Dental Insurance for Self-Employed: 2026 Guide

Dental insurance for self-employed individuals is supplemental health coverage that pays for routine cleanings, fillings, and major procedures like crowns or oral surgery when no employer-sponsored plan exists. Freelancers, consultants, and independent contractors must source this coverage entirely on their own, which means navigating the individual insurance market without the group-rate advantages employees receive. Providers like Aflac and Humana offer standalone dental plans specifically designed for this audience. Beyond protecting your teeth, dental coverage functions as a financial planning tool. An unexpected root canal without insurance can cost $1,500 or more out of pocket, a hit that disrupts any freelancer’s cash flow.

What is dental insurance for self-employed professionals?

Dental insurance for self-employed professionals is a private coverage contract between you and an insurer that reimburses a portion of dental care costs in exchange for monthly premiums. The industry standard term is “individual dental insurance,” and it operates on the same basic structure as group plans but without an employer subsidizing the premium. Coverage typically follows a three-tier model: preventive care (cleanings, X-rays) covered at 80 to 100%, basic procedures (fillings, extractions) covered at 70 to 80%, and major procedures (crowns, bridges, dentures) covered at 50%. Annual maximums, usually between $1,000 and $2,000, cap what the insurer pays per year.

Self-employed individuals face a specific challenge: they absorb every dollar of premium increase directly. Premium spikes impact self-employed budgets significantly in the 2026 marketplace, making plan selection more consequential than it is for salaried workers. Routine dental care also prevents systemic health issues, including cardiovascular complications linked to untreated gum disease, which means skipping coverage creates both health and financial risk. Preventive dental care reduces the likelihood of costly future treatments, reinforcing why coverage is a sound investment rather than an optional expense.

How do self-employed individuals qualify for dental insurance and tax deductions?

Eligibility for individual dental insurance is straightforward: you must be self-employed, earn a net profit from your business, and not have access to an employer-sponsored plan through a spouse or your own business (beyond yourself and family members). The tax benefit attached to this coverage is one of the most underused advantages available to freelancers.

Eligible self-employed individuals can deduct 100% of dental insurance premiums for themselves, their spouses, and their dependents on Form 1040, line 17. This deduction reduces your Adjusted Gross Income (AGI), which lowers your federal income tax liability. The deduction is capped at your net business profit for the year, so a loss year eliminates the benefit. There is no dollar ceiling on the deduction as of 2026, meaning high-premium family plans are fully deductible if profit supports it.

One critical nuance trips up many freelancers: deductions reported on Form 1040 line 17 do not reduce self-employment (SE) tax, which is calculated on Schedule SE from net business income. You still pay SE tax on the full profit figure. This distinction matters for accurate tax planning, particularly when estimating quarterly payments.

Key eligibility requirements at a glance:

- You are self-employed with net profit from a sole proprietorship, partnership, or S-corporation

- You are not eligible for coverage through an employer (including a spouse’s employer plan)

- The deduction cannot exceed net business income for the tax year

- Family members covered under your plan qualify for the same deduction

Pro Tip: File the dental premium deduction on Form 1040 line 17, not on Schedule C. Placing it on Schedule C is a common error that overstates business expenses and can trigger IRS scrutiny.

What types of dental plans are available for self-employed professionals?

