Individual Health Coverage for Self-Employed Owners in 2026

Individual health coverage is health insurance you purchase directly, independent of any employer or government program, giving you full control over your plan, your network, and your costs. For self-employed individuals and small business owners, this is not a fallback option. It is the primary path to protecting your health and your finances. Approximately 9% of Americans carry individually purchased health insurance, a figure that understates how central this market has become for the growing independent workforce. Understanding how personal health coverage works, what it costs, and which plan types actually protect you is the difference between smart coverage and an expensive mistake.

What is individual health coverage and how does it work?

Individual health coverage, also called individual health insurance or personal health coverage, is a policy you buy for yourself or your family outside of a job-based benefits package. You choose the plan, you pay the premium, and you own the policy regardless of where you work or whether your business structure changes. That portability is the defining advantage for anyone running their own business.

You can purchase an individual health plan through three main channels. The first is the ACA Marketplace, operated at HealthCare.gov or through state-run exchanges, where income-based premium tax credits may reduce your monthly cost. The second is directly through an insurer, which bypasses the exchange but also forfeits subsidy eligibility. The third is through a licensed broker, like Sageshieldassurance, who can compare plans across carriers and explain trade-offs you would likely miss on your own.

Plan types in the individual market vary significantly in what they cover and what they cost:

- ACA-compliant plans cover the ten essential health benefits, including mental health services, preventive care, and prescription drugs, and cannot deny you coverage for pre-existing conditions.

- Short-term health plans offer lower premiums but can exclude pre-existing conditions, cap benefits, and leave you exposed to large bills.

- Fixed indemnity plans pay a set dollar amount per medical event, not actual costs, which can create serious coverage gaps.

- Healthcare sharing ministries are cost-sharing groups, not insurance. Sharing ministries carry no legal obligation to pay your medical bills, which makes them a financial gamble for anyone with significant health needs.

Pro Tip: If you qualify for a premium tax credit on the ACA Marketplace, you almost certainly get more value from an on-exchange ACA plan than from any off-exchange alternative, even if the off-exchange premium looks lower at first glance.

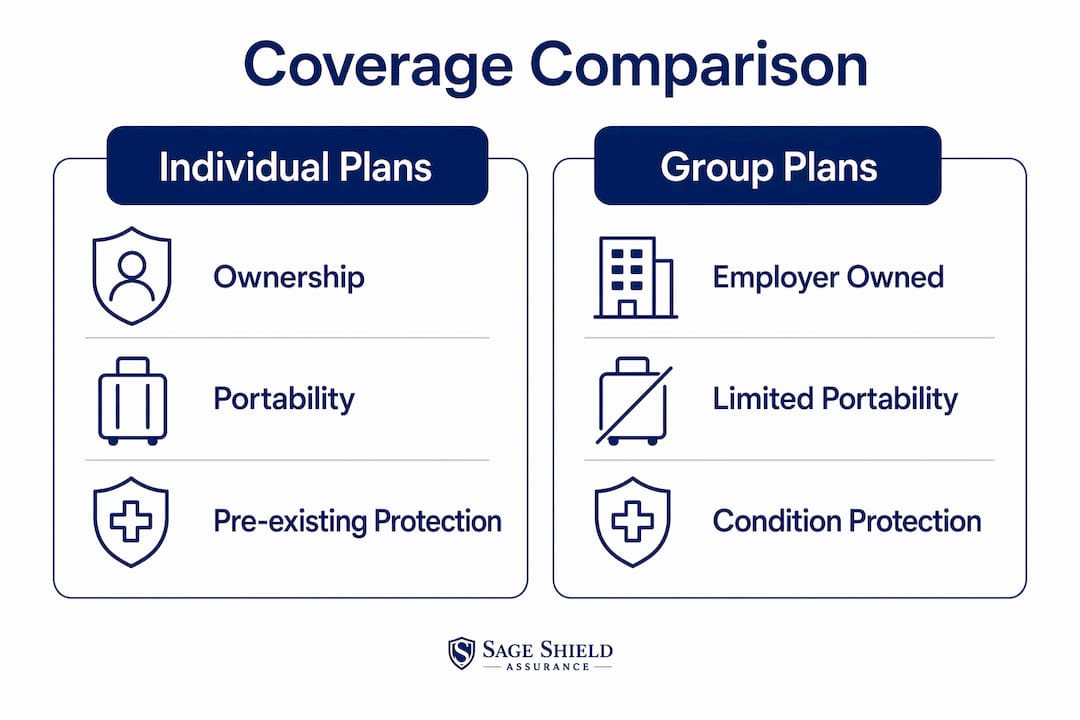

How does individual coverage compare to employer-sponsored group insurance?

The core difference between individual and group insurance is ownership. With group insurance, your employer selects the plan and pays a portion of the premium. With an individual health plan, you make every decision and absorb the full cost, though tax credits and deductions can offset that significantly for self-employed filers.

