Business Life Insurance Policy Guide for Self-Employed Owners

If you run your business solo or with a small team, you are the business. That means a solid business life insurance policy guide is not optional reading. It is the difference between your company surviving a crisis and dissolving overnight. This guide covers everything self-employed owners need to know: the right policy types, how to calculate coverage accurately, the tax rules that trip people up, and how to buy a policy without leaving gaps that could cost your family or your partners everything.

Table of Contents

- Key takeaways

- Your business life insurance policy guide starts here

- Calculating how much coverage you actually need

- How to buy and structure a business life policy

- Tax implications, employee benefits, and risk management

- My honest take on business life insurance for self-employed owners

- How Sageshieldassurance helps you get covered right

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Know your policy types | Key person insurance, buy-sell agreements, and group life serve distinct purposes for self-employed owners. |

| Base coverage on valuation | Use a formal business valuation, not guesswork, to set defensible and accurate coverage amounts. |

| Consent is legally required | IRS Section 101(j) requires written consent from insured employees to keep death benefits tax-free. |

| Premiums are not deductible | Company-owned policy premiums are generally not tax-deductible, but death benefits are income tax-free when structured correctly. |

| Review policies annually | Your business changes every year, and your coverage needs to keep pace with those changes. |

Your business life insurance policy guide starts here

Understanding business life insurance begins with recognizing what it is not. It is not the same as your personal life insurance policy. Personal coverage protects your family’s income if you die. Business life insurance protects the entity you built, the people who depend on it, and the financial obligations tied to it.

For self-employed owners, three policy types do most of the heavy lifting:

- Key person insurance: The business owns the policy and is the beneficiary. If you or another critical person dies, the payout helps the company cover lost revenue, recruit a replacement, or wind down responsibly.

- Buy-sell agreement funding: If you have a business partner, a life insurance policy funds the buyout of a deceased partner’s share. Without this, surviving partners may be forced to work alongside the deceased’s heirs or sell assets under pressure.

- Group life insurance: If you have employees, offering group coverage is a low-cost benefit that builds loyalty and rounds out your total compensation package.

The core difference between personal and business coverage comes down to ownership and purpose. In a business policy, the company is typically the owner and beneficiary. That structure has real tax and legal implications, which we will cover in detail below. The goal of business life coverage options is to protect continuity, not just replace income.

Calculating how much coverage you actually need

This is where most self-employed owners get into trouble. They either guess a round number or copy what a friend told them. Neither approach holds up.

Business coverage calculations are fundamentally different from personal insurance math. You cannot simply multiply your salary by ten and call it done. Your business has its own financial profile: equity value, outstanding debt, operating reserves, and the cost of replacing your specific skills or relationships.

Here is what a proper coverage assessment looks like:

- Business equity: What is your ownership stake worth if the business were sold today?

- Outstanding debt: Loans, lines of credit, and lease obligations the business carries.

- Operating reserves: How many months of expenses would the business need to survive a transition?

- Key person replacement cost: Recruiting, onboarding, and lost revenue during the gap period.

For key person policies specifically, coverage typically ranges from 5 to 10 times the key employee’s annual compensation, with many small businesses landing between $500,000 and $3 million. That range exists because the right number depends on your specific business model, not a formula applied blindly.

A formal business valuation by a CPA or experienced broker can typically be completed in about two weeks and gives you a defensible, accurate number. That matters not just for coverage but for legal purposes if the policy is ever challenged.

Pro Tip: Never set your coverage amount without involving your CPA. The valuation process surfaces debts and liabilities that are easy to overlook, and an underinsured policy can create a financial crisis at exactly the wrong moment.

