What Is a Self Funded Health Plan for Small Businesses

A self-funded health plan is an employer-financed arrangement where the business pays employee medical claims directly, instead of paying fixed premiums to an insurance carrier. Known formally as a self-insured plan, this model shifts financial risk from the insurer to the employer, giving business owners far more control over healthcare spending. Most self-funded plans still contract with insurance carriers or third-party administrators (TPAs) to handle day-to-day claims processing and provider networks. Federal regulations, including ERISA and the Affordable Care Act, govern these plans rather than state insurance mandates.

What is a self-funded health plan and how does it work?

A self-funded insurance plan operates on a straightforward premise: the employer sets aside money to pay medical claims as they arise, rather than prepaying a fixed premium to an insurer each month. When an employee visits a doctor or hospital, the employer pays those claims directly from its own funds or a dedicated claims account. The TPA or insurance carrier handles the administrative side, including processing claims, maintaining provider networks, and issuing ID cards.

Two funding structures exist within self-funded plans:

- Funded plans hold assets in a separate trust or claims reserve account, which triggers specific ERISA reporting requirements including Form 5500 filing.

- Unfunded plans pay claims directly from the employer’s general operating assets, which can simplify setup but increases cash flow exposure.

Historically, large corporations with thousands of employees dominated self-funded arrangements because they could absorb the financial variability of claims. That picture has shifted. Small businesses and self-employed individuals are increasingly exploring self-funded and hybrid options, particularly as premium costs for fully insured plans have climbed year over year. A growing middle ground called level-funded plans blends self-funding mechanics with predictable monthly payments, making the model more accessible to smaller employers.

Pro Tip: Ask any TPA you evaluate whether they offer real-time claims data dashboards. Transparent claims reporting is one of the biggest practical advantages of self-funding, and not every administrator delivers it equally.

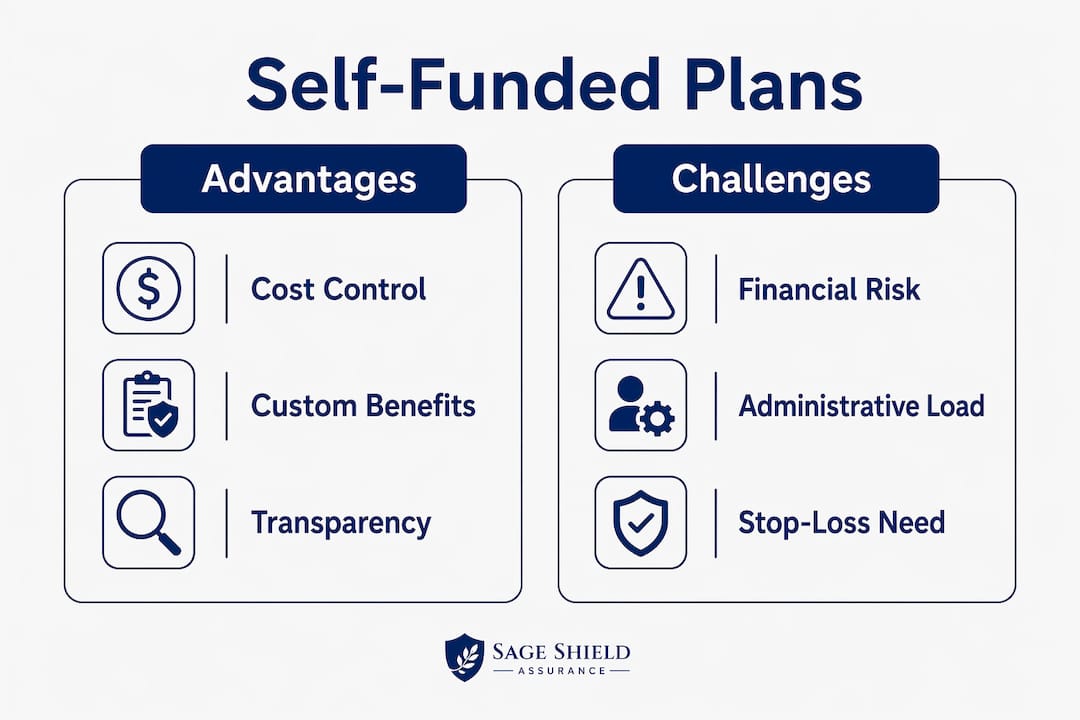

What are the advantages of self-funded health plans?

The advantages of self funding are most visible in three areas: cost structure, plan design flexibility, and data access.

-

Direct cost savings. With a fully insured plan, your premium includes the insurer’s administrative costs, profit margin, and risk loading. Self-funded plans eliminate that markup. If your workforce is relatively healthy and claims run below projections, you keep the difference rather than subsidizing the insurer’s bottom line.

