HDHP Benefits for Self-Employed: 2026 Tax Guide

A high-deductible health plan (HDHP) is a health insurance policy with higher annual deductibles and lower monthly premiums that qualifies self-employed individuals for two powerful tax advantages: the Health Savings Account (HSA) and the Self-Employed Health Insurance (SEHI) deduction. For freelancers, independent contractors, and sole proprietors paying full premium costs out of pocket, HDHP benefits for self-employed workers go well beyond simple premium savings. The 2026 IRS updates expand HSA eligibility to ACA Bronze and Catastrophic plans, opening new options on the Marketplace. Understanding how these tools work together is the difference between paying too much for coverage and building a tax-efficient health strategy.

What are the HDHP eligibility requirements and 2026 HSA thresholds?

The IRS defines an HDHP by two specific numbers: the minimum annual deductible and the maximum out-of-pocket limit. Both must fall within IRS thresholds for your plan to qualify for HSA contributions.

For 2026, the minimum annual deductible is $1,700 for self-only coverage and $3,400 for family coverage. These figures set the floor. Your plan’s deductible must meet or exceed these amounts to count as an HDHP under IRS rules.

The out-of-pocket maximums cap at $8,500 for self-only and $17,000 for family coverage in 2026. Your plan cannot exceed these caps and still qualify. This ceiling protects you from catastrophic costs while keeping the plan within HDHP classification.

Once you confirm HDHP status, you can contribute to an HSA. The 2026 HSA contribution limits are $4,400 for self-only coverage and $8,750 for family coverage, with an additional $1,000 catch-up contribution allowed if you are 55 or older. That catch-up provision alone can meaningfully reduce taxable income for older self-employed workers.

2026 HDHP and HSA thresholds at a glance

| Coverage Type | Minimum Deductible | Max Out-of-Pocket | HSA Contribution Limit |

|---|---|---|---|

| Self-only | $1,700 | $8,500 | $4,400 |

| Family | $3,400 | $17,000 | $8,750 |

| Age 55+ catch-up | N/A | N/A | +$1,000 |

One major 2026 change affects which plans qualify. All ACA Bronze and Catastrophic plans on the individual market are now treated as HDHPs eligible for HSA pairing, regardless of whether their specific deductible or out-of-pocket figures meet the traditional thresholds. This policy expansion gives self-employed workers shopping on the Marketplace far more options than before. That said, always confirm HSA eligibility directly with your insurer and HSA provider before enrolling, since plan design details still matter.

Key eligibility requirements to keep in mind:

- You cannot be enrolled in Medicare and contribute to an HSA simultaneously.

- You cannot be claimed as a dependent on someone else’s tax return.

- You cannot have other disqualifying health coverage, such as a general-purpose Flexible Spending Account (FSA).

- Your HDHP must be your primary coverage.

How does the SEHI deduction work alongside HDHP and HSA benefits?

The Self-Employed Health Insurance deduction is an above-the-line adjustment, meaning it reduces your adjusted gross income (AGI) without requiring you to itemize deductions. That makes it valuable even if you take the standard deduction. The SEHI deduction covers 100% of qualifying premiums reported on Schedule 1, Line 17, for yourself, your spouse, and your dependents.

The deduction is not unlimited. It is capped by your net self-employment profit for the year. If your business runs at a loss, you cannot claim the SEHI deduction for that period. This is a critical planning point for freelancers with variable income.

SEHI eligibility excludes months where you or your spouse had access to subsidized employer-sponsored coverage. If your spouse was eligible for a group plan through their employer in March, you cannot claim the SEHI deduction for March, even if you did not actually enroll in that plan. The IRS looks at eligibility, not enrollment.

The good news is that the IRS treats SEHI and HSA contributions as entirely separate benefits. You can claim both in the same tax year, provided you meet the eligibility rules for each independently. A self-employed graphic designer, for example, could deduct $7,200 in annual premiums via SEHI and contribute $4,400 to an HSA, reducing AGI by $11,600 before any other deductions apply.

Pro Tip: Track every month of your health insurance eligibility separately. If your spouse gains access to employer coverage mid-year, your SEHI deduction must be prorated. Missing this detail is one of the most common audit triggers for self-employed filers.

Higher-income self-employed individuals gain disproportionately from this combination because both deductions reduce AGI at their marginal tax rate. A freelancer in the 32% bracket saves $3,712 in federal income tax on that same $11,600 reduction.

