What Is a Life Insurance Policy? Your 2026 Guide

A life insurance policy is a legal contract between you and an insurer where you pay regular premiums, and the insurer pays a death benefit to your named beneficiaries after you die. That single transaction, repeated over years, is what stands between your family’s financial stability and a crisis. The policy’s three core components are the death benefit (the payout amount), the premium (your cost to maintain coverage), and the beneficiary (the person or entity who receives the money). Understanding how these pieces connect is the first step toward choosing coverage that actually fits your life.

What is a life insurance policy and how does it work?

Life insurance explained at its most basic level: you apply for a policy, get approved through underwriting, pay your premiums, and your beneficiaries collect the death benefit when you die. The underwriting process typically takes 1 to 8 weeks depending on the insurer and the method used, which can range from a full medical exam to an accelerated digital review. That timeline matters because coverage does not begin until the policy is issued and the first premium is paid.

Once the policy is active, your only job is to keep it in force by paying premiums on schedule. If you stop paying, most policies enter a grace period of 30 to 31 days before lapsing. A lapsed policy means no coverage, which is the single most preventable reason families are left without a payout.

When a death occurs, the beneficiary files a claim with the insurer. Insurers require a death certificate, the policy number, and proof of the beneficiary’s identity before releasing funds. Incomplete documentation is the most common cause of payout delays, so storing these documents in an accessible place is a practical step every policyholder should take.

The payout itself is generally a lump sum, and death benefits are typically income tax-free for beneficiaries. One exception applies when the insurer holds the funds and pays interest over time. That interest portion is taxable, even though the base benefit is not.

Pro Tip: Keep a digital copy of your policy documents, beneficiary designations, and insurer contact information in a shared folder that your beneficiaries can access immediately. Delays in claims often come from families not knowing where to look.

What are the main types of life insurance?

Two main categories define the market: term life insurance and permanent life insurance. Each serves a different financial purpose, and choosing between them depends on how long you need coverage and what you want the policy to do beyond paying a death benefit.