Here is how the two models compare across the factors that matter most to small business owners:

| Feature | Individual health coverage | Employer group insurance |

|---|---|---|

| Plan ownership | You own and control the policy | Employer controls plan selection |

| Portability | Stays with you regardless of job status | Ends when employment ends |

| Pre-existing conditions | Protected under ACA-compliant plans | Protected under group plans |

| Premium tax credits | Available on ACA Marketplace | Not available |

| Premium cost | Full cost on you, offset by credits or deductions | Employer typically pays 50% or more |

| Plan customization | High, you choose tier and network | Limited to employer’s chosen options |

The portability column is where individual coverage wins decisively for anyone self-employed. When you run your own business, there is no employer to lose. Your plan continues uninterrupted whether your revenue doubles or your business model shifts entirely. That continuity has real financial value that rarely appears in premium comparisons.

Pre-existing condition protections also apply to ACA-compliant individual plans, meaning insurers cannot charge you more or deny coverage based on your health history. That protection does not extend to short-term or non-ACA plans, which is a critical distinction when evaluating affordable individual health insurance options.

How do ICHRAs work for small business owners?

An Individual Coverage Health Reimbursement Arrangement, or ICHRA, is a formal mechanism that allows employers to reimburse employees tax-free for individual health insurance premiums and qualifying medical expenses. ICHRAs reduce administrative burden while giving employees the freedom to choose their own plans, making them a practical alternative to traditional group coverage for small businesses.

The mechanics are straightforward. You set a monthly reimbursement amount. Employees purchase their own individual plans, submit proof of premium payments, and receive reimbursements tax-free. You deduct the reimbursements as a business expense. Employees get personalized coverage rather than a one-size plan chosen by HR.

Key considerations for small business owners evaluating ICHRAs:

- State rules vary. State-level ICHRA regulations affect employer tax advantages and employee eligibility for premium tax credits. An employee receiving an ICHRA reimbursement above a certain affordability threshold cannot also claim a Marketplace tax credit.

- No minimum contribution is required. You set the reimbursement cap, which gives you direct control over your benefits budget.

- Employees with pre-existing conditions benefit. Because they are purchasing ACA-compliant individual plans, they retain full protections regardless of health history.

- Setup compliance matters. Improper ICHRA setup can disqualify employees from premium tax credits and affect your tax deductibility, so working with a knowledgeable broker is not optional.

Pro Tip: ICHRAs work especially well when your team is spread across multiple states, since each employee can choose a plan with the local network that fits their location rather than being locked into a single group plan.

The individual health insurance market and the ICHRA model are increasingly intertwined. Off-exchange individual plans are often the preferred vehicle for ICHRA reimbursements because they can offer competitive premiums without the exchange’s income verification requirements.

What are the biggest challenges in the 2026 individual market?

The 2026 individual market is under significant pressure from two directions: rising costs and shrinking insurer participation. Both forces directly affect self-employed buyers and small business owners who rely on this market for coverage.

On the cost side, the expiration of enhanced premium tax credits that were introduced during the pandemic has hit Marketplace enrollees hard. 51% of returning Marketplace enrollees reported significantly higher healthcare costs in 2026, with 55% planning to cut other household spending to afford coverage. That is not a marginal adjustment. It is a structural affordability crisis for millions of individual market buyers.

On the supply side, several insurers exited the ACA Marketplace in 2026, affecting over 600,000 enrollees who had to find new plans. Insurer participation is driven by enrollment numbers, risk pool stability, and policy predictability. When those factors deteriorate, carriers exit, and consumers in affected counties face fewer choices and higher premiums.

“This is gambling.” That phrase, used by a consumer advocate describing the shift toward no-frills health plans, captures the real risk of choosing coverage based on premium alone.

The response from many consumers has been predictable but dangerous. Off-exchange plans now account for more than 40% of individual market offerings in 2026, often lacking federal consumer protections. Many buyers do not realize that off-exchange plans can lack essential health benefits and consumer protections, leading to denied claims or benefit caps when they need coverage most. The lower premium is real. The coverage gap is also real.

| Market factor | 2026 status | Impact on buyers |

|---|---|---|

| Enhanced tax credits | Expired post-2025 | Higher net premiums for most enrollees |

| Insurer exits | Multiple carriers withdrew | Fewer plan choices in affected counties |

| Off-exchange plan share | Over 40% of individual market | More options but weaker consumer protections |

| Marketplace enrollment | Declining due to cost increases | Smaller risk pools, potential for further premium increases |

How to choose and maintain the best individual health plan

Choosing the right individual health plan requires matching your actual health needs and budget to the plan’s real benefits, not just its monthly premium. Here is a practical process for self-employed individuals and small business owners:

- Estimate your annual healthcare use. Count your regular prescriptions, specialist visits, and any planned procedures. A Bronze plan with a low premium but a $7,000 deductible is not affordable if you use healthcare regularly.

- Check the provider network. Confirm your current doctors and preferred hospital system are in-network before selecting any plan. Out-of-network costs can eliminate any premium savings within a single visit.

- Calculate your subsidy eligibility. Use HealthCare.gov’s estimator or work with a broker to determine whether your income qualifies for a premium tax credit. Self-employed income can fluctuate, so model multiple income scenarios.