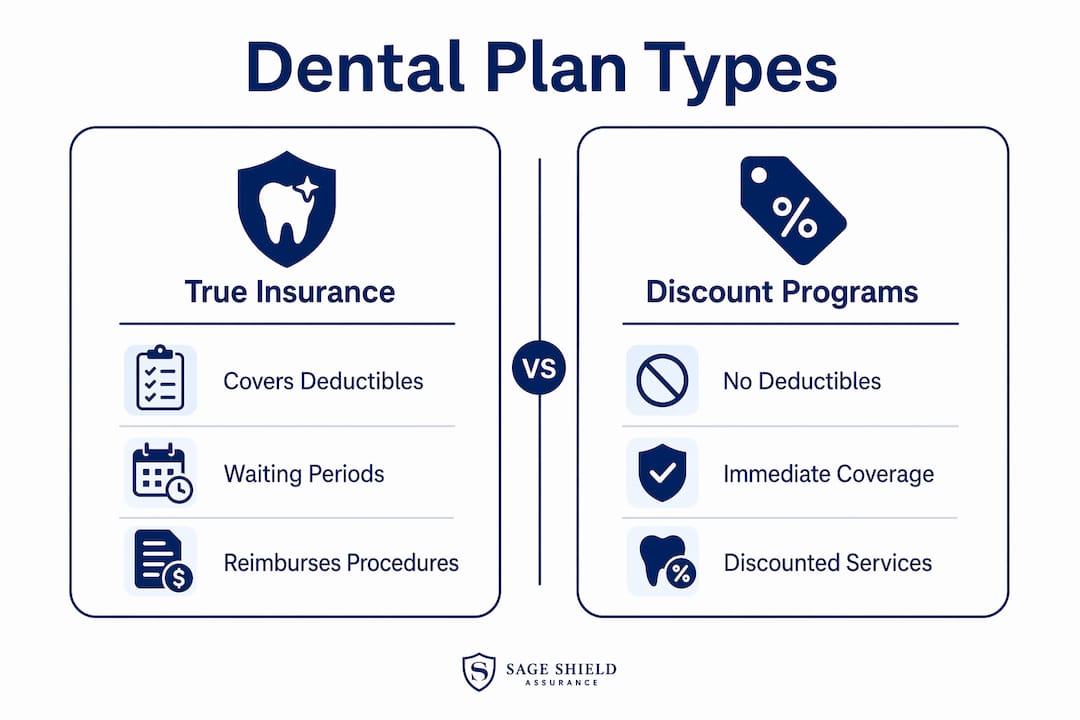

Self-employed dental plans fall into two broad categories: true insurance and dental discount programs. Understanding the difference prevents a costly mistake.

True dental insurance pays a percentage of covered procedures after you meet a deductible. Plans come as standalone dental policies or as dental riders attached to a medical plan. Standalone plans from carriers like Delta Dental or Humana offer more flexibility in network and coverage depth. Riders bundled with self employed health insurance with dental coverage can simplify billing but may limit your dentist choices.

Dental discount programs are not insurance. Discount programs eliminate deductibles and waiting periods but offer only negotiated service rates at participating dentists. You pay the discounted fee entirely out of pocket. There is no reimbursement. For someone who needs only two cleanings a year, a discount plan can save money. For anyone facing a crown or implant, the lack of coverage becomes a serious financial exposure.

The table below summarizes the main plan types available to self-employed professionals:

| Plan type | Coverage | Waiting periods | Best for |

|---|---|---|---|

| Standalone dental insurance | Preventive, basic, major procedures | 6 to 12 months for major work | Comprehensive protection |

| Dental rider on medical plan | Varies by carrier | Often shorter | Bundled simplicity |

| Dental discount program | None (negotiated rates only) | None | Preventive-only needs |

| Dental HMO (DHMO) | Full coverage within network | Minimal | Low-cost, in-network users |

| Dental PPO | Flexible in and out of network | Standard | Network flexibility |

Waiting periods commonly range 6 to 12 months for major procedures, which means a plan purchased today will not cover a crown until next year. This is the most overlooked trap in individual dental coverage. If you need significant work soon, prioritize plans with shorter or waived waiting periods, even if premiums run higher.

How to choose the best dental insurance plan for your situation

Choosing the best dental insurance for self-employed individuals requires matching coverage structure to your actual dental history and cash flow reality. Follow these steps to make a sound decision:

-

Audit your dental history. Review the past two years of dental work. If you have had only cleanings, a lower-premium plan with strong preventive coverage may suffice. If you have crowns, bridges, or orthodontic needs in your future, prioritize major procedure coverage.

-

Check the annual maximum. Most plans cap annual benefits at $1,000 to $2,000. If you anticipate significant work, look for plans with higher maximums or no maximum on preventive care.

-

Prioritize direct billing. Plans with direct dentist billing protect cash flow by avoiding upfront payments and reimbursement delays. For freelancers with irregular income, this is not a minor convenience. It is a budget management tool.

-

Verify network coverage in your area. A Delta Dental PPO plan with 90,000 participating dentists nationwide offers far more geographic flexibility than a regional DHMO. Confirm your current dentist is in-network before enrolling.

-

Include family members. Adding a spouse and dependents to your plan is typically more cost-effective than separate individual policies. Confirm the premium deduction extends to all covered family members on your tax return.

-

Review annually. Regularly reviewing dental plans helps freelancers adjust to premium changes and coverage updates, maintaining budget control as income and health needs shift.

Pro Tip: Never choose a plan based on monthly premium alone. A $15 per month plan with a 12-month waiting period for major procedures offers zero protection if you need a root canal in month three. Calculate your realistic annual dental spend before comparing premiums.

Balanced coverage focusing on prevention helps self-employed individuals avoid costly out-of-pocket treatments. The goal is not the cheapest plan. The goal is the plan that costs least when you actually use it.

What costs and coverage gaps should self-employed individuals expect?

Premium cost variability is the defining financial reality of dental coverage for freelancers. Unlike employees who pay a fixed share of a group rate, self-employed individuals face the full individual market price, which fluctuates with age, location, and carrier competition.

Approximately 24% of Maryland adults lacked dental coverage in 2024, a figure that reflects a national pattern of coverage gaps concentrated among the self-employed and gig workers. That gap is not accidental. Individual market premiums are higher, and without an employer absorbing 50 to 80% of the cost, many freelancers opt out entirely.

