

Some Medigap policies go beyond standard Medicare coverage. Certain plans cover emergency care during foreign travel, a benefit Original Medicare does not provide. That makes Medigap relevant for retirees who travel internationally and want protection outside U.S. borders.

The right supplemental choice for a Medicare beneficiary depends entirely on whether they carry Original Medicare or Medicare Advantage. Getting that base plan decision right first determines which supplemental products are even available to you.

Who should consider supplemental health insurance?

Supplemental coverage shifts from optional to necessary for people with high-deductible health plans. An HDHP keeps monthly premiums low but exposes you to thousands of dollars in out-of-pocket costs before coverage kicks in. A supplemental plan can pay cash to cover that deductible gap without requiring you to drain savings.

The financial case is strongest in these situations:

- You carry an HDHP with a deductible above $2,000 and limited savings to cover it.

- You are self-employed and a hospital stay would disrupt your income with no employer sick pay to fall back on.

- Your family has a documented history of cancer, heart disease, or stroke, making a critical illness diagnosis statistically more likely.

- You have dependents whose care would require paid help if you were hospitalized or recovering at home.

- Your primary plan has significant coinsurance obligations after the deductible, meaning your costs continue well past the deductible threshold.

Self-employed individuals face a compounded risk. They carry their own insurance costs, have no employer sick pay, and often cannot stop working without immediate financial consequences. A critical illness or hospital indemnity plan provides a cash buffer that keeps the business running while they recover.

Pro Tip: Before buying any supplemental plan, list your current plan’s deductible, out-of-pocket maximum, and coinsurance rate. Then compare those numbers against the benefit amounts in the supplemental plan. If the benefits do not meaningfully offset your actual exposure, the plan may not be worth the premium.

One common misconception is that supplemental insurance covers everything your primary plan does not. It does not. Supplemental policies have exclusions and eligibility limits. They cover specific named events. A hospital indemnity plan will not pay if you receive outpatient treatment. An accident plan will not pay for illness-related injuries. Reading the benefit trigger language before you buy is not optional. It is the only way to know whether the plan actually covers your risk.

Key Takeaways

Supplemental health insurance pays cash benefits directly to you for specific covered events, filling the financial gaps your primary plan cannot close.

| Point | Details |

|---|---|

| Cash goes to you, not providers | Benefits are paid directly to you and can cover medical or nonmedical expenses during recovery. |

| Three core plan types | Accident, critical illness, and hospital indemnity plans each target different financial risks with different payout structures. |

| Medigap is Medicare-specific | Medigap works only with Original Medicare and cannot be combined with Medicare Advantage plans. |

| HDHPs create the strongest case | People with high-deductible plans face the largest out-of-pocket exposure and benefit most from supplemental coverage. |

| Read the trigger language | Two plans with the same name can pay very differently. Benefit triggers and exclusions determine real-world value. |

Why I think most people buy supplemental insurance wrong

Most people shop supplemental plans the same way they shop primary insurance: they look at the premium and the plan name, then pick the cheapest option. That approach fails almost every time.

The plan name tells you almost nothing. Two hospital indemnity plans from different carriers can have completely different covered events, waiting periods, and payout conditions. One might pay on day one of admission. Another might require a three-day stay before any benefit triggers. That difference is worth hundreds of dollars in a real claim scenario, and it is buried in the benefit schedule most people never read.

The smarter approach is to start with your actual financial exposure. Pull your primary plan’s summary of benefits. Write down your deductible, your out-of-pocket maximum, and your coinsurance percentage. Then ask: which of these numbers would hurt me most if I hit them tomorrow? That answer tells you which type of supplemental plan to prioritize and how much benefit you actually need.

Guardian’s guidance on supplemental insurance makes a point worth repeating: the flexibility of cash benefits is the product’s real value. You are not buying reimbursement. You are buying financial stability during a period when your income may drop and your expenses may spike simultaneously. That framing changes how you evaluate every plan you consider.

The people I see get the most value from supplemental coverage are those who treat it as a targeted financial tool, not a catch-all safety net. They know exactly which event they are insuring against, exactly how much the plan pays when that event happens, and exactly how that payment maps to their real out-of-pocket risk. That level of clarity is achievable. It just requires reading the contract before signing it.

— mkaravas1m

How Sageshieldassurance helps you find the right supplemental plan

Choosing between accident, critical illness, and hospital indemnity coverage is not a one-size-fits-all decision. The right plan depends on your primary coverage, your financial exposure, and your personal health risks.

Sageshieldassurance works with self-employed individuals and business owners across 40 states to match supplemental plans to real coverage gaps. The team reviews your existing health insurance coverage alongside your financial situation and recommends plans that pay meaningful benefits when you need them. With partnerships across leading carriers, Sageshieldassurance compares benefit triggers, payout structures, and premium costs so you are not left guessing. If you want a clear picture of where your coverage falls short and which supplemental plan closes that gap, Sageshieldassurance is built for exactly that conversation.

FAQ

What does supplemental health insurance cover?

Supplemental health insurance covers specific events like accidents, critical illness diagnoses, and hospital stays by paying fixed cash benefits directly to you. Benefits can be used for medical costs, lost income, transportation, or any other expense during recovery.

Does supplemental insurance cover medications?

Standard supplemental plans like accident, critical illness, and hospital indemnity insurance do not cover prescription medications. Medication coverage falls under your primary health plan or a separate prescription drug plan.

How much does supplemental health insurance cost?

Premiums vary by plan type, benefit amount, age, and carrier. Individual plans are generally affordable relative to primary coverage, but the cost is not publicly listed as a standard rate since it depends on personal underwriting factors.

Can I have supplemental insurance with any primary health plan?

Most supplemental plans work alongside any primary health insurance, including employer-sponsored plans and individual market plans. Medigap is the exception: it works only with Original Medicare and cannot be paired with Medicare Advantage.

Is supplemental health insurance worth it for self-employed people?

For self-employed individuals with high-deductible plans and no employer sick pay, supplemental coverage provides a direct cash benefit during illness or injury that can protect both personal finances and business continuity.

Leave a Reply