Disability Insurance Self-Employed Setup: 2026 Guide

Disability insurance for self-employed workers is defined as a policy that replaces 50–70% of your income when illness or injury stops you from working. Unlike employees, you have no employer-provided safety net, so a disability insurance self-employed setup requires you to arrange every detail yourself. Providers like Guardian and Thrivent offer individual long-term disability policies built for this purpose. Social Security Disability Insurance (SSDI) exists as a fallback, but its approval process is slow and benefits are modest. Individual LTD policies typically cost 1%–3% of your annual income in premiums. That cost is manageable when you understand what you are buying and why.

What policy setup choices should self-employed people understand?

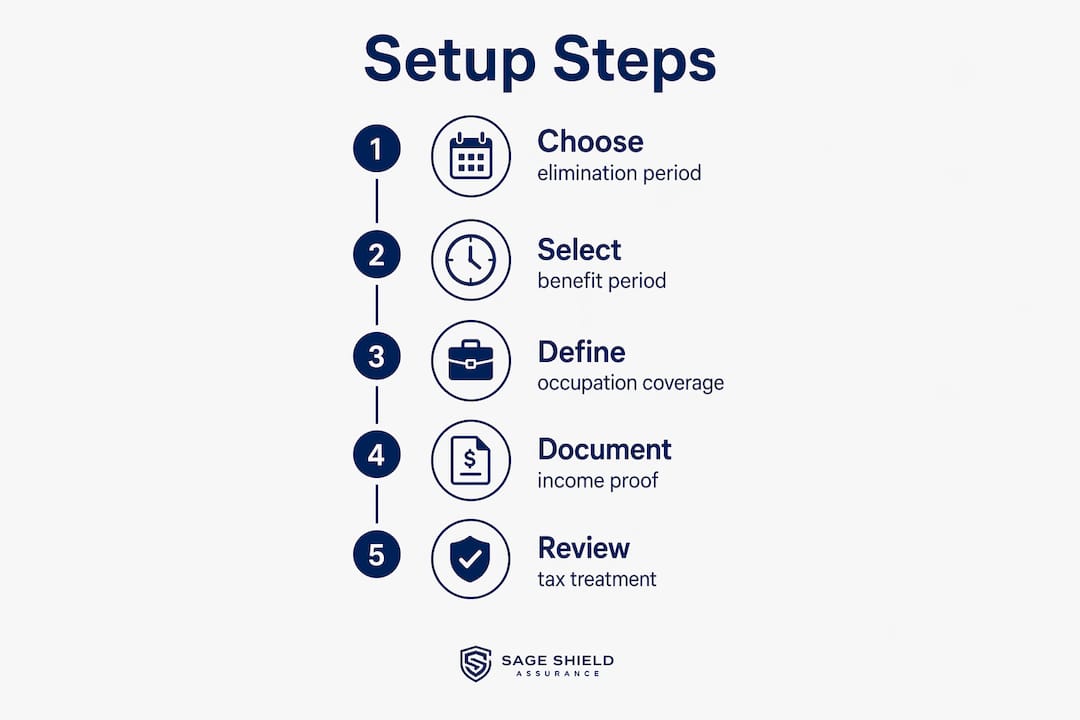

The three variables that shape every disability policy are the elimination period, the benefit period, and the occupation definition. Getting these right determines both your premium cost and whether a claim actually pays out when you need it.

Elimination period: your self-insurance window

The elimination period is the waiting period between when your disability starts and when benefits begin. Options run from 30 to 365 days. A 90-day elimination period is widely considered the balance point between cost and coverage. The catch is that 90 days is also a self-insurance period. You must cover your fixed costs from savings during that window. Choosing a 30-day period lowers your risk exposure but raises your premium significantly.

Benefit period: how long coverage lasts

Benefit periods come in fixed terms of 2, 5, or 10 years, or they extend to retirement age at 65 or 67. A 2-year benefit period costs less but leaves you exposed if a serious condition keeps you out of work longer. For most self-employed individuals, a benefit period to age 65 offers the strongest protection relative to the risk. The longer the benefit period, the higher the premium, so model this against your actual financial obligations.

Own-occupation vs. any-occupation definitions

Own-occupation coverage pays benefits if you cannot perform the specific duties of your current profession, even if you could work in another field. Any-occupation coverage only pays if you cannot work in any job at all. Own-occupation is the stronger protection, especially for specialists like dentists, architects, or consultants. It also raises premiums because the claim bar is lower. For most self-employed professionals, own-occupation is worth the extra cost.

