Mental Health Coverage Private Plan: 2026 Guide

Mental health coverage in a private health insurance plan is defined as the set of benefits that pay for psychological, psychiatric, and substance use disorder services under your policy. As of 2026, ACA marketplace plans cover mental health as an essential benefit with no annual or lifetime dollar limits, and most private plans from major insurers like Blue Cross Blue Shield, Aetna, and Cigna follow the same standard. What separates a plan that truly serves your mental health needs from one that looks good on paper is the structure: plan type, network size, cost-sharing rules, and how the insurer handles prior authorization. This guide breaks all of it down so you can choose with confidence.

What mental health services do private health insurance plans usually cover?

Private health insurance mental health benefits typically include a broad range of services, but the specifics depend on your plan tier and insurer. Knowing what is and is not covered before you enroll prevents costly surprises later.

Most private plans cover the following categories of mental health treatment:

- Individual therapy: One-on-one sessions with a licensed therapist, psychologist, or licensed clinical social worker. Coverage applies to evidence-based approaches like cognitive behavioral therapy (CBT) and dialectical behavior therapy (DBT).

- Group and family therapy: Sessions involving multiple participants or family members, often at a lower copay than individual sessions.

- Psychiatric services: Evaluations, medication management, and follow-up appointments with a psychiatrist.

- Substance use disorder treatment: Inpatient detox, outpatient rehabilitation, and medication-assisted treatment programs. For more on how medication-assisted treatment works, the misconceptions around MAT are worth reviewing before you assume what your plan will or will not pay for.

- Telehealth therapy: Telehealth coverage is now standard and often reimbursed at in-person rates, though licensing and state rules vary.

- Inpatient psychiatric care: Hospitalization for acute mental health crises, subject to medical necessity review.

One critical requirement applies across all of these: therapy coverage requires a documented mental health diagnosis from a licensed provider. Sessions billed without a proper diagnosis and appropriate billing codes may be denied entirely. This is not a technicality. It is the mechanism insurers use to define “medically necessary” care, which is the threshold most plans require before paying a single dollar.

How do different private insurance plan types affect mental health coverage?

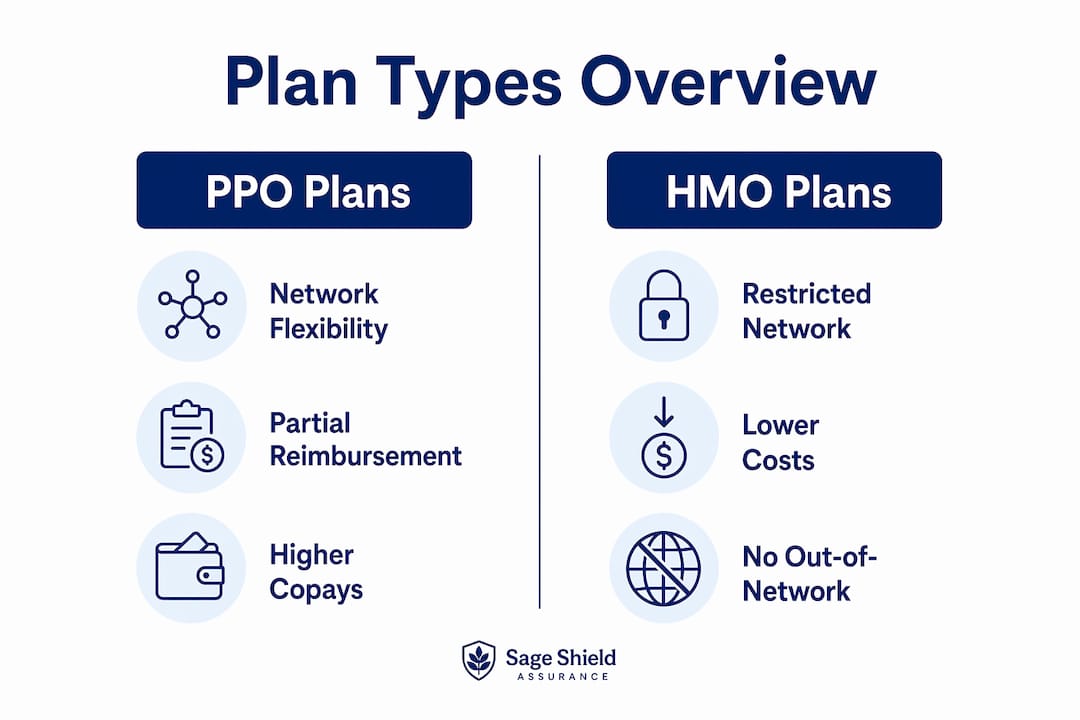

The plan type you choose shapes not just your costs but your access to providers. Three structures dominate the private market: PPO, HMO, and HDHP. Each creates a different experience when you seek mental health care.

| Plan Type | Network Flexibility | Typical Copay | Out-of-Network Coverage |

|---|---|---|---|

| PPO | High — see any provider | $30–$60 per session | Yes, with partial reimbursement |

| HMO | Low — in-network only | $15–$40 per session | No, except emergencies |

| HDHP | Moderate | Varies after deductible | Sometimes, with higher cost share |

PPO plans allow out-of-network care with partial reimbursement, while HMOs restrict coverage to a network with typically lower copays. For mental health specifically, this distinction matters more than it does for primary care. The therapist you connect with may not be in every network, and switching providers mid-treatment carries real psychological and clinical costs.

