Income Protection Plan for Self-Employed: 2026 Guide

An income protection plan for the self-employed is defined as an insurance policy that pays a regular, tax-free benefit when illness or injury stops you from working. Unlike salaried employees, self-employed workers lack sick pay entirely, meaning your income stops the moment you cannot work. The industry standard term is income protection insurance, though you may also hear it called permanent health insurance or PHI. Policies typically replace 50% to 70% of gross income, and because most self-employed people pay premiums from after-tax money, those benefits arrive free of income tax. That tax treatment means a policy covering 60% of your gross income closely mirrors your actual take-home pay, making it one of the most efficient self-employed safety net tools available.

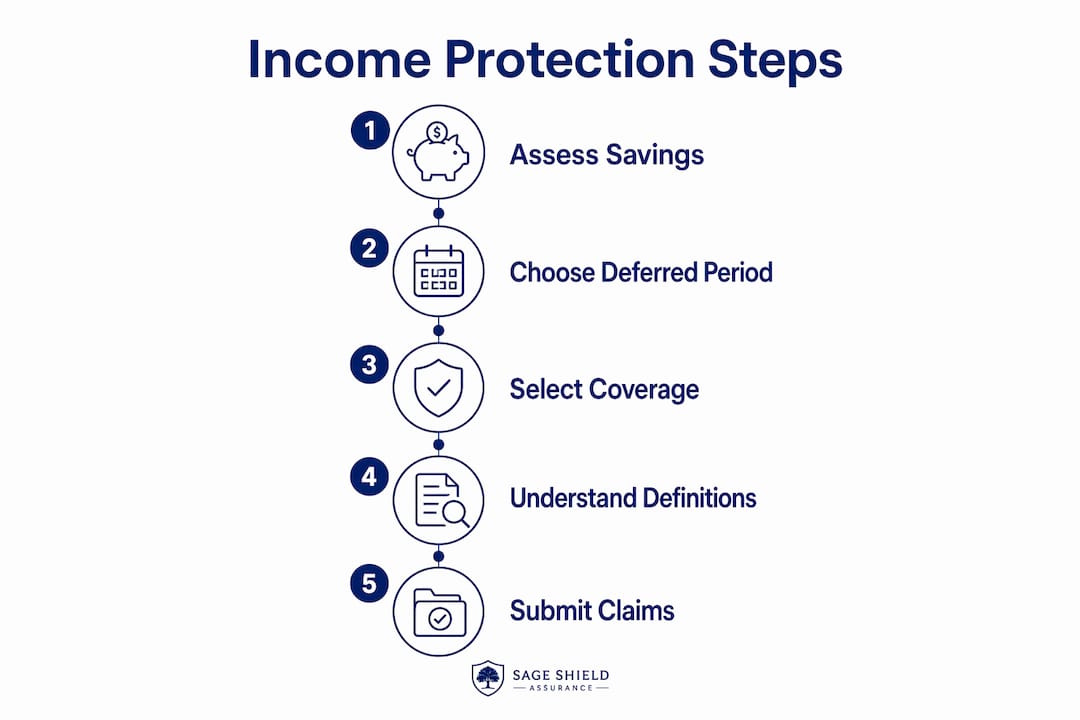

What are the key features of an income protection plan for self-employed workers?

Understanding the mechanics of income protection insurance before you buy prevents expensive surprises at claim time. Four components drive how a policy performs: the deferred period, the benefit amount, the benefit period, and the occupation definition.

The deferred period is the gap between when you stop working and when the insurer starts paying. Options typically run from 4 weeks to 52 weeks. Shorter deferred periods like 4 to 8 weeks cost more in premiums but protect you faster. A 52-week deferred period carries a much lower premium but requires you to fund nearly a year of living expenses from savings.

The benefit amount is capped at roughly 50% to 70% of your pre-disability earnings. Because benefits paid from after-tax premiums are not subject to income tax, the effective replacement rate is higher than the headline percentage suggests. For a freelancer earning $80,000 annually, a 60% benefit delivers $48,000 per year tax-free, which for many people exceeds their net working income after business expenses.

The benefit period is how long the policy pays out per claim. The two main structures are:

- Short-term policies: Pay for 1 to 5 years per claim. Lower premiums, but you face a funding gap if your condition extends beyond the payment window.