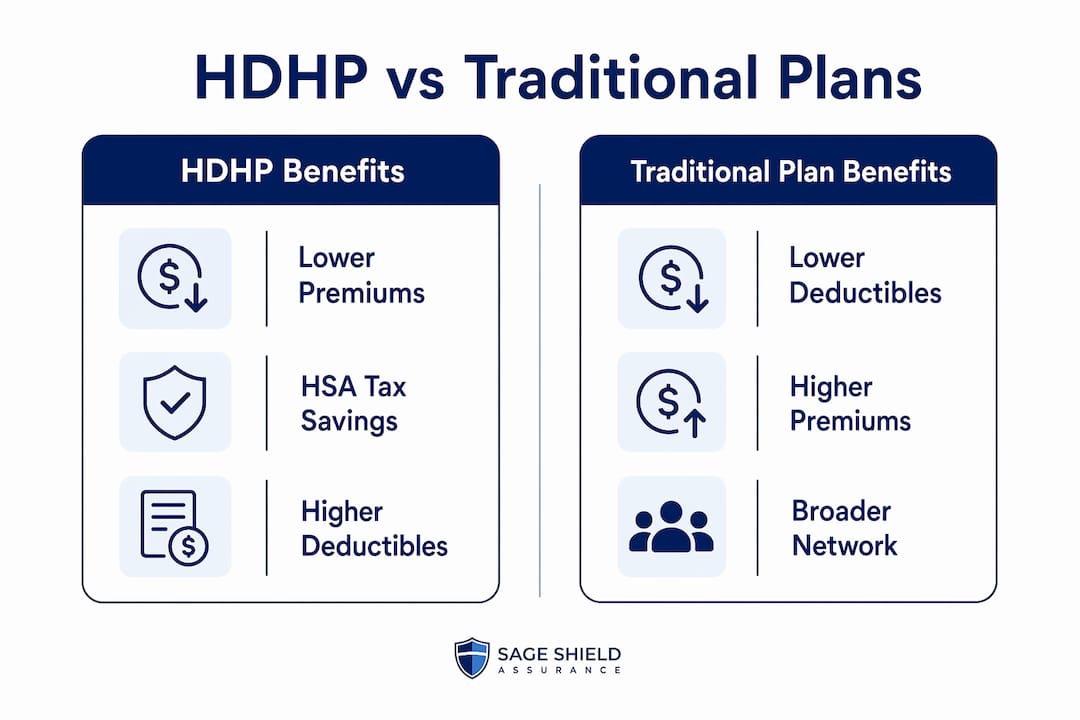

What practical advantages do HDHPs with HSAs offer vs. traditional plans?

The most immediate advantage of a high-deductible plan for self-employed individuals is the lower monthly premium. When you are covering 100% of your own insurance costs with no employer contribution, even a $200 to $400 monthly difference in premium adds up to $2,400 to $4,800 in annual savings. That cash stays in your pocket until you actually need care.

The HSA compounds those savings through what the IRS effectively structures as a triple tax advantage: contributions are tax-deductible, earnings grow tax-deferred, and qualified withdrawals for medical expenses are completely tax-free. No other savings vehicle in the U.S. tax code offers all three of these benefits simultaneously. A 401(k) gives you two. An HSA gives you three.

How HDHPs with HSAs compare to traditional PPO plans for self-employed workers

| Feature | HDHP with HSA | Traditional PPO |

|---|---|---|

| Monthly premium | Lower | Higher |

| Annual deductible | Higher | Lower |

| Tax-advantaged savings account | Yes (HSA) | No (FSA only, limited) |

| Premium deductible via SEHI | Yes | Yes |

| Portable savings growth | Yes | No |

| Retirement savings potential | Yes (after 65) | No |

Four practical advantages stand out for self-employed workers specifically:

- Cash flow flexibility. Lower premiums reduce fixed monthly expenses, which matters when client payments are irregular.

- HSA as a retirement supplement. After age 65, HSA funds can be withdrawn for any purpose and taxed as ordinary income, functioning like a traditional IRA without the required minimum distributions.

- Expanded plan choices in 2026. With 35% of Marketplace plans now HSA-eligible, independent contractors have more options than at any prior point under the ACA. More competition among eligible plans typically means better pricing.

- Preventive care without deductible costs. HDHPs are required by law to cover preventive services, including annual physicals, screenings, and vaccinations, at no cost before you meet your deductible. Telehealth services also receive favorable treatment under current HDHP rules.

What are common pitfalls and planning tips for maximizing HDHP benefits?

The SEHI deduction and HSA are both powerful, but each has traps that catch self-employed filers off guard. Avoiding these errors requires attention to detail that most general tax guides skip.

The most frequent mistake is claiming the SEHI deduction for months when employer-sponsored coverage was available. This applies even if the employer plan was inferior or more expensive. The IRS standard is access, not quality. Review your eligibility month by month, not annually.

S-corporation owners face a specific structural requirement. Premiums must flow through payroll and appear on your W-2 for the SEHI deduction to survive scrutiny. If you pay premiums directly without routing them through the S-corp’s payroll system, the deduction can be disallowed entirely. This is not a gray area. The IRS has clear guidance, and incorrect handling is a documented audit risk.

Pro Tip: Use your HSA funds first for deductible expenses and medical emergencies rather than investing everything immediately. Build a cash buffer of at least one year’s deductible before shifting HSA contributions into investment funds. This prevents forced liquidation of investments during a health event.