High-deductible health plans (HDHPs) pair with Health Savings Accounts (HSAs), which let you pay for therapy with pre-tax dollars. That tax advantage can offset the higher upfront deductible, but you will pay full session costs until you meet it. For someone in weekly therapy, that deductible can be exhausted quickly.

Employee Assistance Programs (EAPs) sit outside this structure entirely. EAPs offer 6 to 12 free short-term therapy sessions annually, separate from insurance deductibles. Many people enrolled in HDHPs or plans with high deductibles overlook EAPs entirely, which is a significant financial mistake. EAP sessions do not count against your deductible and do not require a formal diagnosis to access.

Pro Tip: If you are self-employed and evaluating plan tiers, the 2026 self-employed plan tier guide from Sageshieldassurance breaks down how Bronze, Silver, Gold, and Platinum tiers affect your mental health cost-sharing in practical terms.

What costs should you expect with mental health coverage on private plans?

Cost is where most people get caught off guard. The sticker price of a therapy session and what you actually pay after insurance are often very different numbers.

Here is what the typical cost structure looks like for in-network mental health care on a private plan:

- Copays: Most in-network therapy sessions carry a copay of $20 to $50 per visit. This applies after you meet your deductible on plans that require it.

- Deductibles: Many plans require you to meet a deductible before copays kick in. On an HDHP, that deductible can exceed $1,500 for an individual.

- Coinsurance: Some plans charge a percentage of the session cost rather than a flat copay. A 20% coinsurance on a $150 session means you pay $30, but that rate applies only after the deductible.

- Out-of-network therapy: PPO out-of-network reimbursement ranges from 50% to 80% after meeting your deductible. The remaining balance, called the balance bill, comes directly from your pocket.

The Mental Health Parity and Addiction Equity Act (MHPAEA) legally requires private insurers to apply the same financial limits to mental health benefits as they do to medical and surgical benefits. However, reimbursement for outpatient mental health care runs 16% to 59% lower than for physical health care across all 50 states. That gap exists because parity law governs cost-sharing rules, not what insurers pay clinicians. Lower clinician reimbursement rates push more therapists out of network, which shifts costs back to you.

For those on Medicare, Medicare Part B covers outpatient mental health therapy after a $283 deductible, with 20% coinsurance per session in 2026. That is a relatively predictable cost structure compared to many private plans.

How to verify coverage and avoid surprises with mental health benefits

Verifying your benefits before your first session is the single most effective way to protect yourself from unexpected bills. Here is a step-by-step process that works.

- Call your insurer’s member services line. Ask specifically about outpatient mental health benefits, your deductible status, copay or coinsurance amounts, and whether prior authorization is required for ongoing therapy.

- Verify provider network status through the insurer’s portal. Always verify therapist network status through your insurer’s member portal rather than relying on therapist directories. Directories are often outdated by months or years.

- Ask about prior authorization. Some plans require pre-approval for more than a set number of sessions per year. Skipping this step can result in a full denial of claims.

- Confirm documentation requirements with your therapist. Ask whether they will document a formal diagnosis and use the correct billing codes. Therapy coverage requires documented diagnosis and appropriate billing codes. Sessions treated as elective without such documentation may not be covered.

- Use your EAP first. If your employer or association offers an EAP, exhaust those free sessions before activating your primary insurance. This preserves your deductible and out-of-pocket maximum for higher-cost care later in the year.

Pro Tip: When you call member services, ask for the information in writing via a member portal message or email confirmation. Verbal benefit quotes are not binding, but written records give you a paper trail if a claim is later denied.

For a broader look at how private insurance benefits work for self-employed individuals and business owners, Sageshieldassurance has published a detailed breakdown worth reading before you enroll.

How to choose the best private mental health insurance plan for your needs

Selecting the right plan comes down to matching your actual therapy needs to the plan’s structure. Generic plan rankings rarely account for mental health access specifically.

Consider these factors in order of priority:

- Network size and local provider availability. A plan with 10,000 in-network therapists nationally means little if only three are within 20 miles of you and none are accepting new patients. Check the insurer’s provider directory filtered by your zip code before you commit.

- Therapy frequency. If you attend weekly sessions, a PPO’s higher premium may cost less annually than an HMO’s restricted network that forces you out-of-network. Run the math on your actual usage.