Pro Tip: If you work in a manual or high-risk profession, expect higher premiums regardless of the benefit period you choose. Age, health, and occupation class all factor into your final rate.

How do you document income to qualify for coverage?

Insurers require proof of stable, documented income before they will underwrite a disability policy for a self-employed applicant. This step trips up more freelancers and sole proprietors than any other part of the process.

The standard documentation package includes:

- Tax returns: Most insurers want 2–3 years of Schedule C filings to assess your average net income.

- Profit and loss statements: These matter most if your business is newer than two years old.

- Bank statements: Some underwriters accept 12 months of business bank records as supplemental evidence.

- Business structure documentation: An LLC operating agreement or sole proprietor registration confirms how your income flows.

Insurers look for income consistency, not just totals. A year with a large spike followed by a slow year raises underwriting flags. If your income varies widely, be prepared to explain the business reason in writing.

Pro Tip: If you are in your first year of self-employment, apply for a smaller initial benefit amount and plan to increase coverage once you have two full years of tax returns. Many policies include a future increase option that lets you add coverage without new medical underwriting.

What government disability programs can self-employed workers access?

SSDI is the federal disability program most self-employed workers know by name but few understand in practice. Qualifying is harder than most people expect.

Here is how SSDI eligibility works for self-employed individuals:

- Pay self-employment taxes. You must have paid Social Security taxes through self-employment income to accumulate work credits. No credits mean no SSDI eligibility.

- Meet the substantial gainful activity (SGA) test. The SSA evaluates work activity based on the value of services you perform, not just your reported income. This catches people who reduce their reported earnings to appear disabled.

- Satisfy the duration requirement. Your condition must be expected to last at least 12 months or result in death.

- Survive the approval process. Initial SSDI denials are common. The average approval timeline runs well over a year.

Private disability insurance fills the gaps SSDI leaves open. Benefits start faster, replace a higher percentage of income, and are tailored to your specific occupation. SSDI average monthly benefits are modest and rarely replace the income a successful self-employed professional depends on. Treat SSDI as a last resort, not a primary plan.

How does tax treatment affect your disability premiums and benefits?

The tax rules around disability insurance for self-employed individuals are counterintuitive and often misunderstood. Getting them wrong can cost you money in either premiums or unexpected tax bills.

Here is what the IRS actually says:

- Personal disability insurance premiums are not deductible. Under IRC Section 162(l), self-employed disability premiums do not qualify for the health insurance deduction that medical premiums enjoy.

- Premiums paid with after-tax dollars produce tax-free benefits. If you pay premiums from your own pocket without a deduction, any benefits you receive during a claim are generally not taxable income.

- Business overhead expense (BOE) insurance is different. BOE policies cover your business operating costs during a disability, and those premiums are deductible as a business expense. The benefits, however, are then taxable.

The after-tax premium and tax-free benefit relationship is often misunderstood. Documenting your premium payments carefully ensures your benefits stay tax-free and your planning assumptions hold up at claim time.

Model your after-tax premium cost before you commit to a policy. A $3,000 annual premium paid with after-tax dollars is the real cost. Knowing that your benefit will arrive tax-free makes the math work in your favor during a claim. You can also explore how health insurance deductions interact with disability premiums to build a complete picture of your insurance tax strategy.

What are the practical steps to set up and maintain your coverage?

A successful disability insurance self-employed setup follows a clear sequence. Skipping steps creates gaps that show up at the worst possible time.

- Assess your income risk. Calculate your monthly fixed obligations: rent or mortgage, business overhead, loan payments, and living expenses. This number is your minimum benefit target.

- Build an emergency fund sized to your elimination period. A 90-day elimination period requires roughly three months of expenses in liquid savings before you buy the policy. Without that buffer, a short-term disability becomes a financial crisis before benefits even start.

- Gather your income documents. Pull your last two to three years of tax returns, your most recent profit and loss statement, and three to six months of bank statements. Having these ready speeds up underwriting.

- Shop policies with three variables in mind. Compare elimination period, benefit period, and occupation definition across at least three carriers. Guardian, Thrivent, and other major carriers each price these variables differently based on your occupation class.

- Model the after-tax cost before signing. Confirm that the annual premium fits your budget after taxes. Check whether a BOE policy makes sense alongside your personal disability coverage if you have significant business overhead.