“The biggest financial risk for self-employed individuals is not the monthly premium. It is the emergency dental visit that arrives without warning and without coverage.”

The table below outlines common coverage gaps and their financial impact:

| Coverage gap | Typical out-of-pocket cost | Risk level |

|---|---|---|

| No major procedure coverage | $800 to $3,000 per crown | High |

| Annual maximum exhausted | Full cost of remaining procedures | High |

| Waiting period not met | 100% cost of major work | Medium to high |

| Out-of-network dentist | 20 to 50% higher cost-sharing | Medium |

| Cosmetic procedures excluded | Full cost (no coverage) | Low to medium |

Out-of-pocket maximums and deductibles vary widely. A plan with a $100 deductible and 50% coverage for major procedures still leaves you paying $1,000 on a $2,200 implant. Budget for this gap explicitly, particularly in years when you anticipate significant dental work. Dental savings accounts or a dedicated emergency fund can absorb costs that insurance does not cover. You can also maximize dental cleaning savings by using your preventive benefits fully each year, since most plans cover two cleanings at 100% regardless of deductible status.

Key takeaways

Self-employed individuals who treat dental insurance as a tax-deductible health investment, not just an expense, protect both their physical health and their business cash flow.

| Point | Details |

|---|---|

| Full premium deductibility | Deduct 100% of dental premiums on Form 1040 line 17, capped at net business profit. |

| SE tax is unaffected | The deduction lowers AGI but does not reduce self-employment tax on Schedule SE. |

| Waiting periods are a real trap | Major procedure waiting periods of 6 to 12 months can leave you unprotected when you need care most. |

| Discount plans are not insurance | Dental discount programs offer no reimbursement and provide no financial protection for major procedures. |

| Annual review is non-negotiable | Premium changes and health shifts require yearly plan reassessment to maintain cost-effective coverage. |

Why I think most freelancers get dental insurance completely backward

Most self-employed individuals I have observed approach dental insurance the same way they approach car insurance: they look for the lowest monthly payment and assume they will deal with problems when they arise. That logic works for fender benders. It fails completely for a $4,000 dental implant.

The smarter frame is to treat dental coverage as a cash flow hedge. The question is not “what is the cheapest plan?” It is “what is my maximum acceptable out-of-pocket dental expense in a bad year?” Work backward from that number to find a plan that keeps you inside it. A $40 per month premium difference is $480 per year. One uninsured crown costs three times that.

I have also seen freelancers skip annual plan reviews for three or four years running, then discover their carrier changed the network or raised the annual maximum. Working with a trusted brokerage removes that blind spot. A broker who specializes in self-employed coverage tracks these changes on your behalf and flags when a better option exists. That service pays for itself the first time it catches a coverage downgrade you would have missed.

The tax deduction angle is also chronically underused. Freelancers who bundle dental with a broader private health insurance strategy can reduce AGI meaningfully, which cascades into lower tax brackets, reduced student loan payments tied to income, and better eligibility for income-based programs. Dental insurance is not a standalone decision. It is one piece of a coordinated financial picture.

— mkaravas1m

How Sageshieldassurance helps self-employed individuals find the right dental plan

Self-employed professionals deserve dental coverage that fits their income pattern, health history, and family needs. Sageshieldassurance specializes in exactly this.

Sageshieldassurance has served over 500 families across 40 states, matching freelancers and business owners with dental and health insurance plans that balance premium cost against real coverage depth. Their brokers review your current plan annually, flag coverage gaps before they become financial emergencies, and negotiate across leading carriers to find options you would not find searching alone. If you are self-employed and unsure whether your current dental coverage actually protects you, a personalized consultation with Sageshieldassurance is the most efficient next step you can take.

FAQ

What is dental insurance for self-employed individuals?

Dental insurance for self-employed individuals is a private coverage contract that reimburses a portion of dental care costs, including preventive, basic, and major procedures, purchased directly on the individual market without employer contribution.

Can self-employed individuals deduct dental insurance premiums?

Yes. Eligible self-employed individuals deduct 100% of dental premiums for themselves, spouses, and dependents on Form 1040 line 17, reducing AGI up to the amount of net business profit.

What is the difference between dental insurance and a dental discount plan?

Dental insurance reimburses a percentage of covered procedure costs after a deductible. Dental discount programs offer only negotiated rates with no reimbursement, making them unsuitable for anyone facing major dental work.

How do waiting periods affect self-employed dental coverage?

Waiting periods of 6 to 12 months for major procedures mean a newly purchased plan will not cover crowns, bridges, or dentures until that period expires. Freelancers who need immediate major work should prioritize plans with waived or shortened waiting periods.

Do self-employed individuals need dental insurance if they are healthy?

Yes. Even without current dental problems, routine preventive care prevents systemic health complications and costly future treatments. The tax deductibility of premiums also makes coverage financially advantageous regardless of current dental health.

Leave a Reply