- Out-of-pocket maximum. This is the ceiling on your annual exposure. A plan with a $3,000 out-of-pocket maximum protects you far better than one with a $7,500 cap if you need intensive mental health treatment.

- Telehealth and integrated behavioral health. Plans from insurers like Cigna and Aetna now include integrated behavioral health programs that connect physical and mental health care. These programs often include digital therapy tools and care coordinators at no additional cost.

- EAP availability. If you are self-employed and buying an individual plan, EAP access is not automatic. Some insurers bundle EAP-style benefits into their plans. Ask explicitly.

For self-employed individuals managing pre-existing mental health conditions, plan selection carries additional weight. ACA-compliant plans cannot deny coverage or charge higher premiums based on mental health history, but the depth of benefits still varies significantly by plan.

Understanding what mental health care actually encompasses, from therapy modalities to psychiatric services, helps you evaluate whether a plan’s network truly meets your clinical needs.

Key takeaways

Choosing the right mental health coverage private plan requires matching your therapy frequency, provider preferences, and budget to a plan’s network, cost structure, and authorization rules before you enroll.

| Point | Details |

|---|---|

| ACA plans cover mental health | All ACA-compliant private plans include mental health as an essential benefit with no dollar limits. |

| Plan type determines access | PPOs offer out-of-network flexibility; HMOs lower costs but restrict provider choice significantly. |

| Diagnosis documentation is required | Coverage applies only when a licensed provider documents a formal mental health diagnosis with correct billing codes. |

| EAPs are underused | EAPs provide 6 to 12 free therapy sessions annually, separate from your deductible. |

| Verify before your first session | Always confirm network status, prior authorization rules, and copay amounts through your insurer’s portal. |

What I’ve learned about mental health coverage after reviewing hundreds of plans

Parity laws are real, and they matter. But they do not guarantee equal access. The reimbursement gap between mental and physical health care is the quiet driver behind why so many therapists decline insurance altogether. When a plan’s network looks thin for mental health providers, that is usually why.

The clients I see make the most costly mistakes are those who pick a plan based on premium alone and discover mid-year that their therapist is out-of-network. PPO plans cost more monthly, but for someone in regular therapy, that premium difference is often recovered in avoided out-of-network bills within two or three sessions.

EAPs are genuinely underused. I have reviewed plans for self-employed individuals who had no idea their association membership included EAP access. Six free sessions per year is not a complete solution, but it is a meaningful buffer while you navigate your primary insurance.

Telehealth has changed the access equation, but it is not frictionless. State licensing rules mean your therapist may not be able to see you across state lines, even if your plan covers telehealth. If you travel frequently or split time between states, verify this before you assume your coverage travels with you.

The bottom line: read the mental health benefits section of your Summary of Benefits and Coverage document before you sign. It is two pages. Those two pages will tell you more than any plan comparison chart.

— mkaravas1m

How Sageshieldassurance helps you find the right plan

Finding a private plan with strong mental health benefits is not a one-size-fits-all process. Sageshieldassurance works with self-employed individuals and business owners across 40 states to match them with plans from leading insurers that include the mental health benefits they actually need. Their brokers review your therapy frequency, provider preferences, and budget to identify plans where the network, cost structure, and telehealth options align with your real-world usage. Visit Sageshieldassurance health insurance to explore private plan options with mental health coverage built in, or connect with a broker directly to get a personalized plan review at no cost.

FAQ

What mental health services does a private plan typically cover?

Private health insurance mental health benefits generally include individual therapy, group therapy, psychiatric evaluations, medication management, substance use disorder treatment, and telehealth sessions. Coverage applies when a licensed provider documents a formal diagnosis and uses the correct billing codes.

Does the Mental Health Parity Act guarantee equal coverage?

The MHPAEA requires private insurers to apply the same financial limits to mental health benefits as to medical benefits, but reimbursement rates for outpatient mental health care remain 16% to 59% lower than for physical health care nationwide. Parity law governs cost-sharing rules, not clinician pay rates.

Is telehealth therapy covered under private insurance plans?

Telehealth therapy is now standard coverage on most private plans and is often reimbursed at the same rate as in-person sessions. State licensing rules vary, so confirm your therapist is licensed in your state before scheduling a virtual appointment.

What is the difference between PPO and HMO for mental health coverage?

PPO plans allow you to see out-of-network therapists with partial reimbursement of 50% to 80% after your deductible. HMO plans restrict coverage to in-network providers but typically offer lower copays, making them more cost-efficient if your preferred therapist is in the network.

How do I use my EAP before my primary insurance?

Contact your employer’s HR department or your insurer to get your EAP provider’s contact information. EAPs offer 6 to 12 free therapy sessions per year that do not count against your deductible. Use these sessions first to preserve your out-of-pocket maximum for higher-cost care later in the year.

Leave a Reply