What Is Accident Insurance Coverage? Your 2026 Guide

Accident insurance coverage is a supplemental cash-benefit policy that pays you a fixed dollar amount when a covered accidental injury occurs, regardless of what your health insurance pays. Unlike major medical insurance, which reimburses hospitals and providers for actual bills, accident insurance sends money directly to you based on a predetermined benefit schedule. Providers like MetLife and Guardian have offered these plans for decades, and they remain one of the most practical tools for managing the financial gap that even good health insurance leaves behind. For self-employed individuals and small business owners without employer-sponsored benefits, this coverage can be the difference between a manageable setback and a serious financial disruption.

What is accident insurance coverage and how does it work?

Accident insurance pays predetermined cash benefits based on a benefit schedule, not actual medical bill reimbursement. That distinction matters more than most people realize. When you break your wrist, your health insurer negotiates with the hospital and covers a portion of the bill. Your accident insurer, by contrast, looks at your policy’s schedule, sees “wrist fracture: $500,” and sends you $500 in cash. You spend it however you need to.

The claim process is straightforward. You file a claim with documentation proving the qualifying accident event occurred and that your injury matches a covered benefit category. Some employer-offered plans process claims within approximately 10 business days after receiving complete information, with payment delivered by check or electronic transfer. Many plans also carry no waiting period, meaning coverage begins the day your policy is active.

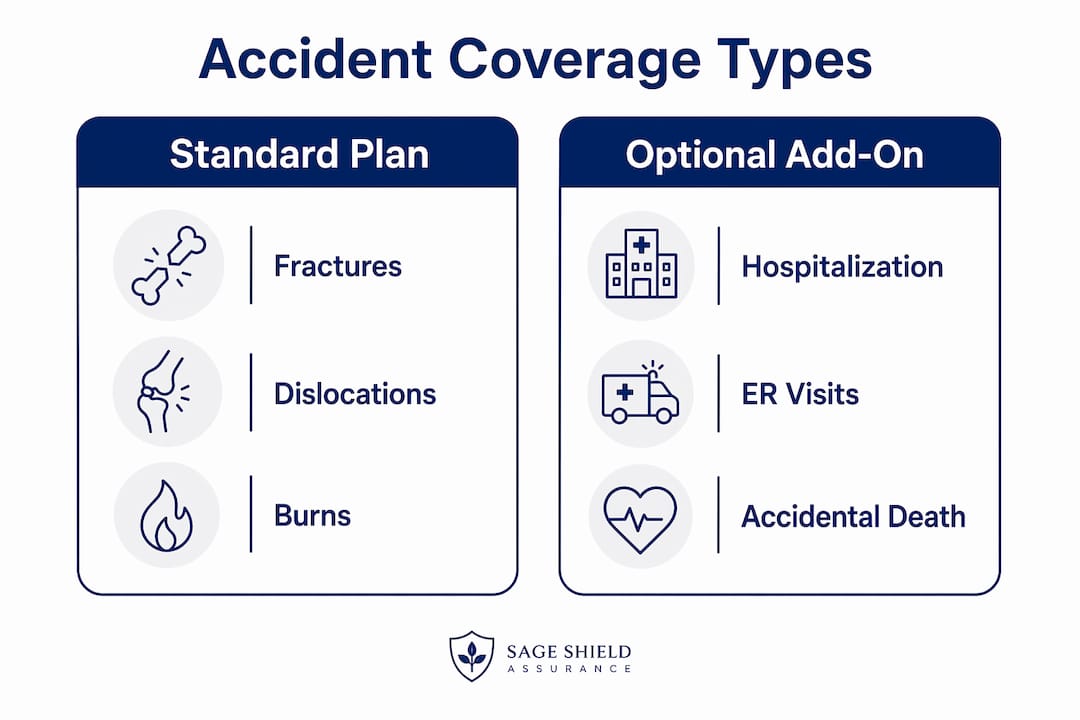

Here is what a typical benefit schedule covers:

- Fractures and dislocations: Fixed payouts per bone or joint, scaled by severity

- Burns: Tiered benefits based on burn degree and body surface area affected

- Emergency room visits: A flat benefit triggered by any covered ER admission

- Hospitalization: A daily or per-admission benefit for inpatient stays

- Ambulance transport: Reimbursement for ground or air ambulance services

- Accidental death and dismemberment (AD&D): A lump-sum benefit paid to you or your beneficiary

Pro Tip: Always request the full benefit schedule before purchasing a plan. Two policies with identical premiums can have dramatically different payout amounts for the same injury. Compare the fracture and hospitalization lines specifically, since those are the most commonly triggered benefits.