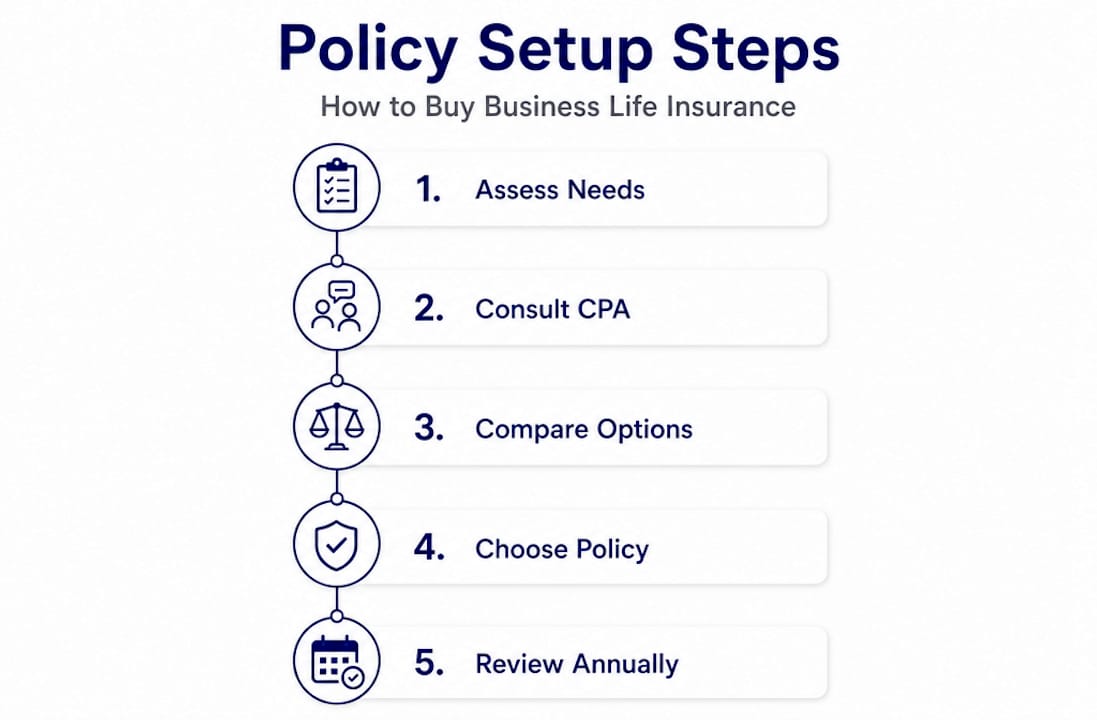

How to buy and structure a business life policy

Buying a business life insurance policy is not the same as buying personal term coverage online in fifteen minutes. There are legal, tax, and structural decisions that have lasting consequences. Here is how to do it right.

Step-by-step purchasing process

- Identify the policy type you need. Start with your specific risk: key person loss, partner buyout, or employee benefits. Each requires a different policy structure.

- Get a formal business valuation. Before you talk to any insurer, know your numbers. This prevents you from buying too little or overpaying for coverage you do not need.

- Work with a licensed broker. A broker shops multiple carriers on your behalf, which almost always produces better rates and terms than going direct to a single insurer.

- Complete underwriting requirements. Business policies require medical exams, financial statements, and sometimes business tax returns. Prepare these in advance to avoid delays.

- Obtain written consent from insured employees. Under IRS Section 101(j), any employee-insured policy requires a signed notice and consent form before the policy is issued. Skip this step and the death benefit becomes taxable income to the business.

- Set ownership and beneficiary designations carefully. The business should typically be both owner and beneficiary for key person policies. For buy-sell funding, the structure depends on whether you use a cross-purchase or entity-purchase agreement.

- Coordinate with your estate attorney. Policy ownership affects your estate, your buy-sell agreement language, and your succession plan. These documents need to align.

- Schedule annual reviews. Your coverage needs change as your business grows, takes on debt, or adds key people.

Here is a quick comparison of the two main buy-sell structures:

| Structure | Who owns the policy | Who pays premiums | Best for |

|---|---|---|---|

| Cross-purchase | Each partner owns a policy on the other | Each partner individually | Small partnerships with 2-3 owners |

| Entity-purchase | The business owns all policies | The business | Larger partnerships or corporations |

Pro Tip: Permanent life insurance policies, such as whole life or universal life, build cash value over time. That cash value can be used to fund buy-sell agreements or executive compensation plans, giving your policy a dual purpose beyond just the death benefit.