- Full-term policies: Cover incapacity until retirement age and provide stronger long-run protection. These cost more but eliminate the risk of benefits expiring mid-illness.

The occupation definition is where many self-employed policyholders get caught off guard. Own-occupation definitions pay benefits if you cannot perform the specific duties of your own job. An “any occupation” definition only pays if you cannot work in any job at all, which is a far higher bar. For a self-employed graphic designer or contractor, own-occupation cover is the only definition that genuinely protects your livelihood.

Pro Tip: Read the small print on how your occupation definition is applied after year two of a claim. Some policies shift from own-occupation to a broader definition after an initial period, which can end your benefits even if you still cannot return to your specific work.

| Feature | What to look for |

|---|---|

| Deferred period | Match to your savings buffer, not the shortest available |

| Benefit amount | Aim for 60% of gross income for near full take-home replacement |

| Benefit period | Full-term policies eliminate long-illness funding gaps |

| Occupation definition | Own-occupation is the gold standard for specialized roles |

How to choose the right income protection plan as a self-employed individual

Choosing the right policy is a financial planning exercise as much as an insurance decision. Work through these steps before comparing quotes.

-

Calculate your monthly floor. Add up rent or mortgage, utilities, food, loan repayments, and any business overhead you must maintain even when not working. This number is your minimum monthly benefit requirement, not your gross income.

-

Audit your savings buffer. How many months can you cover that floor from savings alone? If the answer is three months, a 13-week deferred period is your ceiling. Aligning your deferred period with your savings rather than defaulting to the shortest option keeps premiums manageable without creating a funding gap.

-

Model your income variability. Freelancers and contractors often have feast-and-famine income cycles. Practitioners recommend stress-testing your cash flow by modeling illness onset at different points in your billing cycle. A gap between invoicing and payment collection can mean you run dry faster than your savings balance suggests.

-

Compare benefit period costs. Get quotes for both short-term and full-term policies at the same deferred period. The premium difference is often smaller than people expect, and the long-term protection gap is significant.

-

Review occupation wording carefully. Confirm the policy uses own-occupation language and check whether that definition changes after a set period. Policy occupation definitions can become more restrictive after a fixed duration, which materially affects claim outcomes.

-

Update your insured income after strong years. Many self-employed people set their insured income when they first take out a policy and never revisit it. If your earnings have grown significantly, your original coverage level leaves you underinsured. Review your insured income annually after filing taxes.

Pro Tip: If your income fluctuates, insurers often calculate your insured income based on an average of the last two or three years of earnings. Keep clean financial records so you can demonstrate your true income level at application and at claim time.

How does the application and claims process work?

Applying for income protection insurance as a self-employed person involves more documentation than a standard employee application, because you must prove your income independently.

At application, insurers will ask for:

- Two to three years of tax returns or certified accounts to establish your insured income

- Details of any pre-existing medical conditions, which may result in exclusions or premium loadings

- Your occupation description, including specific duties, since this anchors the own-occupation definition

At claim time, the process follows a defined sequence. You submit a claim form alongside a doctor’s certificate confirming your incapacity. The insurer’s underwriting team then reviews the medical evidence against the policy’s occupation definition. Payment begins after the deferred period ends, provided incapacity continues under the policy terms. Most delays at this stage come from insufficient medical documentation rather than disputed liability.

Keeping detailed records of symptoms and their functional impact on your ability to perform your job duties significantly reduces friction. A physiotherapist’s report, occupational health assessment, or specialist letter that directly maps your condition to your specific job tasks is far more useful than a general sick note.

Pro Tip: Start a simple illness log from day one of any condition that affects your work. Note dates, symptoms, and which job tasks you cannot perform. This contemporaneous record is far more credible to an underwriter than a retrospective account written weeks later.

For self-employed healthcare professionals, resources like direct hire healthcare guides can provide additional context on income structures that affect how insurers calculate your insured income.

How to manage premiums without sacrificing coverage

Premium cost is the most common reason self-employed people either delay buying income protection insurance or buy inadequate coverage. These strategies help you get the protection you need at a price that works.

- Extend your deferred period strategically. The deferred period is the single biggest driver of premium cost. Moving from a 4-week to a 13-week deferred period can reduce your annual premium substantially, provided your savings can cover the gap. Longer deferred periods reduce cost but require you to self-fund for that duration.