-

ERISA preemption of state mandates. Self-funded plans follow federal rules and are largely exempt from state-level insurance benefit mandates. A state law requiring fully insured plans to cover fertility treatments, for example, typically does not apply to self-funded plans. The employer chooses which benefits to include, which means you can design a plan that matches your workforce’s actual needs rather than a state-mandated checklist.

-

Cash flow management. Premiums for fully insured plans are paid monthly regardless of whether employees use their benefits. Self-funded plans pay claims as they occur, which can improve cash flow during periods of low utilization.

-

Claims data transparency. Employers receive detailed data on how their plan dollars are being spent. This visibility allows you to identify cost drivers, adjust plan design, and negotiate more effectively with providers or TPAs.

-

Employer control over plan decisions. Employer plan documents govern benefits in a self-funded arrangement, not the insurer’s standard policy language. This means you can add or remove benefits, adjust cost-sharing, and tailor the plan in ways a fully insured product rarely allows.

The self funded health benefits available through this model are genuinely broader than most small business owners realize. The key is pairing that flexibility with sound financial planning.

How does a self-funded plan differ from a fully insured plan?

The core difference between self-funded vs fully insured plans comes down to one question: who pays the claims and bears the financial risk?

| Feature | Self-funded plan | Fully insured plan |

|---|---|---|

| Who pays claims | Employer pays directly | Insurance carrier pays |

| Financial risk | Employer bears the risk | Insurer bears the risk |

| Regulatory framework | Federal ERISA rules | State insurance mandates apply |

| Plan design flexibility | High. Employer controls benefits | Limited by state mandates and carrier offerings |

| Employee experience | Similar. Same ID cards and networks | Similar. Standard carrier experience |

| Premium structure | Variable. Pay claims as incurred | Fixed monthly premiums |

From an employee’s perspective, the experience looks nearly identical whether the plan is self-funded or fully insured. The same insurance logo appears on the ID card, the same provider network applies, and claims are processed through the same administrative channels. The financial and legal structure underneath is entirely different, but employees rarely notice it.

The regulatory gap is significant for small business owners. Fully insured plans must comply with every state mandate in the state where the policy is issued. Self-funded plans operate under federal ERISA rules, which preempt most state mandates. This gives self-funded employers more latitude in plan design, but it also means fewer consumer protections built into state law apply automatically.

Pro Tip: To verify whether your current plan is self-funded or fully insured, read your Summary Plan Description (SPD). The SPD is the legal document that identifies who bears financial responsibility for claims. HR departments and plan administrators are required to provide it upon request.

What are the risks and challenges of a self-funded plan?

Self-funded plans carry real financial exposure that every employer must understand before committing. The advantages of self funding do not come without trade-offs.

- Catastrophic claim risk. A single employee with a serious illness or injury can generate claims that far exceed what you budgeted. Without protection, one bad year can destabilize a small business’s finances entirely.

- Stop-loss insurance is not optional. Stop-loss coverage protects employers from high-cost claims by reimbursing costs above a set threshold. Specific stop-loss covers individual high-cost claimants. Aggregate stop-loss covers total plan costs that exceed a defined ceiling. Both types are standard practice for self-funded employers of any size.

- Cash flow requirements. Self-funded plans require sufficient liquid reserves to pay claims as they come in. A business with thin operating margins may struggle to absorb a high-claims month without disrupting other operations.

- Administrative complexity. Managing a self-funded plan involves compliance with ERISA, annual Form 5500 reporting, Summary Plan Description maintenance, and ongoing TPA oversight. This burden is manageable with the right partners, but it is not trivial.

- Unpredictable annual costs. Unlike a fully insured plan with a fixed monthly premium, self-funded plan costs fluctuate with actual claims. Budgeting requires more sophisticated modeling and a tolerance for variability.

Employers considering self-funded plans should carefully analyze financial stability and anticipated claims before making the switch. The risks are manageable, but they require deliberate planning.

Is a self-funded plan right for self-employed individuals and small businesses?

Evaluating whether a self-funded plan fits your situation requires honest answers to a few specific questions.

-

Assess your cash flow and reserves. Self-funding works best when you have enough liquid assets to absorb a high-claims month without stress. A general rule of thumb is to have at least three to six months of projected claims costs accessible before launching a self-funded plan.

-

Analyze your workforce’s health profile. A younger, healthier workforce with low historical claims is a better candidate for self-funding than a group with chronic conditions or high utilization. Request claims history data from your current carrier before making any decision.

-

Consider level-funded plans as a starting point. Level-funded plans charge a fixed monthly amount that covers expected claims, stop-loss insurance, and administration. At year end, if actual claims were lower than projected, you receive a refund. This structure gives smaller employers the financial predictability of a fully insured plan with some of the upside of self-funding.