Types of accident coverage and what each benefit pays

Common covered events include fractures, dislocations, burns, ER visits, hospitalization, and accidental death or dismemberment, with coverage applying strictly to sudden bodily injuries from accidents rather than illness. Standard accident insurance packages these into a core benefit tier, but the real value often comes from optional add-ons that extend protection into areas most people overlook.

The table below compares what standard coverage typically includes versus the add-ons worth considering:

| Coverage type | Standard plan | Optional add-on |

|---|---|---|

| Fractures and dislocations | Yes, fixed schedule | Higher benefit tiers available |

| Burns | Yes, tiered by severity | Rarely enhanced |

| ER visit benefit | Yes, flat amount | Sometimes bundled with hospitalization |

| Hospitalization (daily) | Yes | Extended duration riders |

| Ambulance transport | Sometimes | Ground and air reimbursement |

| Temporary disability payments | No | Up to 104 weeks of weekly benefits |

| Home modification coverage | No | Available with select carriers |

| AD&D benefit | Often included | Higher face amounts available |

The temporary disability add-on deserves special attention for small business owners. If you are a sole proprietor and a serious accident keeps you off the job for three months, your revenue stops. A weekly disability benefit from your accident policy does not replace full income, but it covers fixed overhead costs like rent, utilities, and loan payments while you recover.

Pro Tip: If you run a business where physical work is central, such as construction, landscaping, or personal training, prioritize the temporary disability and hospitalization add-ons over the base fracture schedule. The daily cost of being unable to work almost always exceeds the one-time cost of a broken bone.

What accident insurance does not cover

Accident insurance policies exclude coverage for illness, certain hazardous activities, and injuries not caused by a sudden accident. This is the section of the policy most people skip, and it is the section that generates the most claim disputes.

The most common exclusions across carriers include:

- Illness and disease: Any injury or condition with a medical cause rather than an accidental one is excluded. A heart attack that causes a fall is typically not covered because the underlying event was medical.

- Intentional self-injury: No carrier covers self-inflicted harm.

- War and civil unrest: Injuries sustained in war-like situations or military conflict are universally excluded.

- High-risk and hazardous activities: Rock climbing, skydiving, motorcycle racing, and similar activities are excluded by most standard plans unless you purchase a specific rider or choose a carrier that covers them.

- Injuries under the influence: Many policies exclude accidents that occur while the policyholder is intoxicated or under the influence of non-prescribed substances.

Reading the hazardous activities and exclusion clauses closely is critical because policies differ widely on what counts as a covered accident. One carrier may exclude all motorized sports; another may cover recreational motorcycling but not racing. If your lifestyle or business involves physical risk, match the exclusion language to your actual activities before signing.

How accident insurance compares to health insurance

Accident insurance and health insurance solve different problems, and confusing the two leads to coverage gaps. Accident insurance pays fixed amounts regardless of actual medical spend, so there is no conflict or double-dipping concern with your health insurance reimbursements. You can collect from both policies for the same event.

| Feature | Accident insurance | Health insurance |

|---|---|---|

| Payment type | Fixed cash benefit to you | Reimbursement to providers |

| Triggers | Covered accident event | Any covered medical service |

| Illness coverage | No | Yes |

| Deductibles | None on benefits paid | Yes, often $1,000 to $7,000+ |

| Use of funds | Unrestricted | Applied to medical bills only |

| Replaces health insurance | No | Core medical coverage |

Accident insurance works alongside health insurance to cover gap costs such as deductibles and copays, with cash benefits paid directly to policyholders. That cash can also cover household bills, childcare, or lost wages during recovery. For self-employed individuals who carry high-deductible health plans to keep monthly premiums manageable, accident insurance is a practical way to pre-fund the deductible exposure without raising the cost of the primary plan. Comprehensive health insurance plans often leave significant out-of-pocket expenses from accidents that accident coverage can address directly. Accident insurance is supplemental by design. It is not a replacement for major medical coverage, and no responsible broker should position it that way.

How to choose the right accident insurance plan

Selecting the right plan requires more than comparing premiums. The benefit schedule, exclusion language, and claim process efficiency all determine whether a policy actually pays when you need it.

-

Assess your risk profile. A freelance graphic designer and a self-employed electrician face very different accident probabilities. Identify the injuries most likely to affect your work and confirm they appear on the benefit schedule with meaningful payout amounts.

-

Read the benefit schedule line by line. Accident insurance value depends heavily on selecting coverage that matches your typical accident risks. A policy that pays $200 for a fracture is not the same as one that pays $1,500, even if the monthly premium is similar.