- Choose full-term over short-term if budget allows. Short-term policies look cheaper upfront, but if you face a long-term illness, you exhaust benefits and still have no income. Full-term policies cost more monthly but eliminate that catastrophic scenario.

- Review coverage annually. Your income, health, and financial reserves change. An annual review with a broker, like those at Sageshieldassurance, catches both underinsurance and overpayment.

- Do not ignore mental health conditions. Stress, anxiety, and depression are among the most common reasons for long-term work absence. Confirm your policy covers mental health conditions explicitly, since some policies exclude them or apply separate waiting periods.

- Check self-employed insurance cost tips specific to 2026. Tax treatment, available riders, and insurer pricing change year to year, and staying current prevents you from overpaying on an outdated structure.

Key takeaways

A self-employed income protection plan works best when the deferred period matches your savings buffer, the benefit uses own-occupation language, and you review your insured income every year.

| Point | Details |

|---|---|

| Own-occupation definition | Choose own-occupation cover to protect your specific role, not just any job. |

| Deferred period alignment | Match your waiting period to your savings, not the shortest available option. |

| Tax-free benefit advantage | Benefits from after-tax premiums are not taxed, making 60% coverage close to full take-home pay. |

| Annual income review | Update your insured income after strong earnings years to avoid underinsurance. |

| Full-term vs. short-term | Full-term policies eliminate the risk of benefits expiring during a prolonged illness. |

Why most self-employed people get this wrong

Most self-employed professionals I work with make the same two mistakes. They pick the shortest deferred period because it feels safest, and they never update their insured income after a good year. Both decisions cost them money in opposite directions.

The deferred period mistake is understandable. When you have no employer sick pay, a 4-week wait feels terrifying. But if you have three months of expenses in savings, paying for a 4-week deferred period is essentially buying insurance against a risk you have already self-funded. A 13-week deferred period with those same savings costs noticeably less and leaves you no worse off financially.

The underinsurance mistake is quieter but more damaging. A freelancer who earned $60,000 when they took out their policy and now earns $95,000 is insuring a ghost income. If they claim, the payout reflects the original figure, not their current earnings. Updating insured income is a five-minute annual task that most people skip because no one reminds them.

The own-occupation wording issue is the one that genuinely surprises people at claim time. A policy that starts on own-occupation terms but shifts to a broader definition after two years can terminate benefits for a specialist who still cannot return to their specific work. Read that clause before you sign, not after you claim.

Income protection for freelancers is not a luxury product. For anyone without an employer safety net, it is the financial floor that makes every other plan possible.

— mkaravas1m

How Sageshieldassurance helps you find the right coverage

Sageshieldassurance works exclusively with self-employed individuals and business owners to match them with income protection plans that fit both their occupation and their budget. With partnerships across leading insurance providers and clients in 40 states, Sageshieldassurance reviews policy wording, occupation definitions, and deferred period structures so you are not navigating that complexity alone.

Whether you are a freelancer, contractor, or sole proprietor, Sageshieldassurance’s brokers provide a personalized policy review that identifies gaps before they become claims problems. Explore your income protection options or review the full range of self-employed coverage plans to find a structure that protects your income without overextending your budget.

FAQ

What is income protection insurance for self-employed people?

Income protection insurance is a policy that pays a regular, tax-free benefit if illness or injury prevents you from working. For self-employed individuals, it replaces the employer sick pay that salaried workers receive automatically.

How much of my income can an income protection plan cover?

Most policies cover between 50% and 70% of your gross income. Because benefits paid from after-tax premiums are not subject to income tax, a 60% benefit typically approximates your actual take-home pay.

What is a deferred period and how long should mine be?

The deferred period is the waiting time between stopping work and receiving benefits. The right length depends on your savings. If you can cover three months of expenses from savings, a 13-week deferred period balances cost and protection effectively.

Does income protection cover mental health conditions?

Many policies do cover mental health conditions, but coverage varies by insurer. Confirm explicitly that stress, anxiety, and depression are included before purchasing, since some policies apply separate exclusions or extended waiting periods to these claims.

Can I get income protection insurance if I have a pre-existing condition?

Yes, though insurers may exclude the specific condition or apply a premium loading. Sageshieldassurance brokers can review pre-existing condition coverage options to identify policies with the most favorable terms for your situation.

Leave a Reply