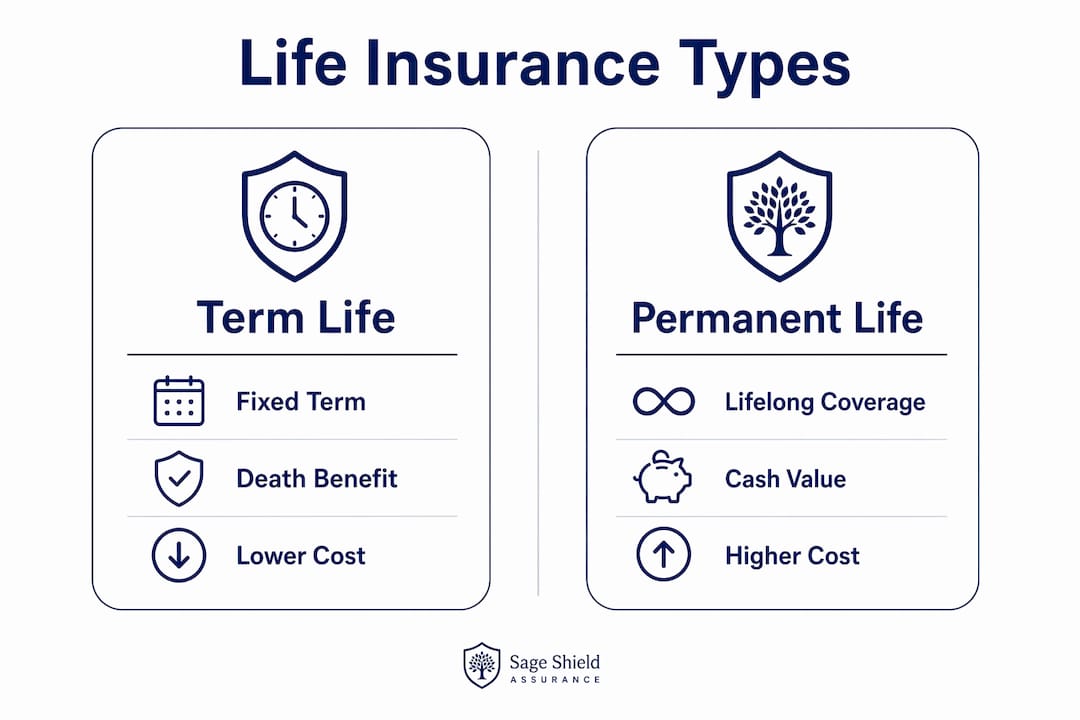

Term life insurance

Term life is considered pure life insurance because it focuses entirely on the death benefit with no savings component attached. You buy coverage for a fixed period, typically 10, 20, or 30 years, pay a flat premium throughout that term, and the policy expires if you outlive it. It is the least expensive way to get a large death benefit, which makes it the right fit for covering temporary financial obligations like a mortgage or raising children through college.

Permanent life insurance

Permanent life insurance provides lifelong coverage and builds cash value over time. The three main subtypes are whole life, universal life, and variable life. Whole life carries fixed premiums and a guaranteed cash value growth rate. Universal life offers flexible premiums and adjustable death benefits. Variable life ties cash value growth to investment sub-accounts, which adds market risk but also growth potential. You can read a detailed breakdown of whole life mechanics in Sageshieldassurance’s whole life insurance guide.

Cash value in permanent policies can be accessed through loans or withdrawals, but borrowing against it without careful management can trigger tax consequences or even cause the policy to lapse. This is one of the most misunderstood features in permanent coverage.

| Feature | Term life | Permanent life |

|---|---|---|

| Coverage duration | Fixed period (10 to 30 years) | Lifelong |

| Premium cost | Lower | Higher |

| Cash value | None | Builds over time |

| Complexity | Simple | More complex |

| Best for | Temporary obligations | Long-term planning |

Pro Tip: If your primary goal is income replacement for dependents during your working years, term life almost always delivers the most coverage per dollar. Consider permanent life only when you have a long-term estate planning or business continuity need.

What are the key benefits of life insurance?

The most direct benefit of life insurance is income replacement. If you earn $75,000 a year and your family depends on that income, a $750,000 death benefit gives your survivors roughly a decade to rebuild financial stability. That math is straightforward, but the real value goes further.

Life insurance payouts cover obligations that do not disappear when you do. Families commonly use death benefits for:

- Paying off a mortgage so dependents keep their home

- Clearing outstanding debts like car loans or credit card balances

- Funding a child’s college education

- Covering final expenses including funeral and burial costs, which average several thousand dollars

- Replacing a business partner’s equity in a buy-sell agreement

Some policies include living benefits riders that allow early access to a portion of the death benefit if you are diagnosed with a critical illness like cancer or a major cardiac event. This feature converts a death-only payout into a financial tool you can use while still alive, which changes the value calculation significantly.

The tax treatment of life insurance adds another layer of protection. Death benefits are generally not taxable income for beneficiaries, though tax can arise on interest earned in certain estate-related situations. For high-net-worth individuals, policy ownership structure matters and is worth reviewing with a financial advisor.

How to choose and manage a life insurance policy

Coverage amounts should align with real financial obligations, not round numbers chosen arbitrarily. A common starting framework is to multiply your annual income by 10 and then add outstanding debts and future education costs. That calculation gives you a floor, not a ceiling.

Several factors directly influence what you will pay in premiums:

- Age: Premiums rise with age because mortality risk increases. Buying at 30 costs significantly less than buying at 45.

- Health: Insurers review medical history, current conditions, and prescription records. Smokers typically pay two to three times more than non-smokers.

- Lifestyle: High-risk hobbies like skydiving or scuba diving can raise premiums or trigger exclusions.

- Coverage amount and type: A $1 million 20-year term policy costs more than a $500,000 10-year term policy, but both cost less than comparable permanent coverage.

Beyond the initial purchase, managing your policy over time matters just as much as choosing it. Beneficiary designations should be reviewed after every major life event: marriage, divorce, the birth of a child, or the death of a named beneficiary. A policy with an outdated beneficiary designation can send the death benefit to the wrong person, and courts rarely override that outcome.

Riders deserve the same attention. Accelerated death benefit riders, waiver of premium riders, and child term riders each add value in specific circumstances. Reviewing them annually takes less than an hour and can prevent gaps in protection.