- Review your policy annually. As your income grows, your coverage amount may fall short. Most policies offer a future increase option. Use it when your income rises materially.

The most common mistake self-employed workers make is choosing the shortest elimination period without the savings to back it up. A 30-day elimination period costs more in premiums and still leaves you scrambling if your savings are thin. The 90-day period with a funded emergency account is the more financially sound approach.

Pro Tip: Treat your disability policy like a subscription that protects your entire business model. Viewing disability insurance as an ongoing cash-flow management tool, not a one-time purchase, keeps you from letting coverage lapse during a slow revenue quarter.

For additional ways to reduce your total insurance costs, the self-employed cost reduction guide at Sageshieldassurance covers strategies that apply directly to disability and health coverage together.

Key takeaways

Disability insurance for self-employed individuals requires deliberate policy design, documented income, and after-tax premium planning to deliver reliable income protection when you need it most.

| Point | Details |

|---|---|

| Income replacement target | Policies replace 50–70% of income; calculate your monthly obligations to set the right benefit amount. |

| Elimination period strategy | A 90-day elimination period works best when backed by three months of liquid emergency savings. |

| Own-occupation definition | Choose own-occupation coverage if your income depends on a specific professional skill set. |

| Tax treatment reality | Personal disability premiums are not deductible, but after-tax premiums produce tax-free benefits at claim time. |

| Annual policy review | Update your coverage amount whenever your income grows to avoid being underinsured as your business scales. |

Why most self-employed people get this wrong from the start

Most freelancers and sole proprietors I have worked with treat disability insurance as a checkbox. They buy the cheapest policy they can find, file it away, and never look at it again. That approach almost always produces the wrong coverage at the wrong price.

The mindset shift that actually protects you is treating disability coverage as a cash-flow management tool. Your policy is not a one-time decision. It is a financial instrument that needs to match your current income, your current obligations, and your current risk tolerance. A policy that fit your business at $60,000 in annual revenue is probably underinsured at $120,000.

The second mistake I see constantly is ignoring the elimination period math. People choose a 30-day period because it feels safer, but they have no savings to cover even 30 days of expenses. The result is a higher premium and no actual financial cushion. The 90-day period with a funded emergency account is almost always the better structure.

Working with a broker who specializes in self-employed clients makes a real difference here. A generalist broker will hand you a standard policy. A specialist will ask about your occupation class, your business overhead, your tax situation, and your income trajectory. Those questions produce a policy that actually works.

The uncomfortable truth is that most self-employed workers are one serious injury or illness away from a financial crisis. Disability insurance does not eliminate that risk. It converts an unpredictable catastrophe into a manageable, planned-for event. That is worth every dollar of the premium.

— mkaravas1m

How Sageshieldassurance helps you get coverage right

Sageshieldassurance specializes in disability and health insurance for self-employed individuals and business owners across 40 states. Their team reviews your income documentation, occupation class, and financial obligations before recommending a policy structure. That process eliminates the guesswork that leads most self-employed workers to buy the wrong coverage.

Whether you need a personal long-term disability policy, a business overhead expense plan, or both, Sageshieldassurance connects you with leading carriers and walks you through every variable. Explore your tailored insurance options and get a policy review built around your specific business and income situation.

FAQ

What does disability insurance self-employed setup actually involve?

Setting up disability insurance as a self-employed person means selecting an elimination period, benefit period, and occupation definition, then submitting income documentation for underwriting. The process typically takes two to four weeks from application to policy issuance.

How much does freelancer disability insurance cost per year?

Individual long-term disability premiums typically run 1%–3% of your annual income. A self-employed person earning $80,000 per year should budget roughly $800–$2,400 annually for coverage.

Can self-employed individuals qualify for SSDI?

Yes, self-employed individuals can qualify for SSDI if they have paid self-employment taxes and meet the SSA’s substantial gainful activity test. The SSA evaluates actual work activity, not just reported income, when assessing eligibility.

Are disability insurance premiums tax-deductible for the self-employed?

Personal disability insurance premiums are generally not deductible for self-employed individuals under current IRS rules. Paying premiums with after-tax dollars means your disability benefits are typically received tax-free when you file a claim.

What is the best disability policy for self-employed professionals?

The best policy combines own-occupation coverage, a 90-day elimination period backed by emergency savings, and a benefit period extending to age 65. Carriers like Guardian and Thrivent offer individual policies structured specifically for self-employed applicants.

Leave a Reply