-

Engage a broker or consultant with self-funding experience. The plan document, TPA selection, stop-loss carrier, and network access all require expert coordination. A broker who specializes in private health insurance for business owners can model your specific situation and identify whether self-funding or a hybrid approach makes financial sense.

-

Read the plan documents before signing anything. The Summary Plan Description is the governing legal document for your plan. It defines what is covered, who pays, and how disputes are resolved. Never rely on a carrier’s marketing materials to understand what you are actually buying.

Pro Tip: If you are self-employed with no employees, a traditional self-funded plan is not available to you as an individual. However, level-funded small group plans and association health plans may offer similar cost advantages. A specialized broker can identify which options apply to your specific situation.

Key takeaways

Self-funded health plans give employers direct control over healthcare spending, but that control comes with financial risk that requires careful preparation and the right administrative partners.

| Point | Details |

|---|---|

| Core definition | Employer pays medical claims directly instead of paying fixed premiums to an insurer. |

| Stop-loss insurance is required | Specific and aggregate stop-loss coverage protects against catastrophic individual and total plan costs. |

| ERISA governs self-funded plans | Federal rules apply instead of state mandates, giving employers more benefit design flexibility. |

| Level-funded plans bridge the gap | Smaller employers can access self-funding economics with more predictable monthly costs through level-funded structures. |

| Plan documents control everything | The Summary Plan Description, not the insurer’s branding, defines what your plan actually covers and who pays. |

What I have learned advising small business owners on self-funded plans

Most small business owners I speak with assume self-funded plans are only for large corporations. That assumption costs them money every year. The real barrier is not company size. It is the absence of a financial model that accounts for stop-loss coverage, reserve requirements, and TPA costs alongside projected claims savings.

The clients who succeed with self-funded or level-funded arrangements share one trait: they did the math before they committed. They pulled two to three years of claims history, modeled best-case and worst-case scenarios, and priced stop-loss coverage before making any decision. The ones who struggled either underestimated cash flow requirements or chose a TPA based on price alone without evaluating their claims data reporting capabilities.

My honest recommendation is this: if you are a small business owner with five or more employees and your fully insured premiums have increased more than 10 percent in the past two years, a self-funded or level-funded plan deserves a serious look. Not because it is automatically better, but because you owe it to your business to understand what you are paying for and whether a different structure would serve you better.

Stop-loss insurance is non-negotiable. I have seen employers skip it to reduce costs and then face a six-figure claim that wiped out a year of savings. The premium for stop-loss coverage is the price of sleeping at night. Pay it.

— mkaravas1m

How Sageshieldassurance helps you find the right health plan

Sageshieldassurance works with self-employed individuals and small business owners across 40 states to evaluate exactly these decisions. Whether you are weighing a self-funded insurance plan against a fully insured option, or exploring level-funded structures for the first time, the team at Sageshieldassurance models your specific situation before recommending anything.

Their health insurance planning services include claims history analysis, TPA vetting, stop-loss carrier comparisons, and ongoing plan management support. If you want a clear picture of what self-funding would actually cost your business, a personalized consultation is the fastest way to get there. Sageshieldassurance has served over 500 families with exactly this kind of hands-on guidance, and they bring that same specificity to every business owner they work with.

FAQ

What is a self-funded health plan in simple terms?

A self-funded health plan is an arrangement where the employer pays employee medical claims directly instead of paying premiums to an insurance company. An insurance carrier or third-party administrator typically handles the administrative work, but the employer bears the financial risk.

How do self-funded plans work for small businesses?

Small businesses can access self-funded plans by contracting with a third-party administrator for claims processing and purchasing stop-loss insurance to cap their financial exposure. Level-funded plans offer a more accessible entry point by combining self-funding mechanics with fixed monthly payments.

What is the difference between self-funded and fully insured plans?

In a fully insured plan, the insurance carrier pays claims and bears financial risk in exchange for fixed monthly premiums. In a self-funded plan, the employer pays claims directly and retains the financial risk, but gains more flexibility in plan design and access to detailed claims data.

Do self-funded plans have to follow state insurance laws?

Self-funded plans are governed primarily by federal ERISA rules and are largely exempt from state insurance benefit mandates that apply to fully insured plans. This gives employers more control over benefit design but also means certain state consumer protections do not apply automatically.

Is stop-loss insurance required for self-funded plans?

Stop-loss insurance is not legally required, but it is considered standard practice for any self-funded employer. It protects against catastrophic individual claims and total plan costs that exceed projected levels, making it a practical necessity rather than an optional add-on.

Leave a Reply