-

Evaluate the insurer’s claim process. Ask specifically about average claim processing time and documentation requirements. Carriers like MetLife publish their claim timelines publicly. Slower or opaque processes create real hardship when you are injured and waiting on funds.

-

Add optional riders strategically. Review the add-ons available and select only those that match your actual exposure. A temporary disability rider is high value for a business owner with fixed monthly overhead. It adds less value for someone with substantial savings or a working spouse.

-

Integrate with your existing health plan. Check your current health plan’s deductible and out-of-pocket maximum. Structure your accident insurance benefit schedule so that the combined payouts from a major covered event would cover at least your annual deductible. For guidance on pairing accident coverage with private health plans, the private health insurance guide for business owners at Sageshieldassurance is a practical starting point.

-

Document everything from day one. Incomplete documentation is a leading cause of claim denial. Keep medical records, accident reports, and treatment receipts organized from the moment an injury occurs.

Key takeaways

Accident insurance coverage pays fixed cash benefits directly to you for covered injuries, and its real value lies in filling the financial gaps that health insurance leaves open.

| Point | Details |

|---|---|

| Fixed cash benefit model | Payouts are based on a benefit schedule, not actual medical bills, and go directly to you. |

| Supplements health insurance | Use accident payouts to cover deductibles, copays, and household costs during recovery. |

| Exclusions define real coverage | Illness, hazardous activities, and non-accidental injuries are typically excluded. |

| Optional riders add critical value | Temporary disability and ambulance add-ons matter most for self-employed individuals. |

| Documentation prevents denial | Matching your claim to a specific benefit category with full documentation is required for payment. |

Why I think most people buy accident insurance wrong

Most people treat accident insurance as a checkbox. They see it offered during open enrollment, pick the cheapest tier, and assume they are covered. That approach almost guarantees disappointment when a claim actually happens.

The policies I have seen cause the most frustration are the ones where the benefit schedule was never read. Someone breaks a collarbone, files a claim, and receives $150 because they chose a plan with a minimal fracture benefit. They assumed “covered” meant “well covered.” It does not. Accident insurance is an indemnity product, meaning its value is entirely defined by the specific numbers in the schedule you agreed to.

The second mistake I see constantly is buying accident insurance as a substitute for a real health plan. This is especially common among self-employed individuals trying to cut monthly costs. Accident insurance does not cover illness, does not pay for routine care, and does not satisfy ACA requirements. It is a supplement, not a foundation.

What actually works is treating accident insurance the way a good financial planner treats any risk tool: match the coverage to the specific exposure. If you work with your hands, price out the temporary disability rider. If you carry a $5,000 deductible on your health plan, find an accident policy whose combined fracture and hospitalization benefits get you close to that number. That is the calculation that makes accident insurance genuinely useful rather than just technically present.

— mkaravas1m

How Sageshieldassurance can help you find the right plan

Sageshieldassurance specializes in matching self-employed individuals and small business owners with supplemental coverage that actually fits their lives. With over 500 families served across 40 states, the team at Sageshieldassurance reviews benefit schedules, exclusion clauses, and claim processes across multiple carriers so you do not have to decode policy language alone. Whether you need a standalone accident plan or want to pair it with a broader health strategy, explore your accident and health coverage options to see what fits your budget and risk profile. For a deeper look at how supplemental coverage works alongside primary health plans, the trusted brokerage guide walks through the selection process step by step.

FAQ

What is accident insurance coverage in simple terms?

Accident insurance coverage is a supplemental policy that pays you a fixed cash amount when you are injured in a covered accident. The payout is based on a benefit schedule and goes directly to you, not to your doctor or hospital.

Is accident insurance necessary if I already have health insurance?

Accident insurance is not required, but it fills real gaps. Health insurance covers medical bills; accident insurance pays you cash that can cover deductibles, copays, lost income, or household expenses during recovery.

What does accident insurance typically not cover?

Most policies exclude illnesses, injuries from high-risk activities like skydiving or racing, intentional self-harm, and injuries sustained during war or civil unrest. Exclusions vary by carrier, so reading the policy language before purchasing is critical.

How much does accident insurance cost?

Premiums vary by carrier, benefit schedule, and optional riders selected, but individual plans are generally affordable relative to the coverage provided. Adding riders like temporary disability or extended hospitalization increases the monthly cost but can significantly raise the payout in a serious accident.

Can I collect from both accident insurance and health insurance?

Yes. Accident insurance pays fixed benefits regardless of what your health insurer covers, so there is no double-dipping conflict. You can receive both a health insurance reimbursement and an accident insurance cash benefit for the same event.

Leave a Reply