If you are self-employed or run a small business, the coverage calculation gets more complex. Sageshieldassurance’s self-employed life insurance guide walks through the specific obligations business owners need to account for, including key-person coverage and buy-sell funding.

Common pitfalls to avoid:

- Letting a policy lapse during a grace period because of a missed payment

- Assuming cash value equals the death benefit (it does not)

- Underinsuring because the premium feels high today

- Failing to disclose health conditions on the application, which can void a claim

Key takeaways

A life insurance policy is the most direct financial tool for protecting your family’s income and obligations after your death, and the type you choose determines both cost and long-term value.

| Point | Details |

|---|---|

| Core definition | A policy pays a death benefit to named beneficiaries in exchange for regular premium payments. |

| Two main types | Term life covers a fixed period at lower cost; permanent life provides lifelong coverage with cash value. |

| Tax advantage | Death benefits are generally income tax-free for beneficiaries, with limited exceptions for interest. |

| Coverage sizing | Base your coverage amount on actual financial obligations, not arbitrary round numbers. |

| Policy management | Review beneficiary designations and riders after every major life event to keep coverage accurate. |

Why most people get life insurance wrong the first time

Most people approach life insurance the same way they approach buying a car: they look at the monthly payment and pick the option that fits the budget. That logic works for a car. It fails for life insurance, and the consequences show up years later when it is too late to fix them.

The mistake I see most often is underinsuring. Someone buys a $250,000 term policy because the premium is affordable, without ever calculating whether $250,000 actually covers their mortgage, replaces their income for a meaningful period, and funds their children’s education. It does not. It just feels like a large number.

The second mistake is treating permanent life insurance as a savings account. Cash value growth in whole or universal life is real, but it is slow and comes with costs that most policyholders do not fully understand until they try to access it. Borrowing against cash value without understanding the loan terms can trigger a tax event or collapse the policy entirely. That is not a theoretical risk. It happens regularly.

What actually works is starting with a clear number: what would your family need to maintain their standard of living for 10 years if your income disappeared tomorrow? Build the coverage around that figure, then choose the policy type that fits your timeline and budget. If you are 35 with a mortgage and two kids, a 20-year term policy almost certainly gives you the most protection per dollar. If you are a business owner with estate planning needs, permanent coverage deserves a serious look.

The other thing I would tell anyone exploring coverage for the first time: do not wait. Every year you delay, premiums go up and health conditions that affect underwriting become more likely. The best policy is the one you buy today, not the perfect one you research for three more years.

— mkaravas1m

How Sageshieldassurance can help you find the right coverage

Sageshieldassurance works with self-employed individuals and business owners across 40 states to match them with life insurance coverage that fits their actual financial picture, not a generic plan off a shelf.

With access to multiple leading insurance providers, Sageshieldassurance compares policy options across term and permanent products to find coverage that fits your budget and obligations. Their team handles the underwriting process, explains policy details in plain language, and reviews your coverage as your life changes. If you are also weighing health insurance options alongside life coverage, Sageshieldassurance can address both in a single conversation. For business owners specifically, their business life insurance guide covers the additional coverage layers that protect both your family and your company.

FAQ

What is a life insurance policy in simple terms?

A life insurance policy is a contract where you pay regular premiums to an insurer, and the insurer pays a lump sum death benefit to your named beneficiaries after you die. The benefit is designed to replace your income and cover financial obligations your family would otherwise face alone.

How do life insurance premiums work?

Premiums are the regular payments you make to keep your policy active, typically monthly or annually. The amount is set at the time of purchase based on your age, health, lifestyle, and the coverage amount you choose, and a lapsed premium can end your coverage after a short grace period.

What is the difference between term and permanent life insurance?

Term life covers you for a fixed period, such as 10 to 30 years, with no cash value component. Permanent life provides lifelong coverage and builds cash value over time, but carries higher premiums and greater complexity.

Are life insurance death benefits taxable?

Death benefits paid to beneficiaries are generally income tax-free. Tax can apply to interest earned if the insurer holds the funds over time, or in certain estate-related ownership situations.

How much life insurance coverage do I actually need?

Coverage should reflect your real financial obligations: outstanding mortgage, debts, income replacement for dependents, and future education costs. A common starting point is 10 times your annual income, adjusted upward for specific obligations.

Leave a Reply