- Compare mental health coverage. ACA-compliant plans must cover mental health services at parity with physical health benefits. If you or a family member uses therapy or psychiatric care, verify that mental health treatment is covered at a realistic cost before enrolling.

- Understand open enrollment and special enrollment periods. Open enrollment for 2026 Marketplace plans runs from November 1 through January 15 in most states. A qualifying life event, such as losing other coverage, getting married, or having a child, triggers a Special Enrollment Period that gives you 60 days to enroll outside the standard window.

Pro Tip: Self-employed individuals can deduct 100% of health insurance premiums paid for themselves and their families from federal taxable income, regardless of whether they itemize. This deduction applies even if you do not purchase through the Marketplace.

Working with a trusted insurance broker removes the guesswork from plan comparison. A good broker presents options across multiple carriers, explains the real cost of each plan including deductibles and out-of-pocket maximums, and flags coverage gaps you might overlook when comparing plans on premium alone.

Key takeaways

Individual health coverage gives self-employed buyers and small business owners the portability, customization, and ACA protections that employer-sponsored plans provide by default, but only when you choose the right plan type and avoid the growing share of off-exchange alternatives that strip away those protections.

| Point | Details |

|---|---|

| Definition and ownership | Individual health coverage is purchased directly by you, not tied to any employer, and stays with you regardless of job changes. |

| ACA protections matter | Only ACA-compliant plans guarantee coverage for pre-existing conditions and all ten essential health benefits. |

| ICHRA as a business tool | Small business owners can reimburse employees tax-free for individual plans through an ICHRA, controlling costs without managing a group plan. |

| 2026 market pressure | Over half of Marketplace enrollees face higher costs after enhanced tax credits expired, pushing many toward riskier off-exchange plans. |

| Broker guidance pays off | A licensed broker helps you compare real total costs, verify networks, and avoid coverage gaps that a low premium can disguise. |

What I’ve learned about individual coverage after years in this market

The most consistent mistake I see self-employed buyers make is treating the monthly premium as the cost of health insurance. It is not. The premium is the entry fee. The actual cost is the premium plus the deductible plus the out-of-pocket maximum plus whatever your plan does not cover. I have watched people save $150 a month on premiums and then face $12,000 in uncovered bills because they chose a short-term plan that excluded a condition they did not know they had.

The 2026 market has made this mistake easier to make. With enhanced tax credits gone and premiums rising, the off-exchange plans with lower sticker prices look genuinely attractive. Some of them are reasonable products for healthy people with low healthcare use. Many of them are not. The line between a legitimate off-exchange plan and a product that will fail you when you need it most is not visible in a premium comparison table.

ICHRAs represent the most interesting structural shift I have seen in years for small business owners. The ability to give employees a defined dollar amount and let them choose their own ACA-compliant plan is genuinely better than forcing everyone onto a single group plan that fits no one perfectly. But the compliance requirements are real, and the state-level variations are not trivial. Getting the setup wrong does not just create administrative headaches. It can cost your employees their tax credits.

My honest advice: do not shop for individual health coverage alone in 2026. The market is too fragmented, the risks in off-exchange products are too real, and the tax implications of your choices are too significant to navigate without someone who does this every day.

— mkaravas1m

How Sageshieldassurance helps you find the right coverage

Sageshieldassurance specializes in individual health insurance for self-employed individuals and small business owners across 40 states. Their team compares plans across leading carriers, identifies your subsidy eligibility, and explains the real cost of each option before you commit to anything.

For small business owners evaluating ICHRAs, Sageshieldassurance provides setup guidance and ongoing management support so your arrangement stays compliant and your employees stay covered. Whether you need a single individual plan or a benefits structure for a growing team, their health insurance solutions are built around your budget and your actual health needs. Over 500 families served across 40 states reflects a track record built on personalized service, not generic plan recommendations. Reach out to Sageshieldassurance before your next enrollment window closes.

FAQ

What is individual health coverage in simple terms?

Individual health coverage is health insurance you buy directly for yourself or your family, not through an employer or government program. You choose the plan, pay the premium, and own the policy regardless of your employment status.

Is individual health insurance required by law?

No federal mandate currently requires you to carry individual health insurance, though some states including California, Massachusetts, and New Jersey impose their own penalties for going uninsured. The financial risk of going without coverage is the more practical concern for most self-employed individuals.

Can self-employed individuals deduct health insurance premiums?

Self-employed individuals can deduct 100% of health insurance premiums for themselves and their families from federal taxable income. This deduction applies whether or not you purchase through the ACA Marketplace and does not require itemizing.

What is an ICHRA and who benefits from it?

An ICHRA is an employer-funded arrangement that reimburses employees tax-free for individual health insurance premiums. Small business owners benefit by controlling their benefits budget without managing a group plan, while employees gain the freedom to choose their own coverage.

Are off-exchange health plans safe to buy?

Some off-exchange plans are ACA-compliant and carry full consumer protections. Others, including short-term plans and fixed indemnity products, can lack essential health benefits and may deny claims for pre-existing conditions. Always verify ACA compliance before purchasing any off-exchange plan.

Leave a Reply