One common mistake is treating the policy as a set-and-forget purchase. Annual coordination with legal and financial advisors keeps your coverage aligned with changes in your buy-sell agreements and current tax law.

Tax implications, employee benefits, and risk management

Tax treatment you need to understand

The tax rules around business life insurance catch a lot of owners off guard. Here is the short version: premiums for company-owned policies are generally not tax-deductible. The tradeoff is that death benefits are received income tax-free, provided the policy was structured correctly and the Section 101(j) consent requirements were met.

Group life insurance for employees works differently. Premiums are tax-deductible for the employer on the first $50,000 of coverage per employee, and typical costs run $10 to $15 per employee per month for a $50,000 policy. That is an affordable benefit with a real tax advantage.

Adding group coverage for your team

If you have employees, group life insurance is one of the most cost-effective benefits you can offer. Beyond the tax deduction, group policies offer guaranteed issue coverage with no medical underwriting up to a set limit. That means employees with pre-existing conditions can still get covered, which matters when you are competing for talent.

Fitting life insurance into your broader risk strategy

Life insurance does not exist in a vacuum. About 40% of small businesses face a property or liability claim within ten years, and over one-third of small US businesses are underinsured. Life insurance is one layer of a complete protection strategy that should also include liability, property, and health coverage.

For self-employed owners, your private health insurance coverage and your life insurance strategy are closely connected. Both protect your ability to keep working and keep your business running.

Hybrid and remote work arrangements also introduce new coverage considerations. If your team works across state lines or your business model has shifted since you last reviewed your policies, those changes may affect your coverage needs in ways that are not obvious until a claim surfaces.

My honest take on business life insurance for self-employed owners

I have worked with enough self-employed business owners to spot the pattern clearly. Most people delay this decision because it feels abstract. You are busy running your business, and the idea of planning for your own death or incapacity feels like a problem for future you.

What I have seen in practice is that the owners who regret waiting are not the ones who bought too much coverage. They are the ones who had a partner die without a funded buy-sell agreement, or who lost a key employee and had no financial cushion to absorb the blow.

The other mistake I see constantly is treating coverage amounts like a guess. Picking a number that sounds big enough is not a strategy. The formal valuation process exists for a reason, and skipping it is the single most common way owners end up underinsured when it actually matters.

My honest advice: treat your business life insurance the same way you treat your most important client contract. Read it carefully, get the right people involved, and revisit it every year. The cost of doing this right is small compared to what you are protecting. The trusted brokerage approach to finding coverage is not just about price. It is about getting the structure right the first time.

— mkaravas1m

How Sageshieldassurance helps you get covered right

Sageshieldassurance works specifically with self-employed business owners and small business teams who need more than a generic policy. The team helps you identify the right policy type, run a proper coverage assessment, and shop competitive rates across multiple carriers. From key person insurance to group life and annuities, the full range of services is built around your business structure, not a one-size-fits-all product. If you are ready to stop guessing and start building real protection, schedule a consultation to get a personalized coverage review from an advisor who understands the self-employed owner’s situation.

FAQ

What is a business life insurance policy?

A business life insurance policy is a contract where the business is the owner and beneficiary, designed to protect the company from financial loss due to the death of a key person or to fund ownership transitions through buy-sell agreements.

How much key person coverage does a small business need?

Key person coverage typically ranges from 5 to 10 times the key employee’s annual compensation, with most small businesses selecting policies between $500,000 and $3 million depending on the individual’s role and revenue impact.

Are business life insurance premiums tax-deductible?

Generally, premiums on company-owned life insurance policies are not tax-deductible. However, death benefits are received income tax-free when the policy is properly structured and IRS Section 101(j) consent requirements are satisfied.

What happens without a funded buy-sell agreement?

Without a life insurance-funded buy-sell agreement, surviving partners may be forced to accept the deceased partner’s heirs as co-owners or liquidate business assets quickly to buy out the estate, often at a significant financial loss.

How often should I review my business life insurance policy?

You should review your policy at least once a year, or any time your business takes on significant new debt, adds a key employee, or changes its ownership structure. Annual reviews with your CPA and attorney keep coverage aligned with your current business reality.

Leave a Reply