Additional planning practices that protect your deductions:

- Keep a month-by-month log of health insurance eligibility, especially if your spouse’s employment situation changes during the year.

- Confirm HSA eligibility with your insurer in writing after selecting any plan, particularly under the new 2026 ACA expansion rules.

- Separate your HSA contributions from your business checking account to simplify documentation.

- Recalculate your SEHI deduction limit each quarter as net self-employment income becomes clearer, especially if your income fluctuates significantly.

Meticulous bookkeeping of eligibility months and income limits is not optional. It is the foundation of a defensible tax position. Self-employed individuals who treat this as an afterthought often leave thousands in deductions unclaimed or face penalties for overclaiming.

Key takeaways

HDHPs paired with HSAs and the SEHI deduction form the most tax-efficient health coverage structure available to self-employed individuals in 2026.

| Point | Details |

|---|---|

| HDHP thresholds are IRS-defined | 2026 minimums are $1,700 self-only and $3,400 family deductibles; out-of-pocket caps are $8,500 and $17,000. |

| HSA contributions reduce AGI directly | Contribute up to $4,400 self-only or $8,750 family in 2026, plus $1,000 catch-up if 55 or older. |

| SEHI and HSA benefits stack independently | You can claim both in the same year under separate IRS rules, compounding your total tax reduction. |

| 2026 ACA expansion widens your options | ACA Bronze and Catastrophic plans now qualify for HSA pairing, giving self-employed workers more Marketplace choices. |

| S-corp owners need payroll compliance | Premiums must appear on your W-2 through payroll to qualify for the SEHI deduction without audit risk. |

Why I think most self-employed workers underuse this combination

Most freelancers I have seen pick a health plan based on the premium number alone. They see the lower monthly cost of an HDHP, choose it to save money, and then never open an HSA. That is leaving the most valuable part of the strategy completely unused.

The SEHI deduction is similarly underutilized. Because it requires tracking eligibility by month and tying it to net self-employment income, many self-employed filers either skip it entirely or claim it incorrectly. Both errors are costly. The above-the-line nature of this deduction means it reduces your AGI before your tax bracket is even calculated, which has downstream effects on other income-based thresholds.

The 2026 expansion of HSA eligibility to ACA Bronze and Catastrophic plans is genuinely significant. It means that self-employed workers who previously chose a Bronze plan for its low premium but assumed they could not open an HSA now have that option. The combination of a low-premium Bronze plan, full HSA contributions, and the SEHI deduction is the most aggressive legal tax reduction available to someone without an employer.

My honest observation after working through these structures: the people who benefit most are those who treat their health insurance as a financial planning decision, not just a healthcare decision. Confirming HSA eligibility with your provider before enrollment takes one phone call. That call can unlock thousands in annual tax savings. The math is not complicated. The discipline to do it is.

— mkaravas1m

How Sageshieldassurance helps self-employed individuals find the right HDHP

Choosing the right health insurance plan as a self-employed individual means weighing premiums, deductibles, HSA eligibility, and SEHI deduction rules simultaneously. Most people do not have the time or background to do that analysis correctly on their own.

Sageshieldassurance works exclusively with self-employed individuals and business owners across 40 states, matching clients to HDHP and HSA-eligible plans from leading carriers while clarifying exactly how the SEHI deduction applies to their situation. Their team reviews your income, coverage needs, and tax position to identify the plan that minimizes your total annual cost, not just your monthly premium. If you are ready to stop guessing and start optimizing, explore your self-employed coverage options with a broker who specializes in exactly this.

FAQ

What qualifies as an HDHP for HSA eligibility in 2026?

A plan qualifies as an HDHP in 2026 if it has a minimum deductible of $1,700 for self-only or $3,400 for family coverage and does not exceed out-of-pocket caps of $8,500 or $17,000 respectively. Starting January 1, 2026, all ACA Bronze and Catastrophic plans on the individual market also qualify automatically.

Can self-employed individuals deduct both premiums and HSA contributions?

Yes. The IRS treats the SEHI deduction and HSA contributions as separate benefits, so you can claim both in the same tax year provided you meet the eligibility requirements for each independently.

Does the SEHI deduction apply if my spouse has employer coverage?

No. You cannot claim the SEHI deduction for any month in which you or your spouse had access to subsidized employer-sponsored health coverage, even if you did not enroll in that plan.

How much can I contribute to an HSA as a self-employed individual in 2026?

The 2026 HSA contribution limits are $4,400 for self-only HDHP coverage and $8,750 for family coverage. If you are 55 or older, you can add a $1,000 catch-up contribution on top of those limits.

Do S-corp owners have special rules for the health insurance deduction?

Yes. S-corporation shareholder owners must route health insurance premiums through the company’s payroll system and have them reported on their W-2 to qualify for the SEHI deduction. Paying premiums directly without this payroll step is a documented audit risk.

Leave a Reply